Question: write a brief case analysis. 400 words Summarize the case and the problem the company that the case follows in your own words. (3pts Explain

write a brief case analysis. 400 words

- Summarize the case and the problem the company that the case follows in your own words. (3pts

- Explain your recommendation to the company that the case follows. (4pts)

- Justify your recommendation using concepts learned throughout your MBA program

400 words

- Summarize the case and the problem the company that the case follows in your own words. (3pts

- Explain your recommendation to the company that the case follows. (4pts)

- Justify your recommendation using concepts learned throughout your MBA program

400 words

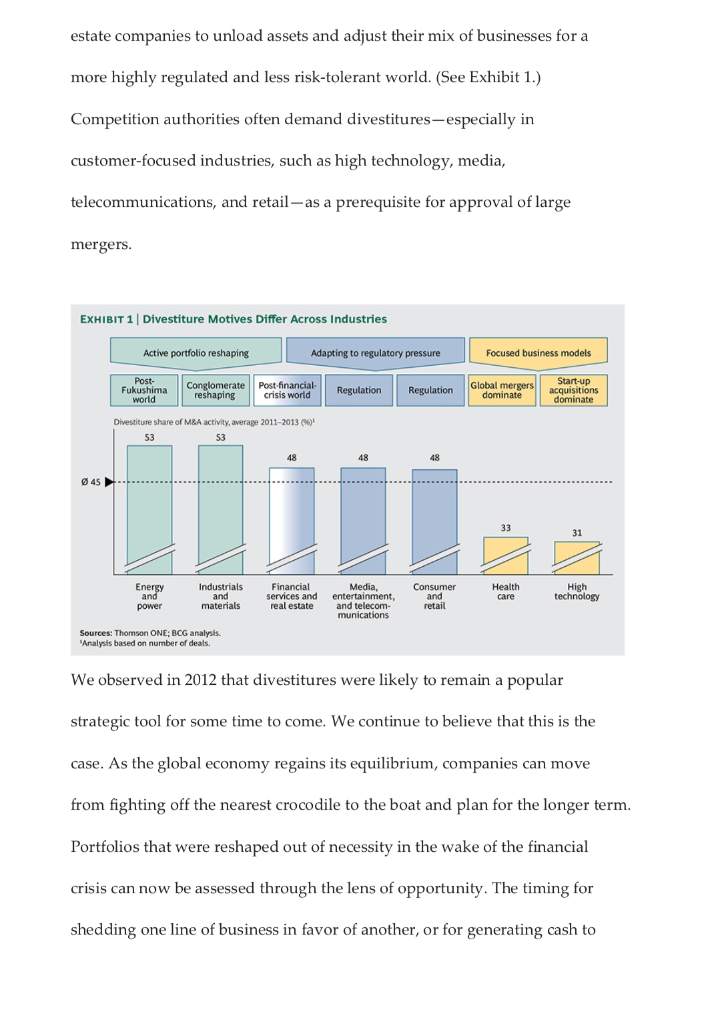

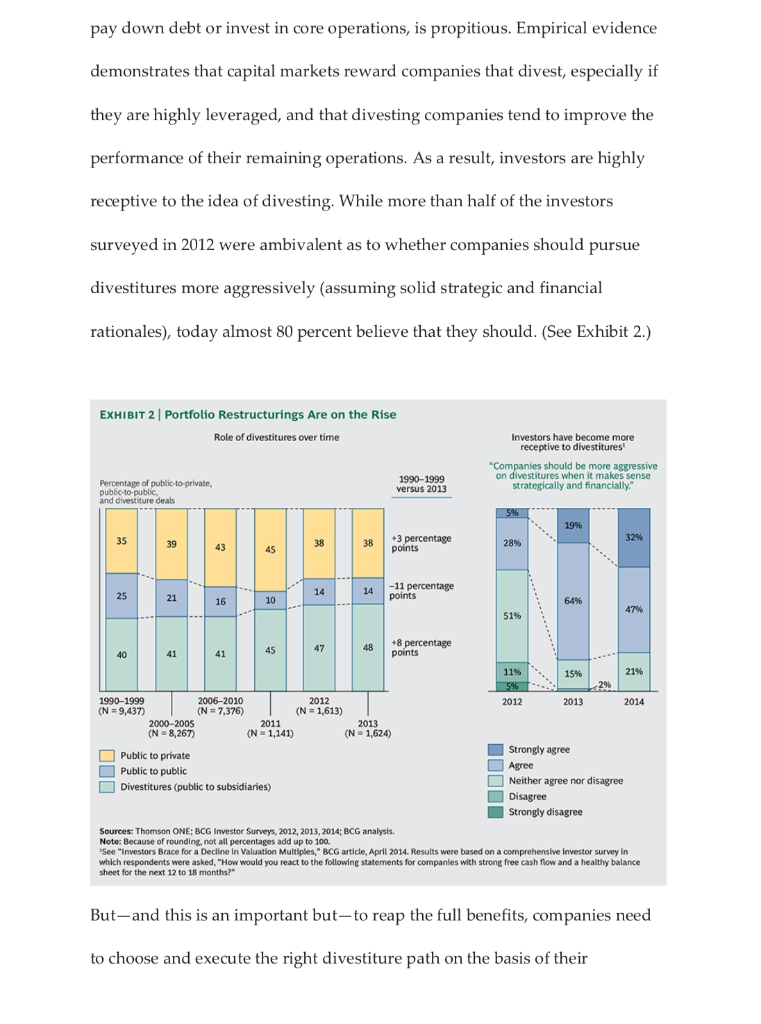

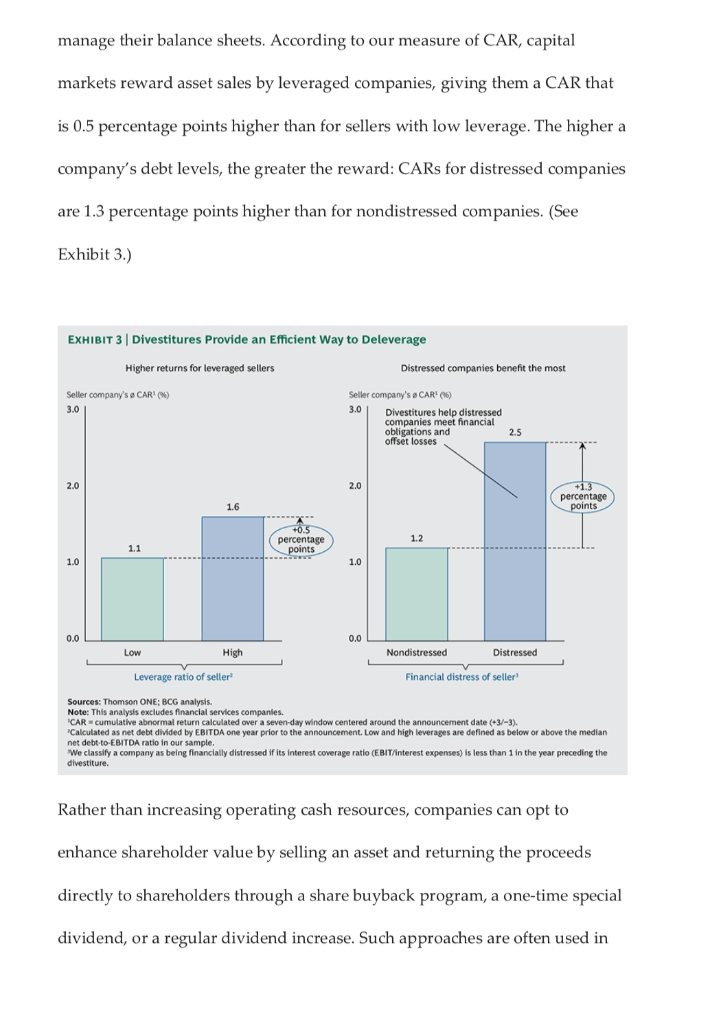

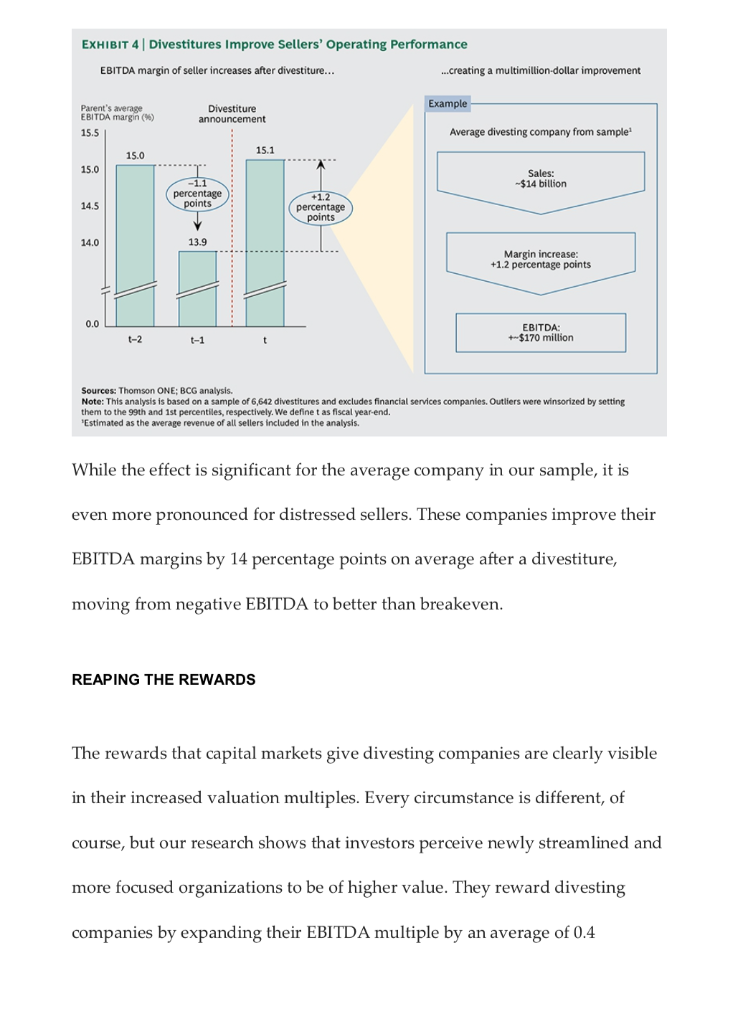

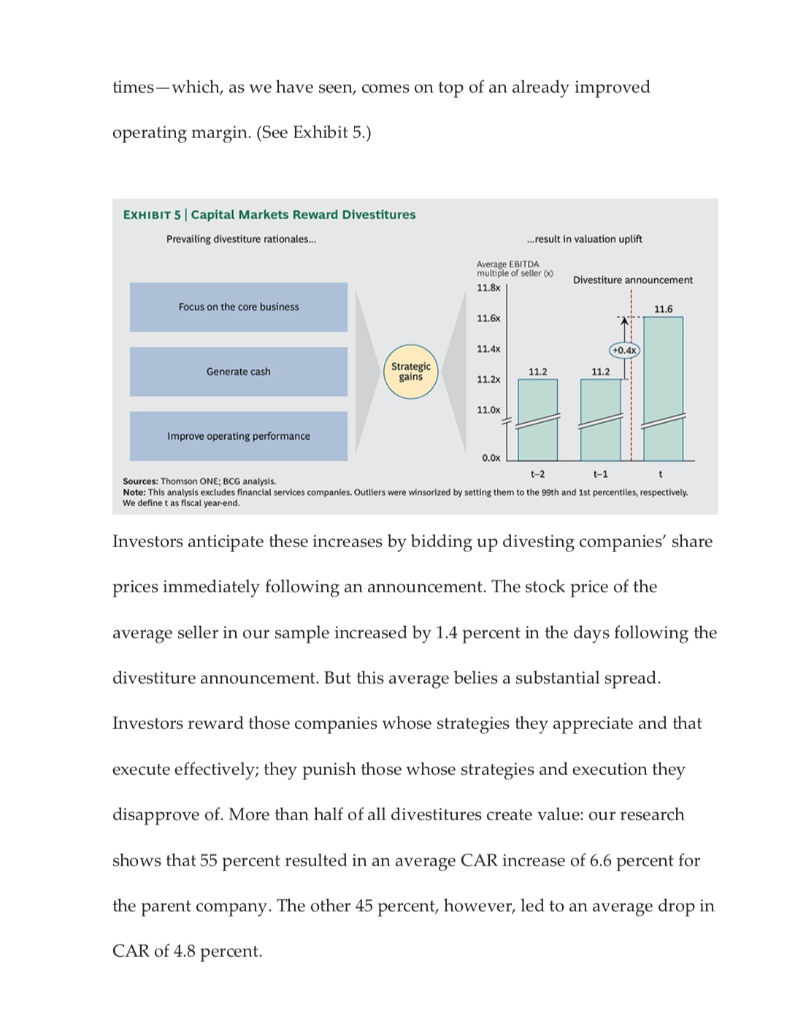

Most executives are not naturally inclined toward breaking things up; they would rather grow and create value through building than through dividing. But we live in a time when most business units can conceivably be assets in play. The truly strategic question any company or CEO needs to ask is whether one company's assets could have a higher value for another company. (See Looking Anew at the Value of Divesting, BCG article, August 2012.) For all kinds of companies, the answer increasingly is yes. Companies in energy, industrials and materials, financial services and real estate, media and telecommunications, and consumer and retail have been particularly active divestors since 2011, especially when compared with industries such as health care and high tech, where business dynamics cause mergers and acquisitions to dominate activity. Sixteen of the 50 biggest divestitures in 2013 were made by energy and financial services companies. The factors driving divestitures vary by industry. Conglomerates have actively reshaped their portfolios in a time of economic uncertainty and volatility. Energy companies have shed assets as they adjust to a post-Fukushima world, react to regulatory shifts (especially in Europe), and position themselves to pursue new opportunities in shale gas and renewable energies. Regulatory and financial pressures have pushed financial and real Most executives are not naturally inclined toward breaking things up; they would rather grow and create value through building than through dividing. But we live in a time when most business units can conceivably be assets in play. The truly strategic question any company or CEO needs to ask is whether one company's assets could have a higher value for another company. (See Looking Anew at the Value of Divesting, BCG article, August 2012.) For all kinds of companies, the answer increasingly is yes. Companies in energy, industrials and materials, financial services and real estate, media and telecommunications, and consumer and retail have been particularly active divestors since 2011, especially when compared with industries such as health care and high tech, where business dynamics cause mergers and acquisitions to dominate activity. Sixteen of the 50 biggest divestitures in 2013 were made by energy and financial services companies. The factors driving divestitures vary by industry. Conglomerates have actively reshaped their portfolios in a time of economic uncertainty and volatility. Energy companies have shed assets as they adjust to a post-Fukushima world, react to regulatory shifts (especially in Europe), and position themselves to pursue new opportunities in shale gas and renewable energies. Regulatory and financial pressures have pushed financial and real estate companies to unload assets and adjust their mix of businesses for a more highly regulated and less risk-tolerant world. (See Exhibit 1.) Competition authorities often demand divestitures-especially in customer-focused industries, such as high technology, media, telecommunications, and retail - as a prerequisite for approval of large mergers. EXHIBIT 1 Divestiture Motives Differ Across Industries | Active portfolio reshaping Adapting to regulatory pressure Focused business models Post- Fukushima world Conglomerate Post-financial- reshaping crisis world Regulation Regulation Global mergers dominate Start-up acquisitions dominate Divestiture share of M&A activity, average 2011-2013) 53 53 48 48 48 45 33 31 Energy and" power Industrials and materials Financial services and real estate Media, entertainment, and telecom- munications Consumer and retail Health care High technology Sources: Thomson ONE; BOG analysis. "Analysis based on number of deals. We observed in 2012 that divestitures were likely to remain a popular strategic tool for some time to come. We continue to believe that this is the case. As the global economy regains its equilibrium, companies can move from fighting off the nearest crocodile to the boat and plan for the longer term. Portfolios that were reshaped out of necessity in the wake of the financial crisis can now be assessed through the lens of opportunity. The timing for shedding one line of business in favor of another, or for generating cash to pay down debt or invest in core operations, is propitious. Empirical evidence demonstrates that capital markets reward companies that divest, especially if they are highly leveraged, and that divesting companies tend to improve the performance of their remaining operations. As a result, investors are highly receptive to the idea of divesting. While more than half of the investors surveyed in 2012 were ambivalent as to whether companies should pursue divestitures more aggressively (assuming solid strategic and financial rationales), today almost 80 percent believe that they should. (See Exhibit 2.) EXHIBIT 2 Portfolio Restructurings Are on the Rise Role of divestitures over time Investors have become more receptive to divestitures! "Companies should be more aggressive on divestitures when it makes sense strategically and financially." Percentage of public-to-private, public-to-public and divestiture deals 1990-1999 versus 2013 5% 19% 32% 35 39 38 38 +3 percentage points 28% 43 45 14 14 -11 percentage 25 21 16 10 points 64% 47% 51% 47 48 40 41 45 +8 percentage points 41 11% 15% 21% 596 29 1990-1999 2006-2010 2012 2012 2013 2014 (N = 9,437) (N = 7,376) (N = 1,613) 2000-2005 2011 2013 (N = 8,267) (N = 1,141) (N = 1,624) Public to private Strongly agree ] Public to public O Agree Divestitures (public to subsidiaries) Neither agree nor disagree Disagree Strongly disagree Sources: Thomson ONE; BCG Investor Surveys, 2012, 2013, 2014; BCG analysis. Note: Because of rounding, not all percentages add up to 100. See "Investors Brace for a Decline in Valuation Multiples, " BCG article, April 2014. Results were based on a comprehensive investor survey in which respondents were asked, "How would you react to the following statements for companies with strong free cash flow and a healthy balance sheet for the next 12 to 18 months?" But-and this is an important but-to reap the full benefits, companies need to choose and execute the right divestiture path on the basis of their individual situation, the attributes of the assets being shed, and the market environment at the time of the transaction. (See Maximizing Value: Choose the Right Exit Route, BCG article, September 2014.) LOTS OF REASONS TO LET GO Companies divest assets and operations to adapt to an evolving business environment. Specific reasons change over time with shifts in the economy, individual industry dynamics, regulatory policy, and other factors, but three of the most consistent are the following: Focusing on the core business Generating cash Improving operating performance Focusing on the Core Business. Capital and management time are scarce resources; CEOs have to decide where to put their attention and their money. Even companies operating in a single sector or category can find themselves managing multiple brands or lines of business. The question needs to be asked periodically, especially when economic, business, or regulatory conditions shift: is an asset generating sufficient value or could it do better with somebody else (including as a stand-alone company), and could the current parent deploy time and cash better in its other operations? The capital markets' answer to that question is often a clear yes, which can easily be seen in prevailing "conglomerate discounts that markets assign to diversified companies. BCG research shows that the long-term average discount is 13.9 percent. (See Invest Wisely, Divest Strategically: Tapping the Power of Diversity to Raise Valuations, BCG Focus, April 2014.) It's hardly surprising that diversified companies are also active divestors. In the U.S., General Electric has shed 57 businesses since 1990, Invensys of the UK has unloaded 30, and Germany's Siemens, 24. The list of top divesting companies since 1990 includes three banks (Deutsche Bank, JPMorgan Chase, and Citigroup) that needed to navigate the financial crisis and reorient themselves for a postcrisis environment, and two consumer-goods companies, Philips and Unilever, for which continual portfolio reshaping is not unusual. Divesting does not necessarily mean shrinking, however. While divesting companies reduce complexity and improve capital allocation, they also accumulate war chests for investing in existing operations and funding acquisitions. Generating Cash. Cash proceeds from asset sales are often used to fund acquisitions or reduce debt, especially when companies are overextended or economies slow. Capital markets are sensitive to how leveraged companies manage their balance sheets. According to our measure of CAR, capital markets reward asset sales by leveraged companies, giving them a CAR that is 0.5 percentage points higher than for sellers with low leverage. The higher a company's debt levels, the greater the reward: CARs for distressed companies are 1.3 percentage points higher than for nondistressed companies. (See Exhibit 3.) EXHIBIT 3 Divestitures Provide an Efficient Way to Deleverage Higher returns for leveraged sellers Distressed companies benefit the most Seller company's CARI (16 ) 3.0 Seller company's a CAR (6) 8 3.0 Divestitures help distressed companies meet financial obligations and offset losses 2.5 2.0 2.0 +1.3 percentage points 1.6 +0.5 percentage points 1.2 1.1 1.0 1.0 0.0 0.0 Low High Nondistressed Distressed Leverage ratio of seller Financial distress of seller! Sources: Thomson ONE; BCG analysis. Note: This analysis excludes financial services companies. "CAR -cumulative abnormal return calculated over a seven-day window centered around the announcement date (+3/-3). Calculated as net debt divided by EBITDA one year prior to the announcement. Low and high leverages are defined as below or above the median net debt-to-EBITDA ratio in our sample. We classify a company as being financially distressed if its interest coverage ratio (EBIT/Interest expenses) is less than 1 in the year preceding the ( divestiture. Rather than increasing operating cash resources, companies can opt to enhance shareholder value by selling an asset and returning the proceeds directly to shareholders through a share buyback program, a one-time special dividend, or a regular dividend increase. Such approaches are often used in mature low-growth industries where opportunities for reinvestment are few unless management embarks on a diversification program. Improving Operating Performance. Divesting companies often achieve higher profitability from an improved focus on core activities. Many companies get an added boost because the business being sold or spun off was a corporate orphan, receiving inadequate investment and attention, and consequently producing poor performance. Its sale lifts overall profitability. Increased management focus on the remaining assets, better capital allocation, and the availability of more funds to inv in the remaining business result in improved growth and profitability for the portfolio. Our analysis of 6,642 divesting companies since 1990 shows that EBITDA margins increase by more than 1 percentage point between the announcement of a divestiture and the end of the company's fiscal year. For our average seller, which has approximately $14 billion in annual sales, this translates into an increase of $170 million in EBITDA. The large size of our average seller reflects the fact that big international companies tend to be the most active divestors. (See Exhibit 4.) EXHIBIT 4 Divestitures Improve Sellers' Operating Performance EBITDA margin of seller increases after divestiture... ...creating a multimillion-dollar improvement Example Parent's average EBITDA margin() 15.5 Divestiture announcement Average divesting company from sample 15.1 15.0 15.0 Sales: --$14 billion percentage points 14.5 +1.2 percentage points 14.0 13.9 Margin increase: +1.2 percentage points 0.0 EBITDA: +$170 million t-2 t-1 t Sources: Thomson ONE; BCG analysis. Note: This analysis is based on a sample of 6,642 divestitures and excludes financial services companies. Outliers were winsorized by setting them to the 99th and 1st percentiles, respectively. We define tas fiscal year-end. 'Estimated as the average revenue of all sellers included in the analysis. While the effect is significant for the average company in our sample, it is even more pronounced for distressed sellers. These companies improve their EBITDA margins by 14 percentage points on average after a divestiture, moving from negative EBITDA to better than breakeven. REAPING THE REWARDS The rewards that capital markets give divesting companies are clearly visible in their increased valuation multiples. Every circumstance is different, of course, but our research shows that investors perceive newly streamlined and more focused organizations to be of higher value. They reward divesting companies by expanding their EBITDA multiple by an average of 0.4 Divestitures not only bring internal improvements for companies; they also reward investors. The biggest benefits accrue to those who get both the strategy and the execution right. Those who choose the wrong exit route leave money on the table or, worse, actually destroy value as shareholders punish their mistakesStep by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock