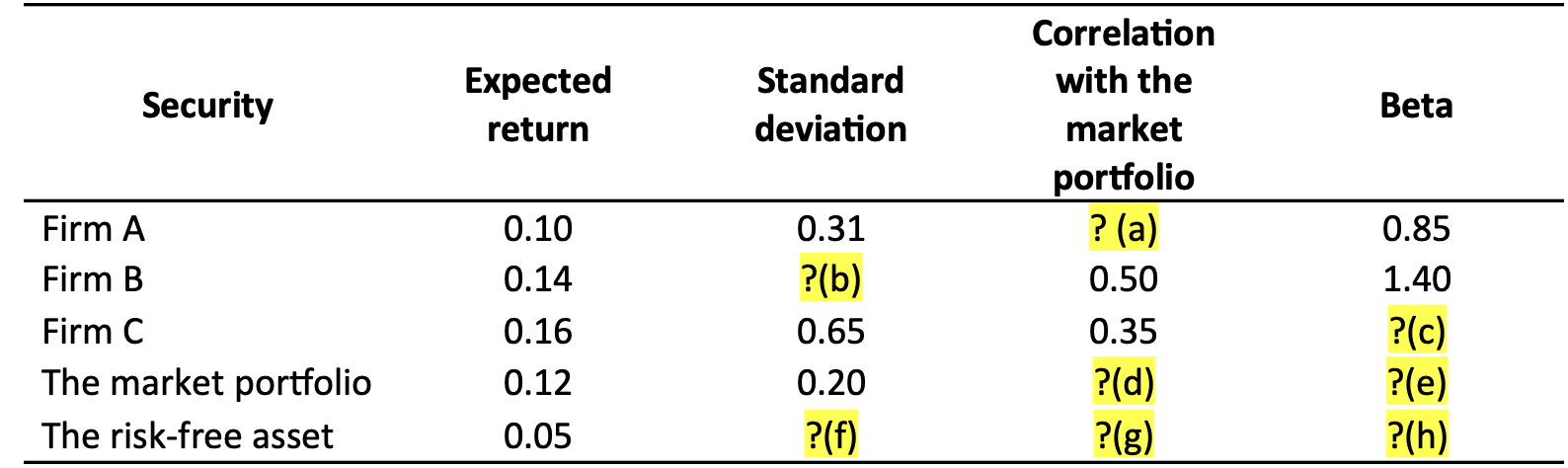

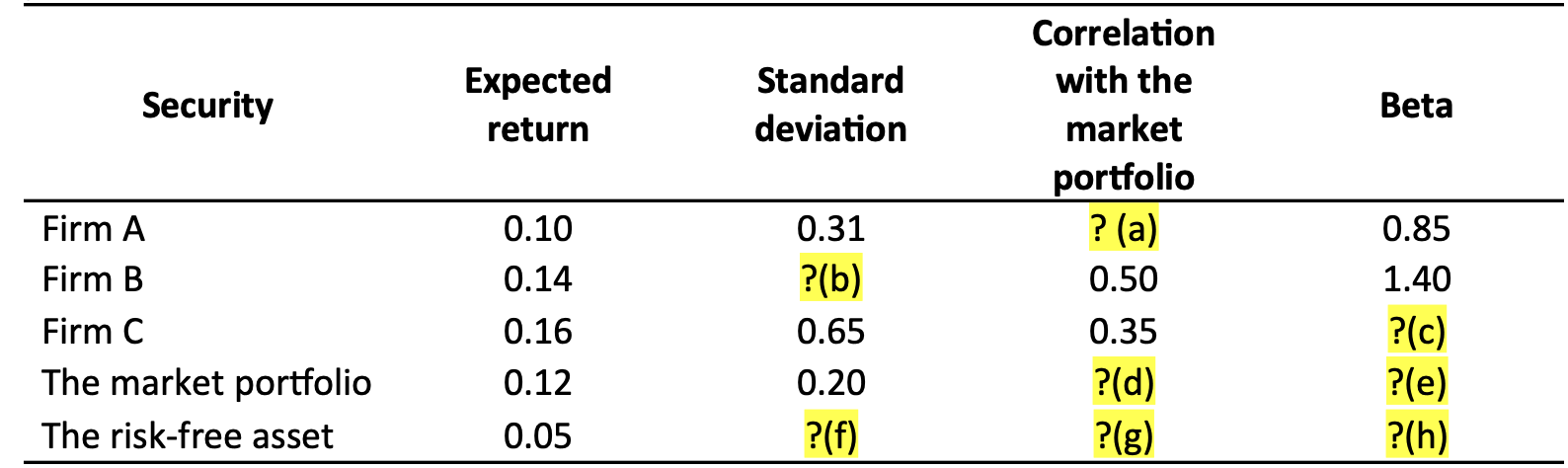

Question: You have been provided with the following data about the securities of three firms, the market portfolio, and the risk-free asset: Security Firm A Firm

You have been provided with the following data about the securities of three firms, the market portfolio, and the risk-free asset:

Security Firm A Firm B Firm C The market portfolio The risk-free asset Expected return 0.10 0.14 0.16 0.12 0.05 Standard deviation 0.31 ?(b) 0.65 0.20 ?(f) Correlation with the market portfolio ? (a) 0.50 0.35 ?(c|) ?(g) Beta 0.85 1.40 ?(C) ?(e) ?(h)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock