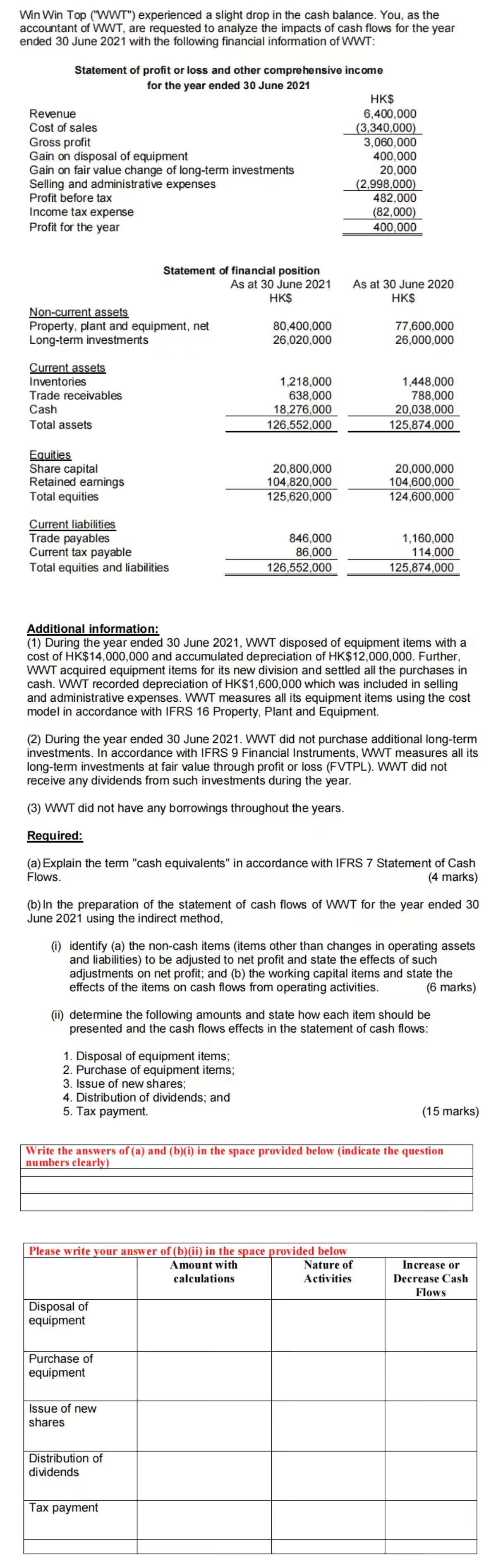

Win Win Top (WWT) experienced a slight drop in the cash balance. You, as the accountant...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a Cash equivalents refers to shortterm highly liquid investments that are readily convertible into known amounts of cash and have original maturities ... View the full answer

Related Book For

Financial Accounting and Reporting

ISBN: 978-0273744443

14th Edition

Authors: Barry Elliott, Jamie Elliott

Posted Date: