You are a senior auditor with Rodriguez & Jones, a small auditing firm located in Canterbury, an

Fantastic news! We've Found the answer you've been seeking!

Question:

You are a senior auditor with Rodriguez & Jones, a small auditing firm located in Canterbury, an eastern suburb of Melbourne, Victoria. Your team has been assigned to the audit of a new client, Miller’s Merchandise, for the year ended 30th June 2021. Miller’s Merchandise is a Deepdene-based wholesaler offering for sale everything from baby food and beverages, to snacks and vegetables, and everything in between.

You are planning the audit of accounts payable, where preparatory work has revealed the following:

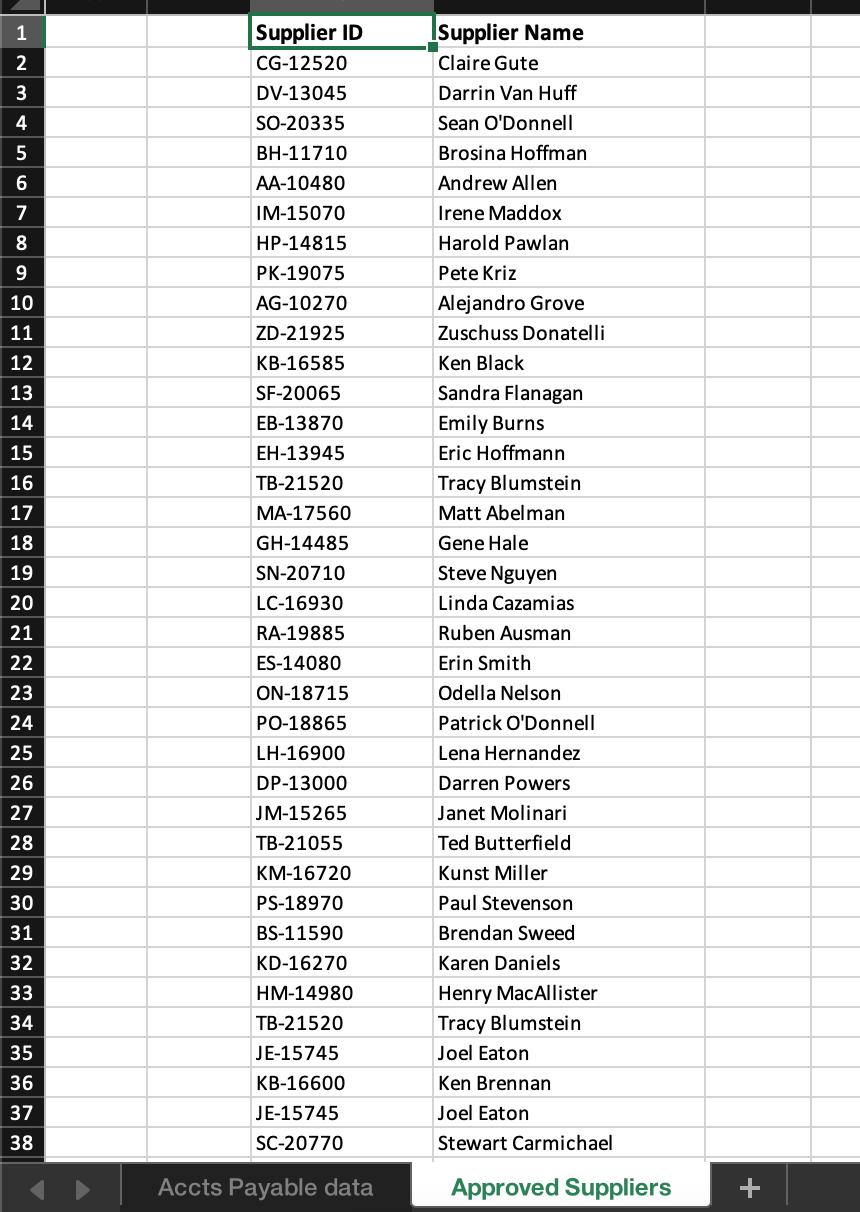

- Miller’s Merchandise purchases its stock from a list of approved suppliers, with purchase orders processed electronically through a business-to-business ecommerce system. This system uses a fast chain model of supply, with suppliers electronically transmitting their invoices – this automated approach means supplier invoices are credited directly to the accounts payable file of Miller’s Merchandise upon receipt of the purchase order. You are concerned about the impact this might have on the existence assertion.

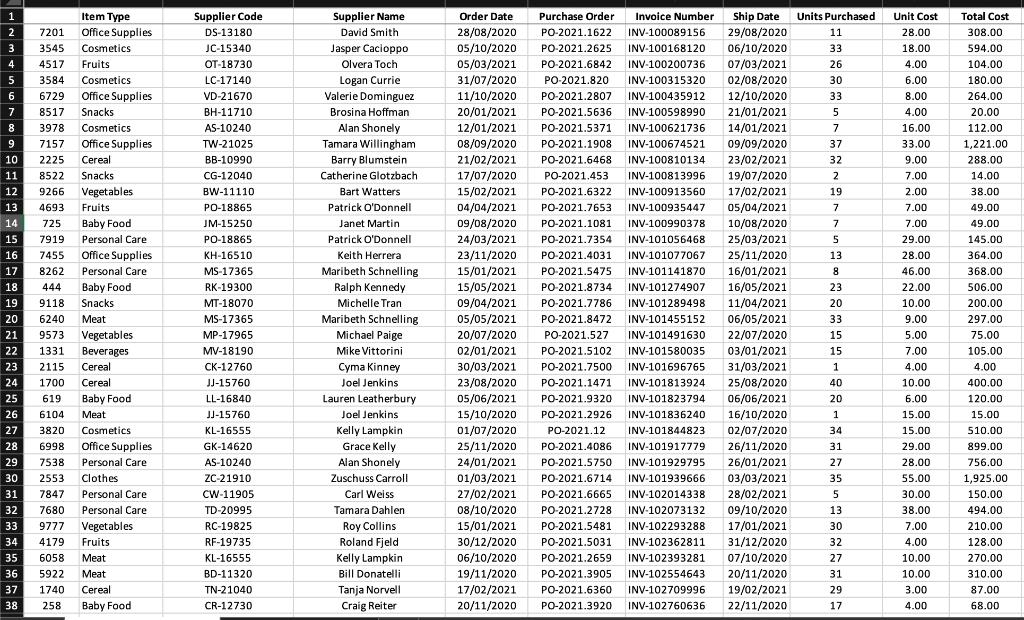

- A key control to safeguard the Valuation and Allocation assertion, is the use of key entry validation – an IT control whereby the Number of Units Purchased is multiplied by the Unit Cost, and compared with the Total Cost as per the supplier’s invoice.

- As is always the case with accounts payable and purchases, you are have flagged the need to investigate the risk associated with the completeness assertion.

- As Miller’s Merchandise operates both in a B2B and B2C environments, you need to test the security and operation of these systems. You are concerned there may be some overlap, thereby putting the classification assertion at risk.

- The owner of Miller’s Merchandise (Suzie Miller) owns and operates another business, Brazeele Mottley, out of Broadmeadows. To make most use of the combined purchasing power, Suzie combines purchases for both businesses where possible. This makes you concerned the rights and obligation assertion for Miller’s Merchandise’s accounts payable may be at risk.

- Interrogate the 2020/2021 accounts payable data provided, developing visualizations to identify potential issues to follow up during the audit. Specifically you are required to comment on the following assertions ‘at risk’:

- Existence;

- Valuation and Allocation;

- Completeness;

- Classification;

- Rights and Obligations.

For each of the above:

- Explain what the assertion means as it relates to Miller’s Merchandise;

- Present relevant data visualisations for the assertion being investigated;

- Discussion/Interpretation of Findings/Data Visualisations.

- Discuss the most appropriate audit strategy to adopt when auditing the accounts payable for Miller’s Merchandise.

Expert Answer:

Posted Date: