Question: You are the controller for Bose Inc. and have assembled the following information to support the preparation of journal entries to record Federal income tax

You are the controller for Bose Inc. and have assembled the following information to support the preparation of

journal entries to record Federal income tax expense/benefit for the year ended December 31, YR10.

Information Collected:

1. At January 1, YR10 the company had no deferred tax balances and owed no income tax payable.

2. For the year ended December 31, YR10 the company had no permanent or temporary differences, and therefore GAAP-basis pretax financial income (PFI) and taxable income (TI) are the same.

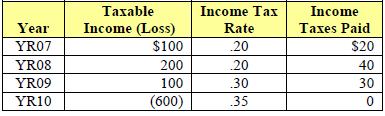

3. Taxable income and the Federal income taxes paid in YR10 and prior years were as follows:

4.Under current Federal income tax law, corporations are permitted to carryback operating losses for 3 years and

carryforward operating losses for 2 years. The company has elected to first use the carryback provisions of the law.

The law limits net operating loss (NOL) deductions to 80% of income reported on the tax return where the NOL deduction is claimed.

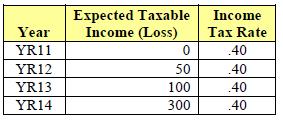

5. Currently enacted tax law specifies the tax rates given in the table below. The table below also discloses, as of December 31, YR10, the taxable income the company estimates it will report for each of the next four years. 6. For the first half of YR10, the company was doing well and earning income. As a result, on June 30, YR10 the company made a tax deposit (payment) and recorded the following journal entry.

6. For the first half of YR10, the company was doing well and earning income. As a result, on June 30, YR10 the company made a tax deposit (payment) and recorded the following journal entry.

Income Tax Payable 30

Cash 30

Starting in the second half of the year, the company’s operations declined and resulted in a loss for the full year.

As a result, no further tax deposits were made.

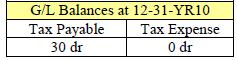

7. At December 31, YR10, the following balances exist in general ledger accounts related to income taxes. At yearend, all other income-tax related accounts have a zero (0) balance.

At yearend, all other income-tax related accounts have a zero (0) balance.

REQUIRED:

YR10

A1. Prepare formal journal entries to record income tax expense/benefit for the year ended 12-31-YR10.

A2. Compute ‘Current’ tax expense/benefit and ‘Deferred’ tax expense/benefit for YR10.

A3. Prepare a partial income statement for the year ended 12-31-YR10 beginning with ‘Operating loss before income tax’.

A4. Prepare the balance sheet presentation as of 12-31-YR10.

YR11

B1. Assume that business activity in YR11 improved significantly and as a result the company reported PFI=TI=$400

in YR11. Also assume the company made a tax deposit during the year and recorded the following journal entry:

Income Tax Payable 20

Cash 20

(To record tax deposit.)

Prepare formal journal entries to record income tax expense/benefit for the year ended 12-31-YR11.

B2. Compute ‘Current’ tax expense/benefit and ‘Deferred’ tax expense/benefit for YR11.

B3. Prepare a partial income statement for the year ended 12-31-YR11 beginning with ‘Operating income before income tax’.

B4. Prepare the balance sheet presentation as of 12-31-YR11.

Year YR07 YR08 YR09 YR10 Taxable Income (Loss) $100 200 100 (600) Income Tax Rate .20 .20 .30 .35 Income Taxes Paid $20 40 30 0

Step by Step Solution

3.35 Rating (155 Votes )

There are 3 Steps involved in it

Journal entry for the tax loss carryforward Dr Deferred tax asset 112 Cr Income tax credit 112 A2 Compute Current tax expensebenefit and Deferred tax expensebenefit for YR10 Tax loss carryback YR07 10... View full answer

Get step-by-step solutions from verified subject matter experts