You are shown the following Markowitz frontier and Capital Market Line, from a UK perspective, when combining

Question:

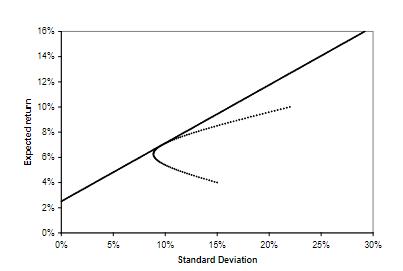

You are shown the following Markowitz frontier and Capital Market Line, from a UK perspective, when combining UK stocks with German stocks. UK stocks have an expected return of 4% and a standard deviation of returns of 15%. German stocks have an expected return of 10% and a standard deviation of returns of 22%. The correlation between UK and German equity returns is -0.5. The UK risk-free rate is 2.5%.

a) You wish to construct the optimal portfolio with a standard deviation of returns of 5%. What is the expected return to this portfolio? Approximately what proportion of your assets should you place in UK equities, German equities and the risk-free asset to achieve the optimal portfolio with this level of risk?

b) How does your answer to part (a) change if you are prepared to have a standard deviation of returns of 20%? You are not permitted to short-sell equity and are unable to borrow.

Expert Answer:

To solve this problem we can use the principles of Modern Portfolio Theory MPT developed by Harry Markowitz MPT suggests that investors can construct ... View the full answer