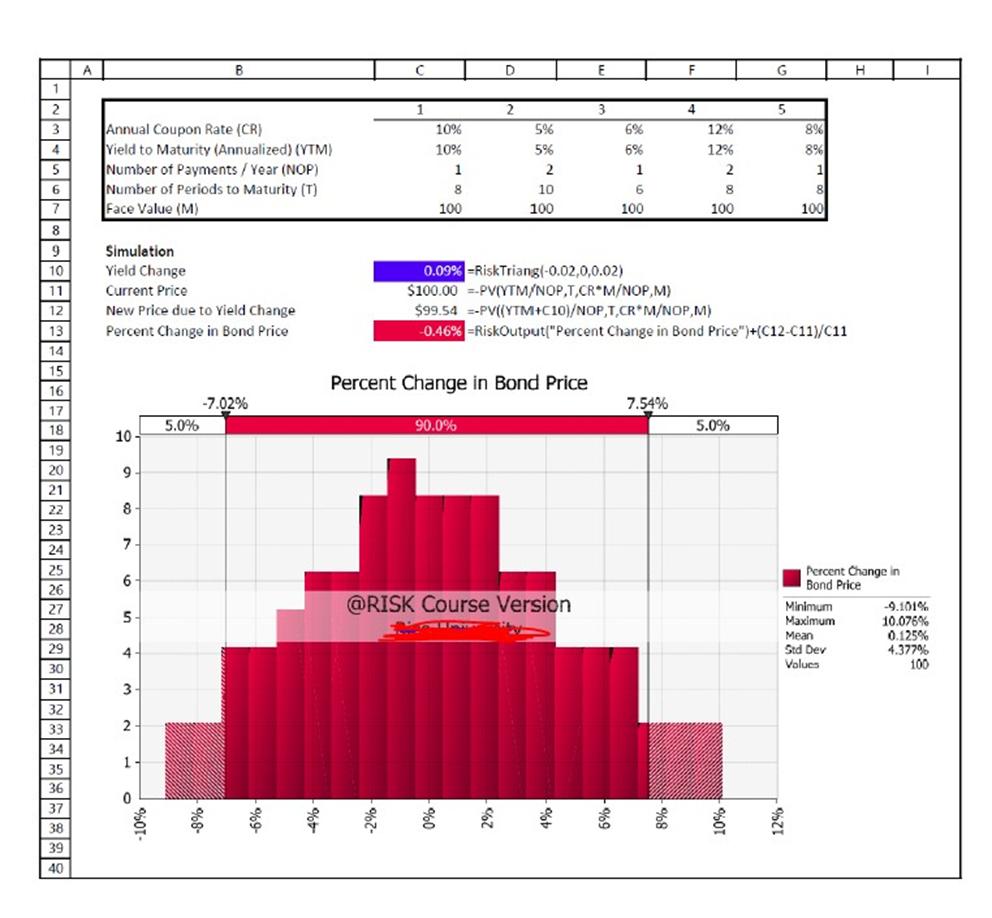

You are an analyst at an asset management fund. The fund currently has five bonds in its

Question:

You are an analyst at an asset management fund. The fund currently has five bonds in its portfolio with the attributes shown below.

The fund’s founder believes that it is most likely that bond yields stay the same, but that it is possible (but very unlikely) that the yields for all of the bonds could drop as much as 200 basis points or rise by as much as 200 basis points. Your colleague has been working on a Monte Carlo analysis of the price risk faced by these potential interest rate moves. Their simulation model and output are on the following page. The simulated data can be found in the Q3 Data tab of the spreadsheet. Unfortunately, they only sent you a screenshot of the model and the data, so you cannot immediately tell which bond they were analyzing (since they named the input cells and all the bonds are currently trading at par).

Annual Coupon Rate (CR) | 1 | 2 | 3 | 4 | 5 |

10% | 5% | 6% | 12% | 8% | |

Yield to Maturity (Annualized) (YTM) | 10% | 5% | 6% | 12% | 8% |

Number of Payments / Year (NOP) | 1 | 2 | 1 | 2 | 1 |

Number of Periods to Maturity (T) | 8 | 10 | 6 | 8 | 8 |

Face Value (M) | 100 | 100 | 100 | 100 | 100 |

Expert Answer:

RISK Data Name Percent Change in Bond Price Yield Change Description Output RiskTriang0020002 Iteration Cell C13 C10 1 401 077 2 024 004 3 515 100 4 0... View the full answer

Financial Management for Decision Makers

ISBN: 978-0138011604

2nd Canadian edition

Authors: Peter Atrill, Paul Hurley