?Price History?, which lists a fictitious set of prices for Jan ?21 oil futures during the month

Question:

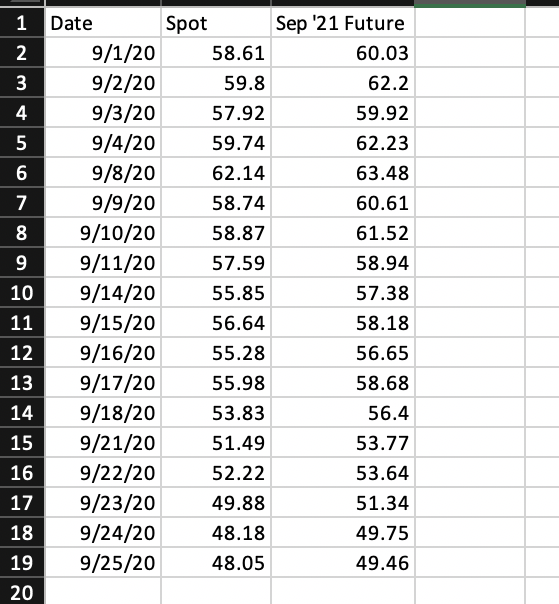

?Price History?, which lists a fictitious set of prices for Jan ?21 oil futures during the month of September. Recall that oil futures quotes are the per-barrel price, and one futures contract is to buy or sell 1,000 barrels of oil. The initial margin for a contract initiated on 9/1 is $6,000. The maintenance margin is 7.5% of current exposure. On a margin call, you must bring your account back to the higher of your initial or your maintenance margin. On September 25, you need to sell 100,000 barrels of oil. You decide to hedge this risk by taking a futures position that you will close out after settlement on 9/25. Assume that on 9/25 you can sell the oil for the spot settlement price that day.

- Suppose instead that after the payment of the initial margin, you did not have the liquidity to make margin calls. Instead, the clearinghouse closes out the minimum number of contracts required to keep your account active. How many contracts would you have at the end of the month? [This is probably the hardest part]

- Based on the situation outlined in part (e), what is the profit or loss from the futures strategy?

- The firm could have avoided losing the contracts by setting aside money for margin calls at initiation. What is the minimum amount that would need to have been set aside, given this set of price movements, and what would be the de facto leverage of such a strategy? [By de facto leverage, I mean: If the oil futures price were to change by 1%, by what percent would your investment change, using the amount calculated in part (g) as your initial outlay]

- What is the minimum amount that would need to be set aside to guarantee the ability to make margin calls for any set of price movements?

Expert Answer:

Answers a You should take a short futures position because you wish to hedge against a fall in oil p... View the full answer

Accounting

ISBN: 978-1118608227

9th edition

Authors: Lew Edwards, John Medlin, Keryn Chalmers, Andreas Hellmann, Claire Beattie, Jodie Maxfield, John Hoggett