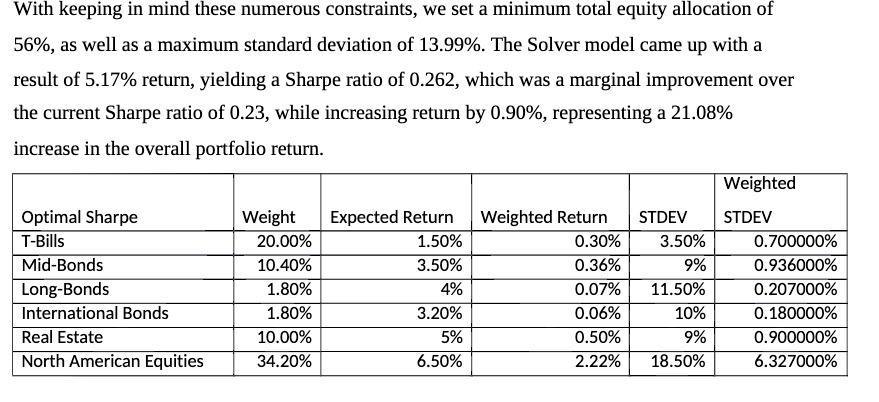

Question: With keeping in mind these numerous constraints, we set a minimum total equity allocation of 56%, as well as a maximum standard deviation of 13.99%.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock