Question: Without Excel and with process Section B - Long Answer (13 points) Answer the following questions. Submit your handwritten providing clear explanation of your method.

Without Excel and with process

Without Excel and with process

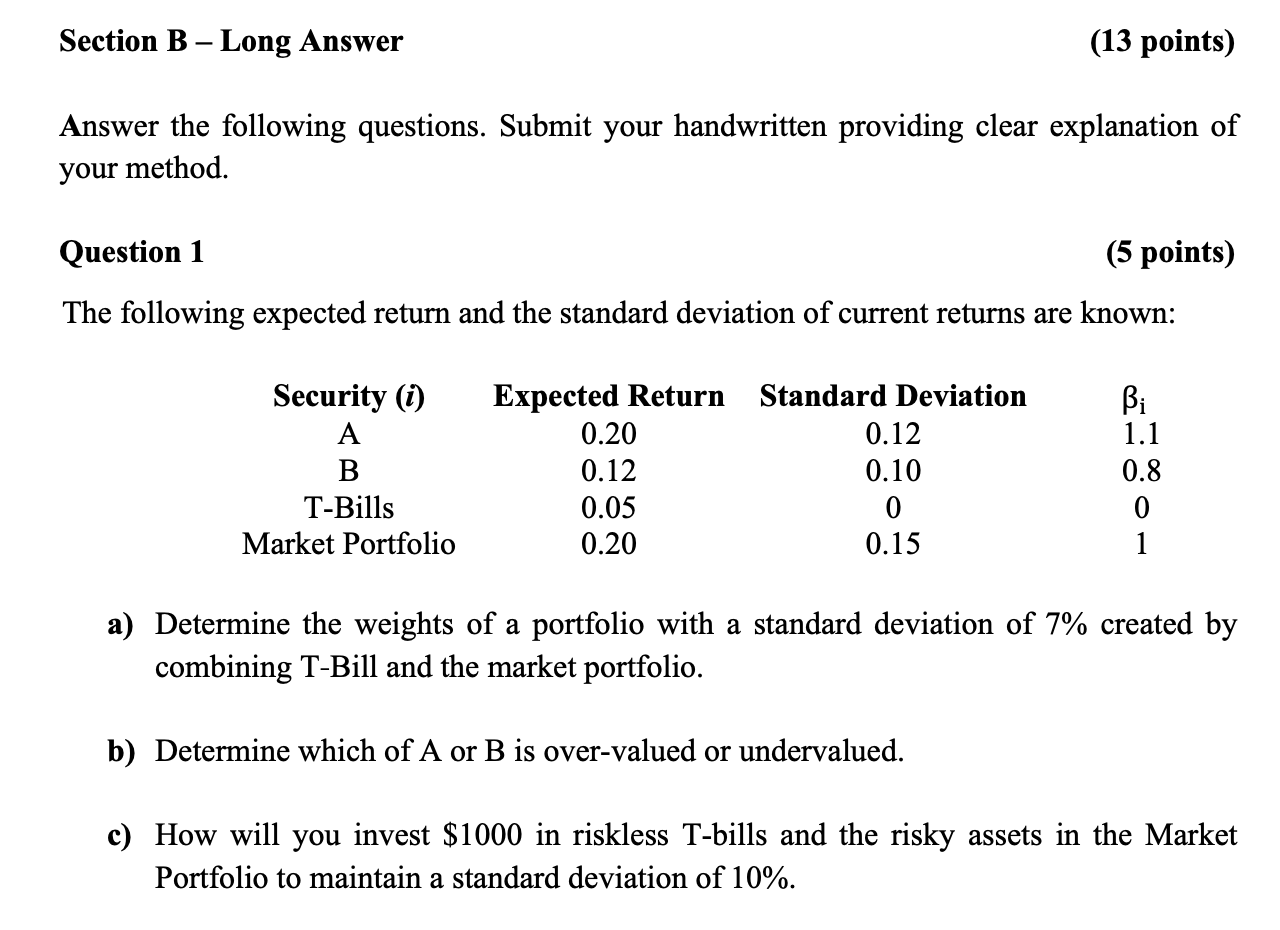

Section B - Long Answer (13 points) Answer the following questions. Submit your handwritten providing clear explanation of your method. Question 1 (5 points) The following expected return and the standard deviation of current returns are known: a) Determine the weights of a portfolio with a standard deviation of 7% created by combining T-Bill and the market portfolio. b) Determine which of A or B is over-valued or undervalued. c) How will you invest $1000 in riskless T-bills and the risky assets in the Market Portfolio to maintain a standard deviation of 10%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock