You are given the following quote for Eurodollar futures prices on Wednesday: a) John Jones wants

Question:

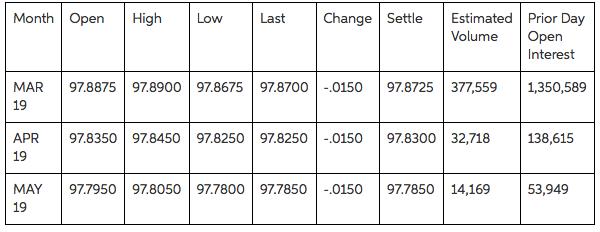

You are given the following quote for Eurodollar futures prices on Wednesday:

a) John Jones wants to hedge a floating rate interest payment in a $2 million loan. The next quarterly interest payment is determined according to a 3-month LIBOR on April 1, 2019. How could he use Eurodollar futures to do it (position, maturity, number of contracts)?

b) If he entered into the futures position at Monday close of 97.865, what would be his cash flow due to marking to market on Tuesday and on Wednesday?

c) What is the value of this futures position (i.e. the value of his futures contracts) on Tuesday?

d) If on April 1, 2019 the 3- month LIBOR turns out to be 2.32% p.a., Eurodollar futures price 97.63 what would be the total cost to John Jones taking into account gains/losses on his hedge, plus the interest payment (disregarding time value of money)?

Expert Answer:

Hedging John Jones interest payment with Eurodollar futures a Position maturity and number of contra... View the full answer

An Introduction to the Mathematics of Financial Derivatives

ISBN: 978-0123846822

3rd edition

Authors: Ali Hirsa, Salih N. Neftci