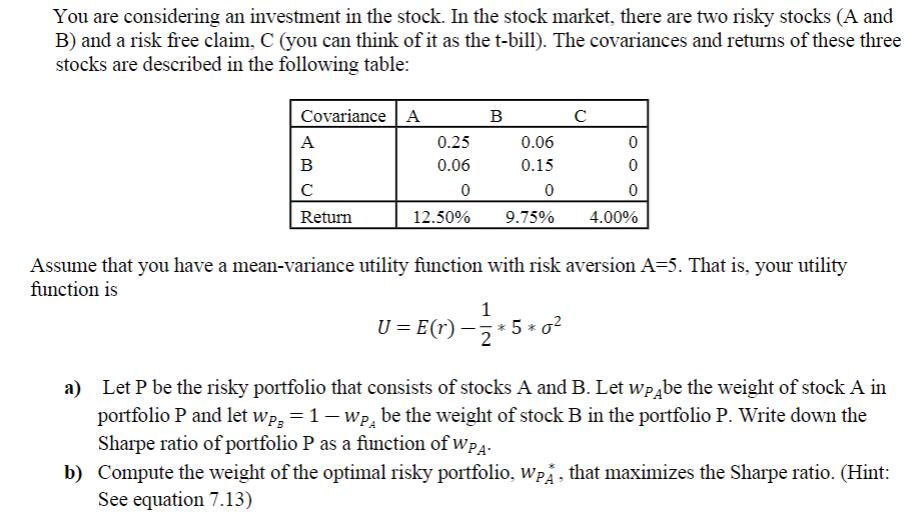

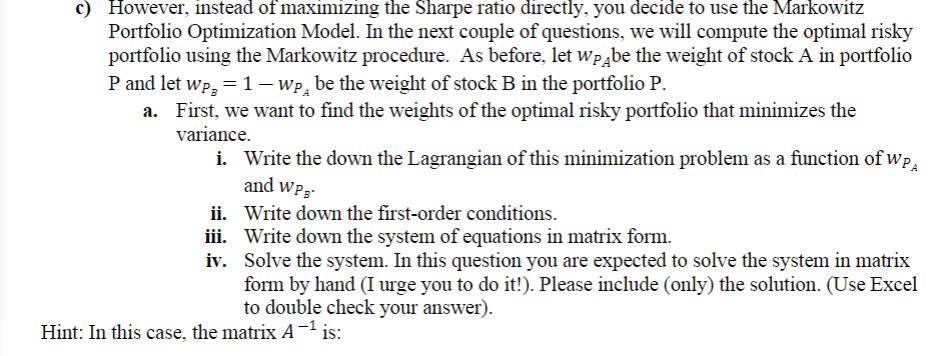

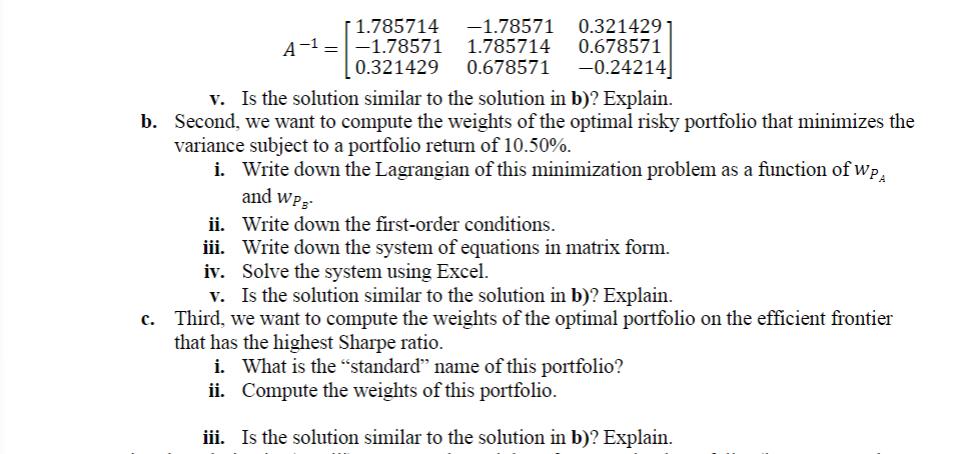

You are considering an investment in the stock. In the stock market, there are two risky...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Financial Analysis with Microsoft Excel

ISBN: 978-1285432274

7th edition

Authors: Timothy R. Mayes, Todd M. Shank

Posted Date: