Question: y=4 Question 3, round your answer to three decimal places (15 marks) Suppose that a U.S. financial institution has the following assets and liabilities: Liabilities

y=4

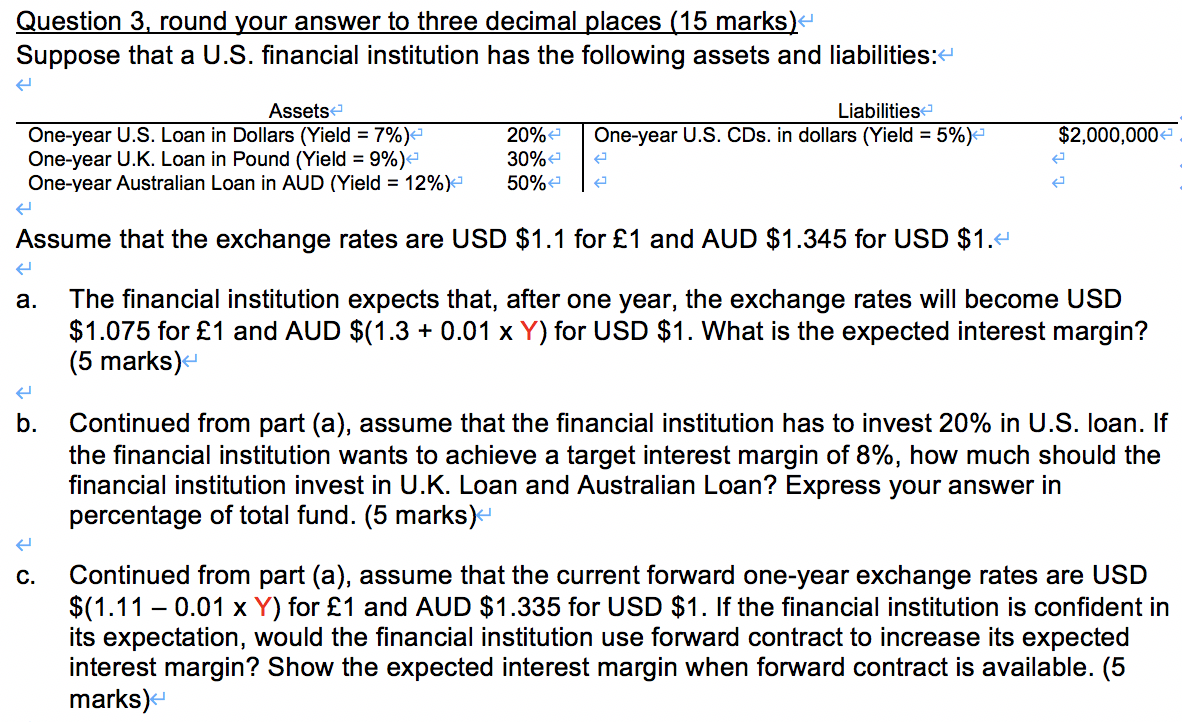

Question 3, round your answer to three decimal places (15 marks) Suppose that a U.S. financial institution has the following assets and liabilities: Liabilities One-year U.S. CDs. in dollars (Yield = 5%) $2,000,000 Assets One-year U.S. Loan in Dollars (Yield = 7%) One-year U.K. Loan in Pound (Yield = 9%) One-year Australian Loan in AUD (Yield = 12%) 20% 30% 50% Assume that the exchange rates are USD $1.1 for 1 and AUD $1.345 for USD $1.4 a. The financial institution expects that, after one year, the exchange rates will become USD $1.075 for 1 and AUD $(1.3 + 0.01 x Y) for USD $1. What is the expected interest margin? (5 marks) & b. Continued from part (a), assume that the financial institution has to invest 20% in U.S. loan. If the financial institution wants to achieve a target interest margin of 8%, how much should the financial institution invest in U.K. Loan and Australian Loan? Express your answer in percentage of total fund. (5 marks) C. Continued from part (a), assume that the current forward one-year exchange rates are USD $(1.11 0.01 x Y) for 1 and AUD $1.335 for USD $1. If the financial institution is confident in its expectation, would the financial institution use forward contract to increase its expected interest margin? Show the expected interest margin when forward contract is available. (5 marks) Question 3, round your answer to three decimal places (15 marks) Suppose that a U.S. financial institution has the following assets and liabilities: Liabilities One-year U.S. CDs. in dollars (Yield = 5%) $2,000,000 Assets One-year U.S. Loan in Dollars (Yield = 7%) One-year U.K. Loan in Pound (Yield = 9%) One-year Australian Loan in AUD (Yield = 12%) 20% 30% 50% Assume that the exchange rates are USD $1.1 for 1 and AUD $1.345 for USD $1.4 a. The financial institution expects that, after one year, the exchange rates will become USD $1.075 for 1 and AUD $(1.3 + 0.01 x Y) for USD $1. What is the expected interest margin? (5 marks) & b. Continued from part (a), assume that the financial institution has to invest 20% in U.S. loan. If the financial institution wants to achieve a target interest margin of 8%, how much should the financial institution invest in U.K. Loan and Australian Loan? Express your answer in percentage of total fund. (5 marks) C. Continued from part (a), assume that the current forward one-year exchange rates are USD $(1.11 0.01 x Y) for 1 and AUD $1.335 for USD $1. If the financial institution is confident in its expectation, would the financial institution use forward contract to increase its expected interest margin? Show the expected interest margin when forward contract is available

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts