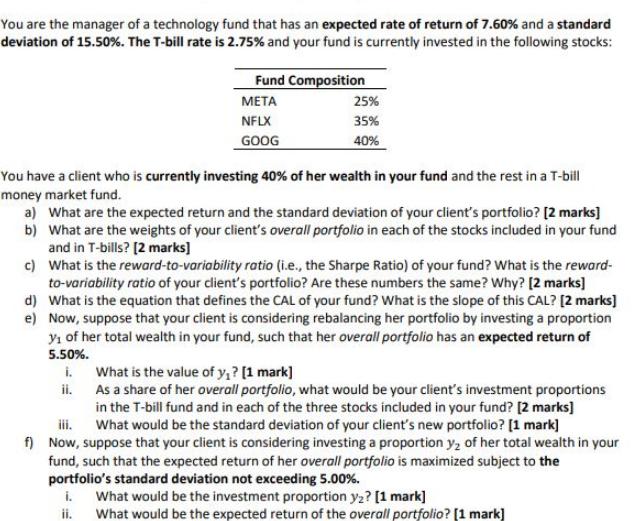

You are the manager of a technology fund that has an expected rate of return of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Solution a The expected return and standard deviation of your clients portfolio are calculated as follows Expected return 040 760 060 275 550 Standard deviation sqrt0402 15502 0602 02 1550 b The weigh... View the full answer

Related Book For

Corporate Finance Core Principles and Applications

ISBN: 978-1259289903

5th edition

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe, Bradford Jordan

Posted Date: