You are studying Interest Rate Parity, a finance theory that the interest rate differential between foreign...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

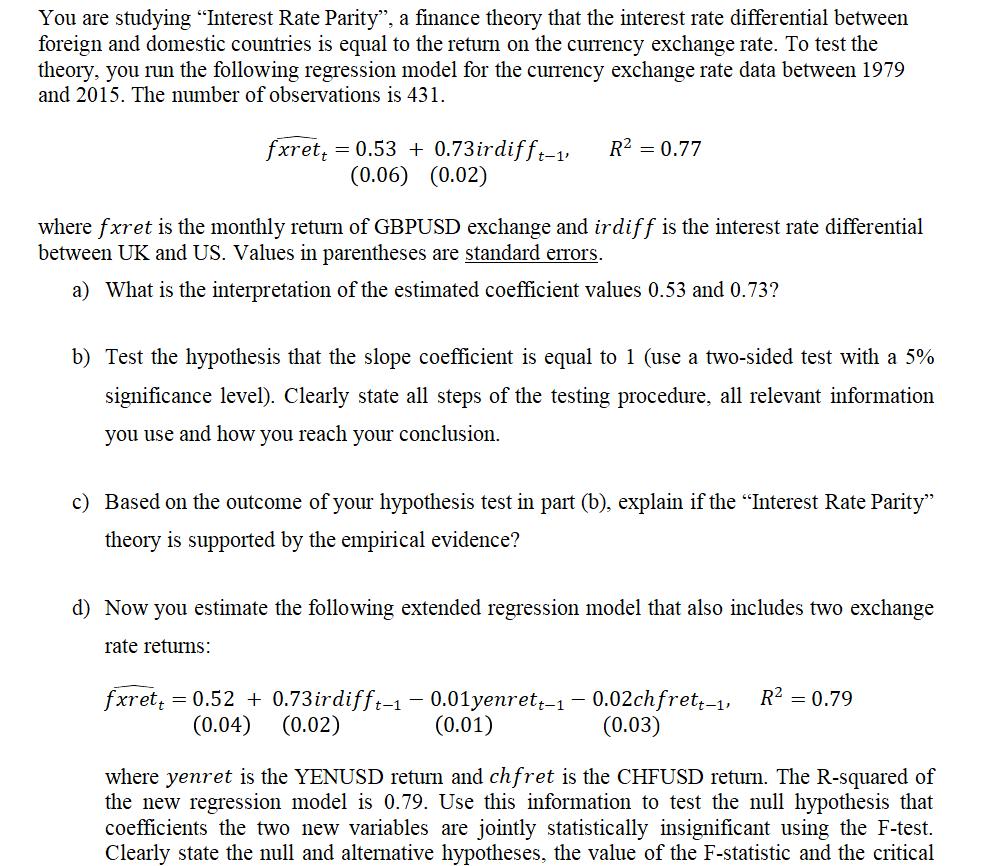

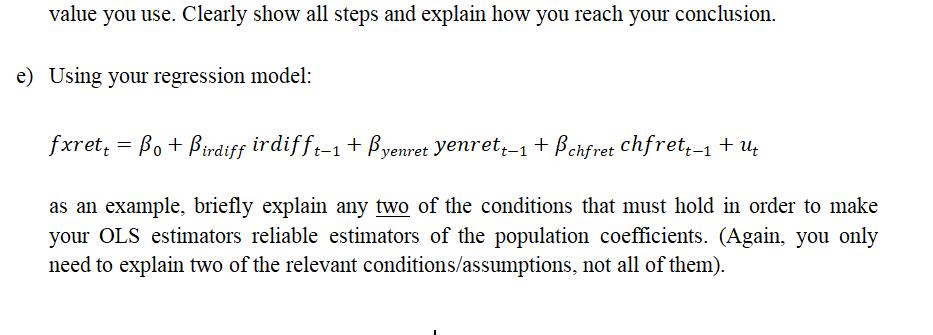

You are studying "Interest Rate Parity", a finance theory that the interest rate differential between foreign and domestic countries is equal to the return on the currency exchange rate. To test the theory, you run the following regression model for the currency exchange rate data between 1979 and 2015. The number of observations is 431. fxret = 0.53 + 0.73irdifft-1 (0.06) (0.02) R² = 0.77 where fxret is the monthly return of GBPUSD exchange and irdiff is the interest rate differential between UK and US. Values in parentheses are standard errors. a) What is the interpretation of the estimated coefficient values 0.53 and 0.73? b) Test the hypothesis that the slope coefficient is equal to 1 (use a two-sided test with a 5% significance level). Clearly state all steps of the testing procedure, all relevant information you use and how you reach your conclusion. c) Based on the outcome of your hypothesis test in part (b), explain if the "Interest Rate Parity" theory is supported by the empirical evidence? d) Now you estimate the following extended regression model that also includes two exchange rate returns: R² = 0.79 fxret = 0.52 +0.73irdifft-1 – 0.01yenrett-10.02chfrett-1, (0.04) (0.02) (0.01) (0.03) where yenret is the YENUSD return and chfret is the CHFUSD return. The R-squared of the new regression model is 0.79. Use this information to test the null hypothesis that coefficients the two new variables are jointly statistically insignificant using the F-test. Clearly state the null and alternative hypotheses, the value of the F-statistic and the critical value you use. Clearly show all steps and explain how you reach your conclusion. e) Using your regression model: fxret = Bo+Birdiff irdifft-1+Byenret yenrett-1 + Bchfret chfrett-1 + Ut as an example, briefly explain any two of the conditions that must hold in order to make your OLS estimators reliable estimators of the population coefficients. (Again, you only need to explain two of the relevant conditions/assumptions, not all of them). You are studying "Interest Rate Parity", a finance theory that the interest rate differential between foreign and domestic countries is equal to the return on the currency exchange rate. To test the theory, you run the following regression model for the currency exchange rate data between 1979 and 2015. The number of observations is 431. fxret = 0.53 + 0.73irdifft-1 (0.06) (0.02) R² = 0.77 where fxret is the monthly return of GBPUSD exchange and irdiff is the interest rate differential between UK and US. Values in parentheses are standard errors. a) What is the interpretation of the estimated coefficient values 0.53 and 0.73? b) Test the hypothesis that the slope coefficient is equal to 1 (use a two-sided test with a 5% significance level). Clearly state all steps of the testing procedure, all relevant information you use and how you reach your conclusion. c) Based on the outcome of your hypothesis test in part (b), explain if the "Interest Rate Parity" theory is supported by the empirical evidence? d) Now you estimate the following extended regression model that also includes two exchange rate returns: R² = 0.79 fxret = 0.52 +0.73irdifft-1 – 0.01yenrett-10.02chfrett-1, (0.04) (0.02) (0.01) (0.03) where yenret is the YENUSD return and chfret is the CHFUSD return. The R-squared of the new regression model is 0.79. Use this information to test the null hypothesis that coefficients the two new variables are jointly statistically insignificant using the F-test. Clearly state the null and alternative hypotheses, the value of the F-statistic and the critical value you use. Clearly show all steps and explain how you reach your conclusion. e) Using your regression model: fxret = Bo+Birdiff irdifft-1+Byenret yenrett-1 + Bchfret chfrett-1 + Ut as an example, briefly explain any two of the conditions that must hold in order to make your OLS estimators reliable estimators of the population coefficients. (Again, you only need to explain two of the relevant conditions/assumptions, not all of them). You are studying "Interest Rate Parity", a finance theory that the interest rate differential between foreign and domestic countries is equal to the return on the currency exchange rate. To test the theory, you run the following regression model for the currency exchange rate data between 1979 and 2015. The number of observations is 431. fxret = 0.53 + 0.73irdifft-1 (0.06) (0.02) R² = 0.77 where fxret is the monthly return of GBPUSD exchange and irdiff is the interest rate differential between UK and US. Values in parentheses are standard errors. a) What is the interpretation of the estimated coefficient values 0.53 and 0.73? b) Test the hypothesis that the slope coefficient is equal to 1 (use a two-sided test with a 5% significance level). Clearly state all steps of the testing procedure, all relevant information you use and how you reach your conclusion. c) Based on the outcome of your hypothesis test in part (b), explain if the "Interest Rate Parity" theory is supported by the empirical evidence? d) Now you estimate the following extended regression model that also includes two exchange rate returns: R² = 0.79 fxret = 0.52 +0.73irdifft-1 – 0.01yenrett-10.02chfrett-1, (0.04) (0.02) (0.01) (0.03) where yenret is the YENUSD return and chfret is the CHFUSD return. The R-squared of the new regression model is 0.79. Use this information to test the null hypothesis that coefficients the two new variables are jointly statistically insignificant using the F-test. Clearly state the null and alternative hypotheses, the value of the F-statistic and the critical value you use. Clearly show all steps and explain how you reach your conclusion. e) Using your regression model: fxret = Bo+Birdiff irdifft-1+Byenret yenrett-1 + Bchfret chfrett-1 + Ut as an example, briefly explain any two of the conditions that must hold in order to make your OLS estimators reliable estimators of the population coefficients. (Again, you only need to explain two of the relevant conditions/assumptions, not all of them). You are studying "Interest Rate Parity", a finance theory that the interest rate differential between foreign and domestic countries is equal to the return on the currency exchange rate. To test the theory, you run the following regression model for the currency exchange rate data between 1979 and 2015. The number of observations is 431. fxret = 0.53 + 0.73irdifft-1 (0.06) (0.02) R² = 0.77 where fxret is the monthly return of GBPUSD exchange and irdiff is the interest rate differential between UK and US. Values in parentheses are standard errors. a) What is the interpretation of the estimated coefficient values 0.53 and 0.73? b) Test the hypothesis that the slope coefficient is equal to 1 (use a two-sided test with a 5% significance level). Clearly state all steps of the testing procedure, all relevant information you use and how you reach your conclusion. c) Based on the outcome of your hypothesis test in part (b), explain if the "Interest Rate Parity" theory is supported by the empirical evidence? d) Now you estimate the following extended regression model that also includes two exchange rate returns: R² = 0.79 fxret = 0.52 +0.73irdifft-1 – 0.01yenrett-10.02chfrett-1, (0.04) (0.02) (0.01) (0.03) where yenret is the YENUSD return and chfret is the CHFUSD return. The R-squared of the new regression model is 0.79. Use this information to test the null hypothesis that coefficients the two new variables are jointly statistically insignificant using the F-test. Clearly state the null and alternative hypotheses, the value of the F-statistic and the critical value you use. Clearly show all steps and explain how you reach your conclusion. e) Using your regression model: fxret = Bo+Birdiff irdifft-1+Byenret yenrett-1 + Bchfret chfrett-1 + Ut as an example, briefly explain any two of the conditions that must hold in order to make your OLS estimators reliable estimators of the population coefficients. (Again, you only need to explain two of the relevant conditions/assumptions, not all of them). You are studying "Interest Rate Parity", a finance theory that the interest rate differential between foreign and domestic countries is equal to the return on the currency exchange rate. To test the theory, you run the following regression model for the currency exchange rate data between 1979 and 2015. The number of observations is 431. fxret = 0.53 + 0.73irdifft-1 (0.06) (0.02) R² = 0.77 where fxret is the monthly return of GBPUSD exchange and irdiff is the interest rate differential between UK and US. Values in parentheses are standard errors. a) What is the interpretation of the estimated coefficient values 0.53 and 0.73? b) Test the hypothesis that the slope coefficient is equal to 1 (use a two-sided test with a 5% significance level). Clearly state all steps of the testing procedure, all relevant information you use and how you reach your conclusion. c) Based on the outcome of your hypothesis test in part (b), explain if the "Interest Rate Parity" theory is supported by the empirical evidence? d) Now you estimate the following extended regression model that also includes two exchange rate returns: R² = 0.79 fxret = 0.52 +0.73irdifft-1 – 0.01yenrett-10.02chfrett-1, (0.04) (0.02) (0.01) (0.03) where yenret is the YENUSD return and chfret is the CHFUSD return. The R-squared of the new regression model is 0.79. Use this information to test the null hypothesis that coefficients the two new variables are jointly statistically insignificant using the F-test. Clearly state the null and alternative hypotheses, the value of the F-statistic and the critical value you use. Clearly show all steps and explain how you reach your conclusion. e) Using your regression model: fxret = Bo+Birdiff irdifft-1+Byenret yenrett-1 + Bchfret chfrett-1 + Ut as an example, briefly explain any two of the conditions that must hold in order to make your OLS estimators reliable estimators of the population coefficients. (Again, you only need to explain two of the relevant conditions/assumptions, not all of them). You are studying "Interest Rate Parity", a finance theory that the interest rate differential between foreign and domestic countries is equal to the return on the currency exchange rate. To test the theory, you run the following regression model for the currency exchange rate data between 1979 and 2015. The number of observations is 431. fxret = 0.53 + 0.73irdifft-1 (0.06) (0.02) R² = 0.77 where fxret is the monthly return of GBPUSD exchange and irdiff is the interest rate differential between UK and US. Values in parentheses are standard errors. a) What is the interpretation of the estimated coefficient values 0.53 and 0.73? b) Test the hypothesis that the slope coefficient is equal to 1 (use a two-sided test with a 5% significance level). Clearly state all steps of the testing procedure, all relevant information you use and how you reach your conclusion. c) Based on the outcome of your hypothesis test in part (b), explain if the "Interest Rate Parity" theory is supported by the empirical evidence? d) Now you estimate the following extended regression model that also includes two exchange rate returns: R² = 0.79 fxret = 0.52 +0.73irdifft-1 – 0.01yenrett-10.02chfrett-1, (0.04) (0.02) (0.01) (0.03) where yenret is the YENUSD return and chfret is the CHFUSD return. The R-squared of the new regression model is 0.79. Use this information to test the null hypothesis that coefficients the two new variables are jointly statistically insignificant using the F-test. Clearly state the null and alternative hypotheses, the value of the F-statistic and the critical value you use. Clearly show all steps and explain how you reach your conclusion. e) Using your regression model: fxret = Bo+Birdiff irdifft-1+Byenret yenrett-1 + Bchfret chfrett-1 + Ut as an example, briefly explain any two of the conditions that must hold in order to make your OLS estimators reliable estimators of the population coefficients. (Again, you only need to explain two of the relevant conditions/assumptions, not all of them). You are studying "Interest Rate Parity", a finance theory that the interest rate differential between foreign and domestic countries is equal to the return on the currency exchange rate. To test the theory, you run the following regression model for the currency exchange rate data between 1979 and 2015. The number of observations is 431. fxret = 0.53 + 0.73irdifft-1 (0.06) (0.02) R² = 0.77 where fxret is the monthly return of GBPUSD exchange and irdiff is the interest rate differential between UK and US. Values in parentheses are standard errors. a) What is the interpretation of the estimated coefficient values 0.53 and 0.73? b) Test the hypothesis that the slope coefficient is equal to 1 (use a two-sided test with a 5% significance level). Clearly state all steps of the testing procedure, all relevant information you use and how you reach your conclusion. c) Based on the outcome of your hypothesis test in part (b), explain if the "Interest Rate Parity" theory is supported by the empirical evidence? d) Now you estimate the following extended regression model that also includes two exchange rate returns: R² = 0.79 fxret = 0.52 +0.73irdifft-1 – 0.01yenrett-10.02chfrett-1, (0.04) (0.02) (0.01) (0.03) where yenret is the YENUSD return and chfret is the CHFUSD return. The R-squared of the new regression model is 0.79. Use this information to test the null hypothesis that coefficients the two new variables are jointly statistically insignificant using the F-test. Clearly state the null and alternative hypotheses, the value of the F-statistic and the critical value you use. Clearly show all steps and explain how you reach your conclusion. e) Using your regression model: fxret = Bo+Birdiff irdifft-1+Byenret yenrett-1 + Bchfret chfrett-1 + Ut as an example, briefly explain any two of the conditions that must hold in order to make your OLS estimators reliable estimators of the population coefficients. (Again, you only need to explain two of the relevant conditions/assumptions, not all of them). You are studying "Interest Rate Parity", a finance theory that the interest rate differential between foreign and domestic countries is equal to the return on the currency exchange rate. To test the theory, you run the following regression model for the currency exchange rate data between 1979 and 2015. The number of observations is 431. fxret = 0.53 + 0.73irdifft-1 (0.06) (0.02) R² = 0.77 where fxret is the monthly return of GBPUSD exchange and irdiff is the interest rate differential between UK and US. Values in parentheses are standard errors. a) What is the interpretation of the estimated coefficient values 0.53 and 0.73? b) Test the hypothesis that the slope coefficient is equal to 1 (use a two-sided test with a 5% significance level). Clearly state all steps of the testing procedure, all relevant information you use and how you reach your conclusion. c) Based on the outcome of your hypothesis test in part (b), explain if the "Interest Rate Parity" theory is supported by the empirical evidence? d) Now you estimate the following extended regression model that also includes two exchange rate returns: R² = 0.79 fxret = 0.52 +0.73irdifft-1 – 0.01yenrett-10.02chfrett-1, (0.04) (0.02) (0.01) (0.03) where yenret is the YENUSD return and chfret is the CHFUSD return. The R-squared of the new regression model is 0.79. Use this information to test the null hypothesis that coefficients the two new variables are jointly statistically insignificant using the F-test. Clearly state the null and alternative hypotheses, the value of the F-statistic and the critical value you use. Clearly show all steps and explain how you reach your conclusion. e) Using your regression model: fxret = Bo+Birdiff irdifft-1+Byenret yenrett-1 + Bchfret chfrett-1 + Ut as an example, briefly explain any two of the conditions that must hold in order to make your OLS estimators reliable estimators of the population coefficients. (Again, you only need to explain two of the relevant conditions/assumptions, not all of them). You are studying "Interest Rate Parity", a finance theory that the interest rate differential between foreign and domestic countries is equal to the return on the currency exchange rate. To test the theory, you run the following regression model for the currency exchange rate data between 1979 and 2015. The number of observations is 431. fxret = 0.53 + 0.73irdifft-1 (0.06) (0.02) R² = 0.77 where fxret is the monthly return of GBPUSD exchange and irdiff is the interest rate differential between UK and US. Values in parentheses are standard errors. a) What is the interpretation of the estimated coefficient values 0.53 and 0.73? b) Test the hypothesis that the slope coefficient is equal to 1 (use a two-sided test with a 5% significance level). Clearly state all steps of the testing procedure, all relevant information you use and how you reach your conclusion. c) Based on the outcome of your hypothesis test in part (b), explain if the "Interest Rate Parity" theory is supported by the empirical evidence? d) Now you estimate the following extended regression model that also includes two exchange rate returns: R² = 0.79 fxret = 0.52 +0.73irdifft-1 – 0.01yenrett-10.02chfrett-1, (0.04) (0.02) (0.01) (0.03) where yenret is the YENUSD return and chfret is the CHFUSD return. The R-squared of the new regression model is 0.79. Use this information to test the null hypothesis that coefficients the two new variables are jointly statistically insignificant using the F-test. Clearly state the null and alternative hypotheses, the value of the F-statistic and the critical value you use. Clearly show all steps and explain how you reach your conclusion. e) Using your regression model: fxret = Bo+Birdiff irdifft-1+Byenret yenrett-1 + Bchfret chfrett-1 + Ut as an example, briefly explain any two of the conditions that must hold in order to make your OLS estimators reliable estimators of the population coefficients. (Again, you only need to explain two of the relevant conditions/assumptions, not all of them). You are studying "Interest Rate Parity", a finance theory that the interest rate differential between foreign and domestic countries is equal to the return on the currency exchange rate. To test the theory, you run the following regression model for the currency exchange rate data between 1979 and 2015. The number of observations is 431. fxret = 0.53 + 0.73irdifft-1 (0.06) (0.02) R² = 0.77 where fxret is the monthly return of GBPUSD exchange and irdiff is the interest rate differential between UK and US. Values in parentheses are standard errors. a) What is the interpretation of the estimated coefficient values 0.53 and 0.73? b) Test the hypothesis that the slope coefficient is equal to 1 (use a two-sided test with a 5% significance level). Clearly state all steps of the testing procedure, all relevant information you use and how you reach your conclusion. c) Based on the outcome of your hypothesis test in part (b), explain if the "Interest Rate Parity" theory is supported by the empirical evidence? d) Now you estimate the following extended regression model that also includes two exchange rate returns: R² = 0.79 fxret = 0.52 +0.73irdifft-1 – 0.01yenrett-10.02chfrett-1, (0.04) (0.02) (0.01) (0.03) where yenret is the YENUSD return and chfret is the CHFUSD return. The R-squared of the new regression model is 0.79. Use this information to test the null hypothesis that coefficients the two new variables are jointly statistically insignificant using the F-test. Clearly state the null and alternative hypotheses, the value of the F-statistic and the critical value you use. Clearly show all steps and explain how you reach your conclusion. e) Using your regression model: fxret = Bo+Birdiff irdifft-1+Byenret yenrett-1 + Bchfret chfrett-1 + Ut as an example, briefly explain any two of the conditions that must hold in order to make your OLS estimators reliable estimators of the population coefficients. (Again, you only need to explain two of the relevant conditions/assumptions, not all of them).

Expert Answer:

Answer rating: 100% (QA)

I can certainly provide some guidance on your financerelated questions a The interpretation of the estimated coefficient values in the regression mode... View the full answer

Related Book For

Posted Date:

Students also viewed these general management questions

-

Explain how currency swaps can hedge foreign exchange operating exposure. What are the accounting advantages of currency swaps?

-

In estimating a regression based on monthly observations from January 1987 to December 2002 inclusive, you find that the coefficient on the independent variable is positive and significant at the...

-

Based on your review of the currency exchange rates between the U.S. dollar and the various European currencies, evaluate in which country a financial institution should invest to maximize its return...

-

The time it takes a cell to divide (called mitosis) is normally distributed with an average time of one hour and a standard deviation of 5 minutes. (a) What is the probability that a cell divides in...

-

Is one factor of production more important than the others? If so, which one? Why?

-

Jimmy's Delicatessen sells large tins of Tom Tucker's Toffee. The deli uses a periodic review system, checking inventory levels every 10 days, at which time an order is placed for more tins. Order...

-

Dr. Walter Sullivan was one of several plastic surgeons in Las Vegas visited by Julie Jones. Jones, an exotic dancer, sought plastic surgery to improve her ability to make money in her profession....

-

Feather Friends, Inc., distributes a high-quality wooden birdhouse that sells for $20 per unit. Variable costs are $8 per unit, and fixed costs total $180,000 per year. Required: Answer the following...

-

(a) Let3+ and 2 = a + bi be complex numbers. Suppose that 7 Argument = 12' find Argument(22). 7-2 (b) Let the map f: CC be defined by f(z) = Find f() if=1+2i. 1 (c) Solve the equation -12 i(9-2),...

-

You are employed by McDowell and Partners, Chartered Accountants (M&P). A new client, Community Finance Corporation (CFC), approached M&P for assistance. Enviro Ltd. (Enviro) has asked CFC for a loan...

-

The Treasury is currently estimating the growth level for Australia. They are concerned about population growth and they have ask you to help them to prepare a report that accounts for an increase in...

-

James purchased a property at 67 Waterworks Road Nundah via contract dated 1 July 2020 and the title transferred on 1 August 2020. The property is two storeys and both the upstairs and downstairs...

-

What is not part of the Strategic Profit Model Framework? Contribution margin Income and balance data sheet Return on investment analysis Impact on return assets

-

If a company purchased equipment then its choices total assets will stay the same. total assets will decrease. total assets will increase.

-

In the consulting industry: For the client: Who, typically, is involved in the project from the client's organization? What roles do they play? What type of time commitment do they need to dedicate?...

-

How should expenses such as repairs be addressed in a property manager's operating budget? a. Allocation of a cash reserve fund b. Establishment of funds for capital expenditures c. Money set aside...

-

Made of high-strength steel, a tie rod is a slender cylindrical structure used to push (compression) and pull (tension) the front tires when the steering wheel is turning (Figure 2). The radius and...

-

Bonus shares can be issued out of revenue reserves. True/False?

-

Graph each equation. 1. y = 3/4x

-

1. What fraction of blood donors have an O blood type? 2. What fraction of blood donors have a B blood type? Distribution of Blood Types in Blood Donors Number of People Blood Type O Rh-positive O...

-

1. Following Exercises have to do with disk storage. Laser Discs have a diameter of 12 centimeters and 20 centimeters. Write the ratio of the smaller diameter to the larger diameter. 2. Floppy disks...

-

A bar in the figure is under the uniformly distributed load \(q\) due to gravity. For a linear elastic material with Young's modulus \(E\) and uniform crosssectional area \(A\), the governing...

-

Calculate the bending moment and the shear force along the cantilevered beam in example 3.7. Compare the results with exact solutions.

-

The twomember plane frame in figure 3.24 is subjected to a single horizontal force \(F\). Both translations and rotational DOFs are fixed at nodes 1 and 3. Also, two members are welded together at...

Study smarter with the SolutionInn App