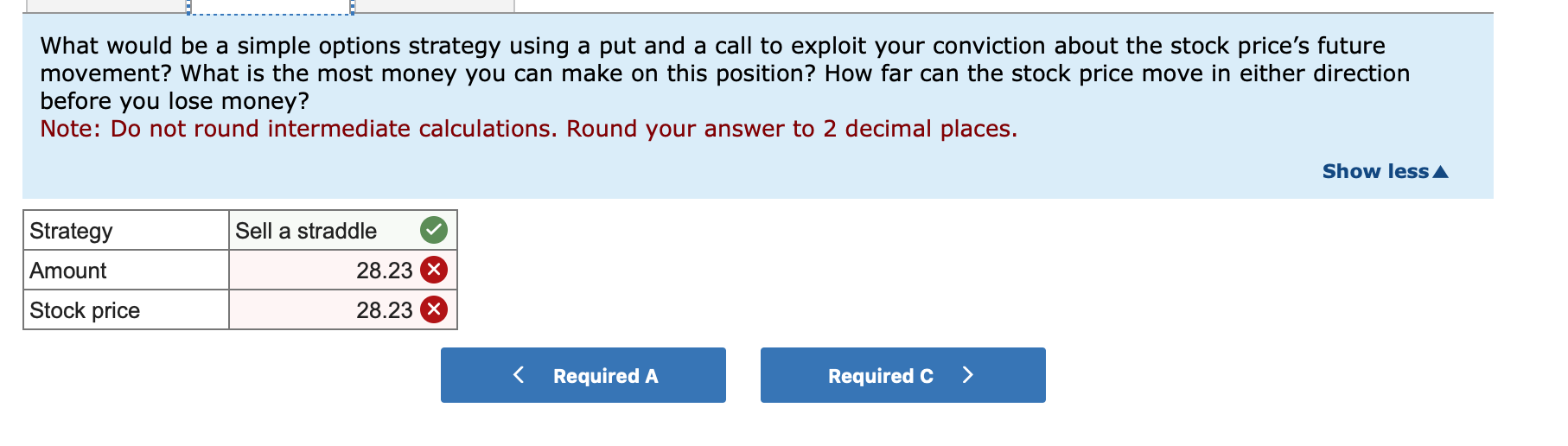

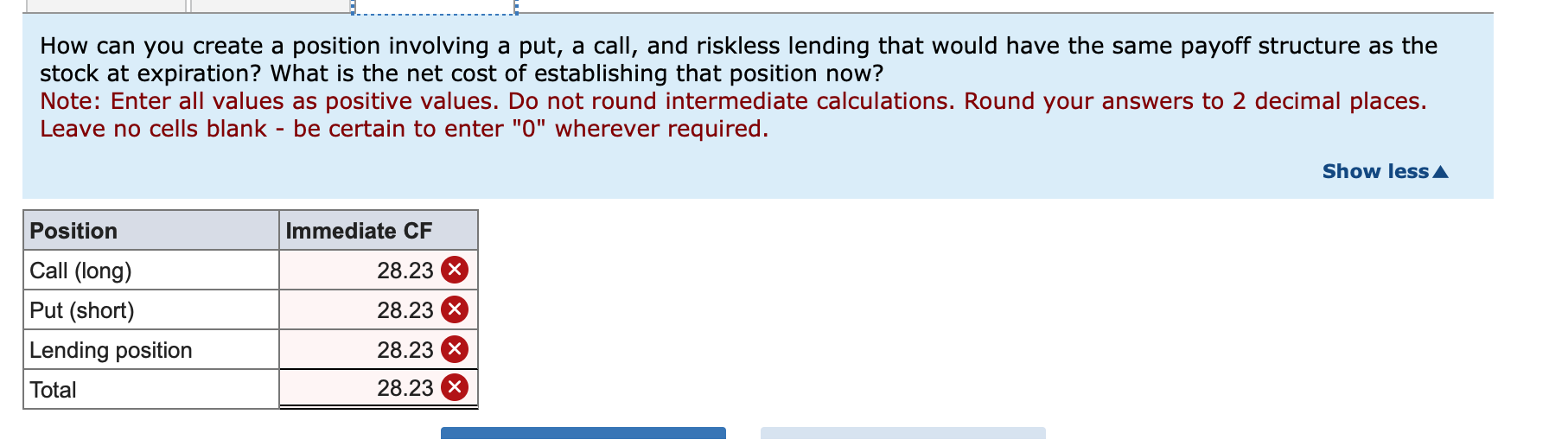

Question: What would be a simple options strategy using a put and a call to exploit your conviction about the stock price's future movement? What is

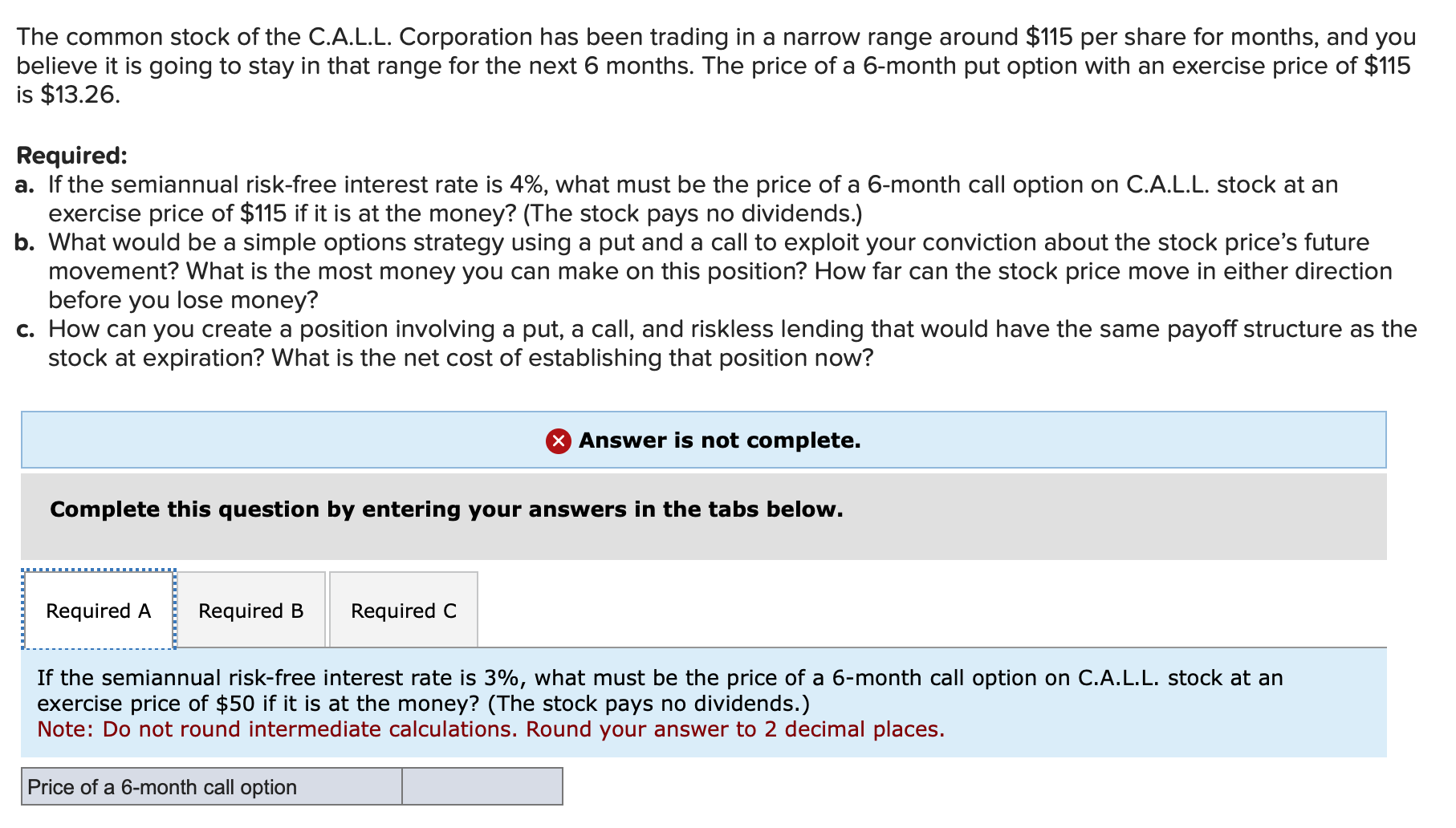

What would be a simple options strategy using a put and a call to exploit your conviction about the stock price's future movement? What is the most money you can make on this position? How far can the stock price move in either direction before you lose money? Note: Do not round intermediate calculations. Round your answer to 2 decimal places. How can you create a position involving a put, a call, and riskless lending that would have the same payoff structure as the stock at expiration? What is the net cost of establishing that position now? Note: Enter all values as positive values. Do not round intermediate calculations. Round your answers to 2 decimal places. Leave no cells blank - be certain to enter "0" wherever required. The common stock of the C.A.L.L. Corporation has been trading in a narrow range around $115 per share for months, and you believe it is going to stay in that range for the next 6 months. The price of a 6 -month put option with an exercise price of $115 is $13.26. Required: a. If the semiannual risk-free interest rate is 4%, what must be the price of a 6 -month call option on C.A.L.L. stock at an exercise price of $115 if it is at the money? (The stock pays no dividends.) b. What would be a simple options strategy using a put and a call to exploit your conviction about the stock price's future movement? What is the most money you can make on this position? How far can the stock price move in either direction before you lose money? c. How can you create a position involving a put, a call, and riskless lending that would have the same payoff structure as the stock at expiration? What is the net cost of establishing that position now? Answer is not complete. Complete this question by entering your answers in the tabs below. If the semiannual risk-free interest rate is 3%, what must be the price of a 6 -month call option on C.A.L.L. stock at an exercise price of $50 if it is at the money? (The stock pays no dividends.) Note: Do not round intermediate calculations. Round your answer to 2 decimal places

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts