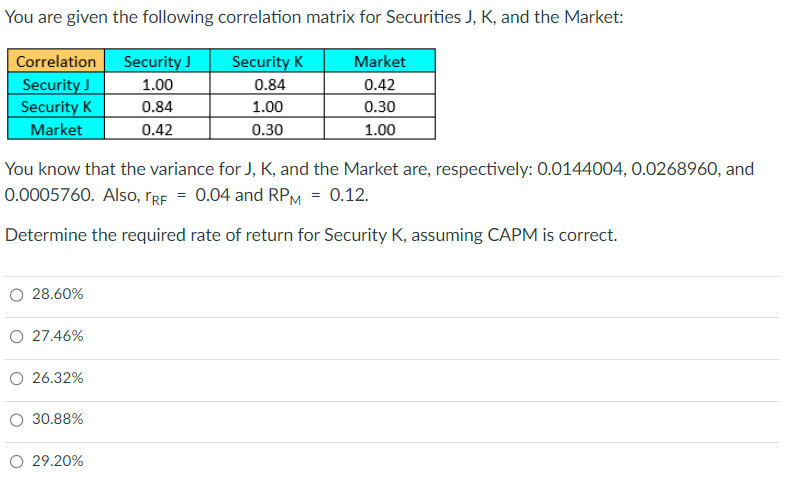

Question: You are given the following correlation matrix for Securities J, K, and the Market: You know that the variance for J, K, and the Market

You are given the following correlation matrix for Securities J, K, and the Market: You know that the variance for J, K, and the Market are, respectively: \\( 0.0144004,0.0268960 \\), and 0.0005760. Also, \\( \\mathrm{r}_{\\mathrm{RF}}=0.04 \\) and \\( \\mathrm{RP}_{\\mathrm{M}}=0.12 \\). Determine the required rate of return for Security \\( \\mathrm{K} \\), assuming CAPM is correct. \28.60 \27.46 \26.32 \30.88 \29.20

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock