You have been presented with the following abridged financial statements of Honda Ltd and Suzuki Ltd...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

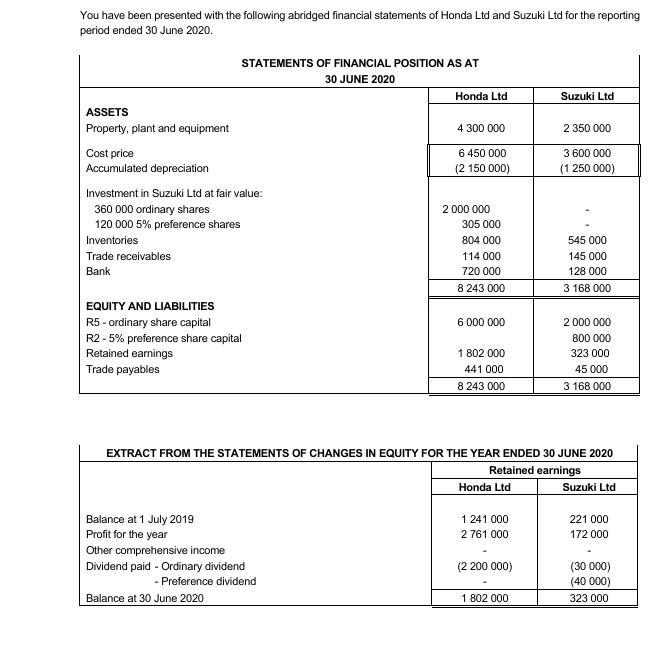

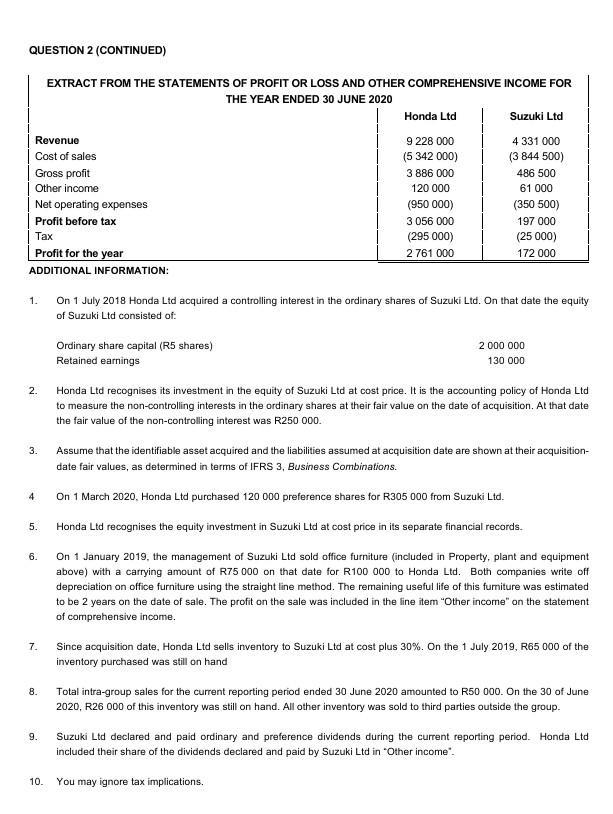

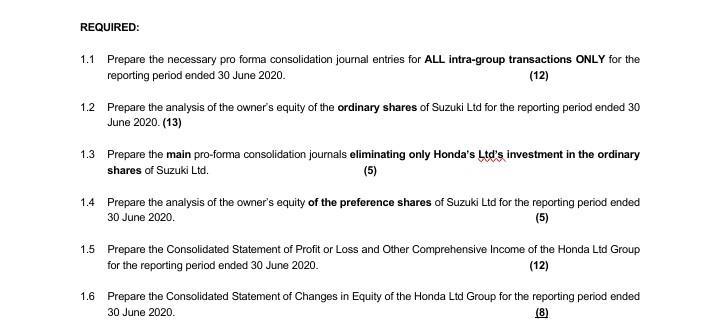

You have been presented with the following abridged financial statements of Honda Ltd and Suzuki Ltd for the reporting period ended 30 June 2020. ASSETS Property, plant and equipment Cost price Accumulated depreciation Investment in Suzuki Ltd at fair value: 360 000 ordinary shares 120 000 5% preference shares Inventories Trade receivables Bank STATEMENTS OF FINANCIAL POSITION AS AT 30 JUNE 2020 EQUITY AND LIABILITIES R5-ordinary share capital R2-5% preference share capital Retained earnings Trade payables Balance at 1 July 2019 Profit for the year Other comprehensive income Honda Ltd Dividend paid - Ordinary dividend - Preference dividend Balance at 30 June 2020 4 300 000 6 450 000 (2 150 000) 2 000 000 305 000 804 000 114 000 720 000 8 243 000 6 000 000 1 802 000 441 000 8 243 000 Honda Ltd EXTRACT FROM THE STATEMENTS OF CHANGES IN EQUITY FOR THE YEAR ENDED 30 JUNE 2020 Retained earnings 1 241 000 2 761 000 Suzuki Ltd (2 200 000) 1 802 000 2 350 000 3 600 000 (1 250 000) 545 000 145 000 128 000 3 168 000 2 000 000 800 000 323 000 45 000 3 168 000 Suzuki Ltd 221 000 172 000 (30 000) (40 000) 323 000 QUESTION 2 (CONTINUED) Revenue Cost of sales Gross profit Other income Net operating expenses Profit before tax Tax Profit for the year ADDITIONAL INFORMATION: 1. 2. 3. 4 5. 6. 7. 8. 9. EXTRACT FROM THE STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 30 JUNE 2020 10. Honda Ltd 9 228 000 (5 342 000) 3 886 000 120 000 (950 000) 3 056 000 (295 000) 2761 000 Ordinary share capital (R5 shares) Retained earnings Suzuki Ltd 4 331 000 (3 844 500) 486 500 61 000 (350 500) 197 000 (25 000) 172 000 On 1 July 2018 Honda Ltd acquired a controlling interest in the ordinary shares of Suzuki Ltd. On that date the equity of Suzuki Ltd consisted of: 2 000 000 130 000 Honda Ltd recognises its investment in the equity of Suzuki Ltd at cost price. It is the accounting policy of Honda Ltd to measure the non-controlling interests in the ordinary shares at their fair value on the date of acquisition. At that date the fair value of the non-controlling interest was R250 000. Assume that the identifiable asset acquired and the liabilities assumed at acquisition date are shown at their acquisition- date fair values, as determined in terms of IFRS 3, Business Combinations. On 1 March 2020, Honda Ltd purchased 120 000 preference shares for R305 000 from Suzuki Ltd. Honda Ltd recognises the equity investment in Suzuki Ltd at cost price in its separate financial records. On 1 January 2019, the management of Suzuki Ltd sold office furniture (included in Property, plant and equipment above) with a carrying amount of R75 000 on that date for R100 000 to Honda Ltd. Both companies write off depreciation on office furniture using the straight line method. The remaining useful life of this furniture was estimated to be 2 years on the date of sale. The profit on the sale was included in the line item "Other income" on the statement of comprehensive income. Since acquisition date, Honda Ltd sells inventory to Suzuki Ltd at cost plus 30%. On the 1 July 2019, R65 000 of the inventory purchased was still on hand Total intra-group sales for the current reporting period ended 30 June 2020 amounted to R50 000. On the 30 of June 2020, R26 000 of this inventory was still on hand. All other inventory was sold to third parties outside the group. Suzuki Ltd declared and paid ordinary and preference dividends during the current reporting period. Honda Ltd included their share of the dividends declared and paid by Suzuki Ltd in "Other income". You may ignore tax implications. REQUIRED: 1.1 Prepare the necessary pro forma consolidation journal entries for ALL intra-group transactions ONLY for the reporting period ended 30 June 2020. (12) 1.2 Prepare the analysis of the owner's equity of the ordinary shares of Suzuki Ltd for the reporting period ended 30 June 2020. (13) 1.3 Prepare the main pro-forma consolidation journals eliminating only Honda's Ltd's investment in the ordinary shares of Suzuki Ltd. (5) 1.4 Prepare the analysis of the owner's equity of the preference shares of Suzuki Ltd for the reporting period ended 30 June 2020. (5) 1.5 Prepare the Consolidated Statement of Profit or Loss and Other Comprehensive Income of the Honda Ltd Group for the reporting period ended 30 June 2020. (12) 1.6 Prepare the Consolidated Statement of Changes in Equity of the Honda Ltd Group for the reporting period ended 30 June 2020. (8) You have been presented with the following abridged financial statements of Honda Ltd and Suzuki Ltd for the reporting period ended 30 June 2020. ASSETS Property, plant and equipment Cost price Accumulated depreciation Investment in Suzuki Ltd at fair value: 360 000 ordinary shares 120 000 5% preference shares Inventories Trade receivables Bank STATEMENTS OF FINANCIAL POSITION AS AT 30 JUNE 2020 EQUITY AND LIABILITIES R5-ordinary share capital R2-5% preference share capital Retained earnings Trade payables Balance at 1 July 2019 Profit for the year Other comprehensive income Honda Ltd Dividend paid - Ordinary dividend - Preference dividend Balance at 30 June 2020 4 300 000 6 450 000 (2 150 000) 2 000 000 305 000 804 000 114 000 720 000 8 243 000 6 000 000 1 802 000 441 000 8 243 000 Honda Ltd EXTRACT FROM THE STATEMENTS OF CHANGES IN EQUITY FOR THE YEAR ENDED 30 JUNE 2020 Retained earnings 1 241 000 2 761 000 Suzuki Ltd (2 200 000) 1 802 000 2 350 000 3 600 000 (1 250 000) 545 000 145 000 128 000 3 168 000 2 000 000 800 000 323 000 45 000 3 168 000 Suzuki Ltd 221 000 172 000 (30 000) (40 000) 323 000 QUESTION 2 (CONTINUED) Revenue Cost of sales Gross profit Other income Net operating expenses Profit before tax Tax Profit for the year ADDITIONAL INFORMATION: 1. 2. 3. 4 5. 6. 7. 8. 9. EXTRACT FROM THE STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 30 JUNE 2020 10. Honda Ltd 9 228 000 (5 342 000) 3 886 000 120 000 (950 000) 3 056 000 (295 000) 2761 000 Ordinary share capital (R5 shares) Retained earnings Suzuki Ltd 4 331 000 (3 844 500) 486 500 61 000 (350 500) 197 000 (25 000) 172 000 On 1 July 2018 Honda Ltd acquired a controlling interest in the ordinary shares of Suzuki Ltd. On that date the equity of Suzuki Ltd consisted of: 2 000 000 130 000 Honda Ltd recognises its investment in the equity of Suzuki Ltd at cost price. It is the accounting policy of Honda Ltd to measure the non-controlling interests in the ordinary shares at their fair value on the date of acquisition. At that date the fair value of the non-controlling interest was R250 000. Assume that the identifiable asset acquired and the liabilities assumed at acquisition date are shown at their acquisition- date fair values, as determined in terms of IFRS 3, Business Combinations. On 1 March 2020, Honda Ltd purchased 120 000 preference shares for R305 000 from Suzuki Ltd. Honda Ltd recognises the equity investment in Suzuki Ltd at cost price in its separate financial records. On 1 January 2019, the management of Suzuki Ltd sold office furniture (included in Property, plant and equipment above) with a carrying amount of R75 000 on that date for R100 000 to Honda Ltd. Both companies write off depreciation on office furniture using the straight line method. The remaining useful life of this furniture was estimated to be 2 years on the date of sale. The profit on the sale was included in the line item "Other income" on the statement of comprehensive income. Since acquisition date, Honda Ltd sells inventory to Suzuki Ltd at cost plus 30%. On the 1 July 2019, R65 000 of the inventory purchased was still on hand Total intra-group sales for the current reporting period ended 30 June 2020 amounted to R50 000. On the 30 of June 2020, R26 000 of this inventory was still on hand. All other inventory was sold to third parties outside the group. Suzuki Ltd declared and paid ordinary and preference dividends during the current reporting period. Honda Ltd included their share of the dividends declared and paid by Suzuki Ltd in "Other income". You may ignore tax implications. REQUIRED: 1.1 Prepare the necessary pro forma consolidation journal entries for ALL intra-group transactions ONLY for the reporting period ended 30 June 2020. (12) 1.2 Prepare the analysis of the owner's equity of the ordinary shares of Suzuki Ltd for the reporting period ended 30 June 2020. (13) 1.3 Prepare the main pro-forma consolidation journals eliminating only Honda's Ltd's investment in the ordinary shares of Suzuki Ltd. (5) 1.4 Prepare the analysis of the owner's equity of the preference shares of Suzuki Ltd for the reporting period ended 30 June 2020. (5) 1.5 Prepare the Consolidated Statement of Profit or Loss and Other Comprehensive Income of the Honda Ltd Group for the reporting period ended 30 June 2020. (12) 1.6 Prepare the Consolidated Statement of Changes in Equity of the Honda Ltd Group for the reporting period ended 30 June 2020. (8)

Expert Answer:

Answer rating: 100% (QA)

11Honda Ltd Dr Cr Inventory 50000 To Suzuki Ltd Inventory Suzuki Ltd Dr Cr Inventory 26000 To Honda ... View the full answer

Related Book For

Accounting and Finance An Introduction

ISBN: 978-1292088297

8th edition

Authors: Peter Atrill, Eddie McLaney

Posted Date:

Students also viewed these accounting questions

-

The directors of Helena Beauty Products Ltd have been presented with the following abridged financial statements: Required: Using six ratios, comment on the profitability (three ratios) and...

-

Old Office Building Karas Investments owns a small office building in Windhoek, from which the company operates. The Windhoek office was purchased on 1 March 2019. Karas Investments decided to move...

-

Exor Ltd manufactures and distributes printing equipment. The company is based in the northern suburbs of Johannesburg. You are provided with the following information for the reporting period ended...

-

Doug, Peter, and Jack have the following capital balances;$150,000, $300,000 and $320,000, respectively. The partners shareprofits and losses 35%, 40%, and 25% respectively. Jones is goingto pay a 2...

-

The Guo Chemical Corporation is considering the purchase of a chemical analysis machine. The purchase of this machine will result in an increase in earnings before interest and taxes of $70,000 per...

-

Evaluate the stream function for a flow with the following velocity components. \[\begin{aligned}& v_{x}=2 x+e^{x} \cos (y) \\& v_{y}=-3 x^{2}-2 y-e^{x} \sin (y)\end{aligned}\] Find the stream...

-

Tsoulos, Tsoulakis and Associates is a small firm of architectural consultants. At 1 July 2024, three architects other than the principals, Tony Tsoulos and Maria Tsoulakis, are employed. The...

-

If a manufacturer sells its laundry detergent to a wholesaler for $2.50, at what price will the wholesaler sell it to a retailer if the wholesaler wants a 15 percent margin based on the selling...

-

Consider a S corporation. The corporation earns $2.5 per share before taxes. The corporate tax rate is 35%, the tax rate on dividend income is 20%, and the personal income tax rate is set at 20%....

-

Given the regression equation Y = 100 + 10X a. What is the change in Y when X changes by +3? b. What is the change in Y when X changes by -4? c. What is the predicted value of Y when X = 12? d. What...

-

Question 30 (1 point) The the form of a cash dividend. is the proportion of earnings that are paid to ordinary shareholders in 1 plus the retention rate retention rate growth rate dividend payout...

-

Suppose you wish to make a vertical leap with the goal of getting your head as high as possible above the ground. At the top of your leap, your arms should be A. Held at your sides. B. Raised above...

-

A \(65 \mathrm{~kg}\) student is walking on a slackline, a length of webbing stretched between two trees. The line stretches and so has a noticeable sag, as shown in Figure P5.8. At the point where...

-

Five forces are applied to a door, as seen from above in Figure Q7.5. For each force, is the torque about the hinge positive, negative, or zero? Fe F Fe Fa Fb FIGURE Q7.5

-

Variation in your apparent weight is desirable when you ride a roller coaster; it makes the ride fun. However, too much variation over a short period of time can be painful. For this reason, the...

-

How large is the "straightening torque"? (You can omit gravitational forces from your calculation; the gravitational torque is much less than this.) A. \(2.3 \times 10^{-7} \mathrm{~N} \cdot...

-

Julie died owning certain interests in a family business, including interests in a partnership and a corporation. Her estate also included a life estate in an irrevocable trust. Julie incurred...

-

Respond to the ethical judgments required based on the following scenarios. Scenario 1. Assume you have collected a sample using MUS and that you have evaluated that sample to calculate a total...

-

A business manufactures refrigerators for domestic use. There are three models: Lo, Mid and Hi. The models, their quality and their price are aimed at different markets. Product costs are computed...

-

Conday and Co. Ltd has been in operation for three years and produces antique reproduction furniture for the export market. The most recent set of financial statements for the business is set out as...

-

Brive plc has the following standards for its only product: Selling price: ..........................................110/unit Direct labour: 1 hour at ........................10.50/hour Direct...

-

In testing the claim that the mean IQ score of statistics students is greater than 100, the alternative hypothesis is expressed as > 100. Decide whether the statement makes sense (or is clearly...

-

In testing a claim about a population mean, a larger z test statistic always results in a larger P-value. Decide whether the statement makes sense (or is clearly true) or does not make sense (or is...

-

A handy mnemonic for interpreting the P-value in a hypothesis test is this: If the P (value) is low, then the null must go.

Study smarter with the SolutionInn App