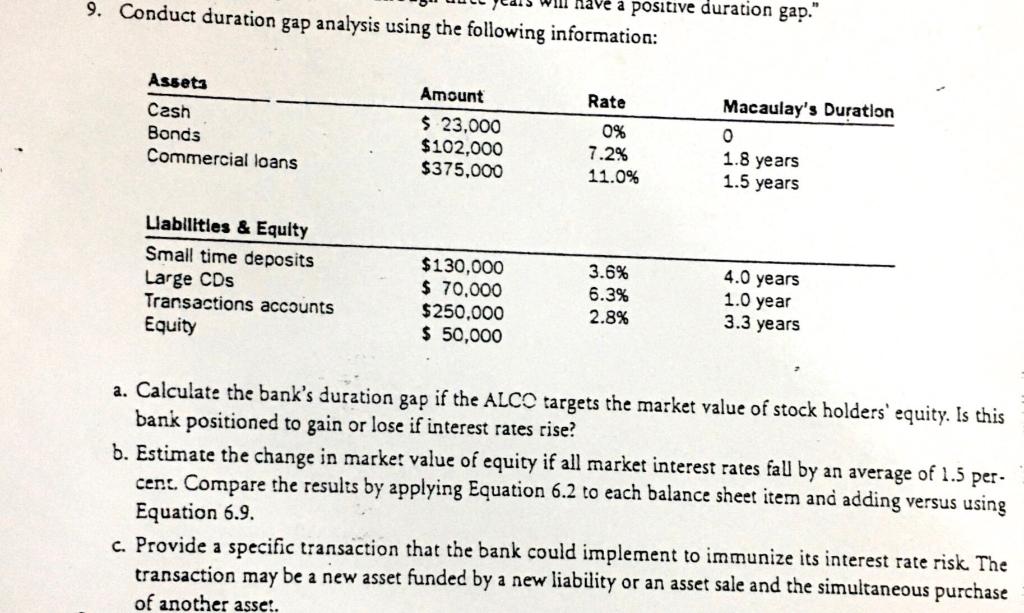

Question: will have a positive duration gap. 9. Conduct duration gap analysis using the following information: Assets Cash Amount Rate Macaulay's Duration $ 23,000 0%

will have a positive duration gap." 9. Conduct duration gap analysis using the following information: Assets Cash Amount Rate Macaulay's Duration $ 23,000 0% 0 Bonds $102,000 7.2% 1.8 years Commercial loans $375,000 11.0% 1.5 years Liabilities & Equity Small time deposits $130,000 3.6% 4.0 years Large CDs $ 70,000 6.3% 1.0 year Transactions accounts $250,000 2.8% 3.3 years Equity $ 50,000 a. Calculate the bank's duration gap if the ALCO targets the market value of stock holders' equity. Is this bank positioned to gain or lose if interest rates rise? b. Estimate the change in market value of equity if all market interest rates fall by an average of 1.5 per- cent. Compare the results by applying Equation 6.2 to each balance sheet item and adding versus using Equation 6.9. c. Provide a specific transaction that the bank could implement to immunize its interest rate risk. The transaction may be a new asset funded by a new liability or an asset sale and the simultaneous purchase of another asset.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts