You have just had a meeting with a new client, Tom Blake, aged 47. Tom has...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

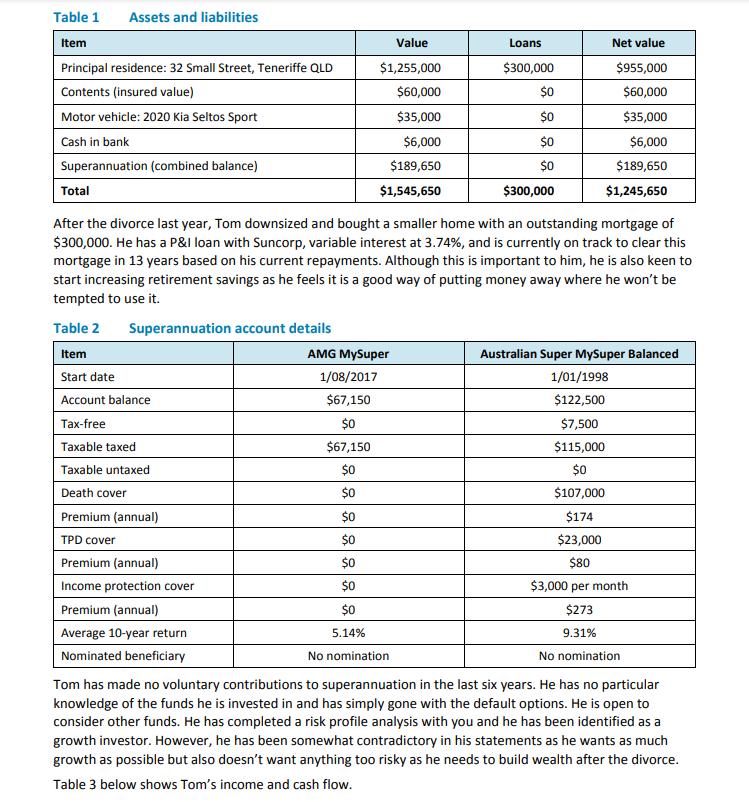

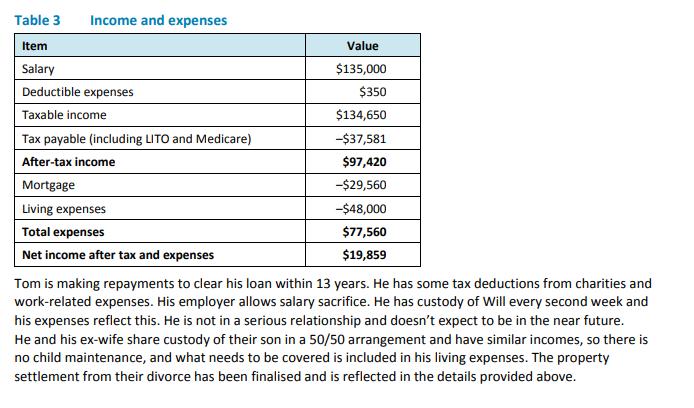

You have just had a meeting with a new client, Tom Blake, aged 47. Tom has recently divorced, and has one child, Will, aged 7. He is determined to stay single and wants to plan for his future and eventual retirement. He has come to see you because he recently read that his super fund, AMG MySuper, was in the news because it had failed some test twice and was now closed to new members. He joined the fund about four years ago when he started his current job, because a friend recommended it. He has a second super fund that he has not contributed to in a few years which he kept because he had insurance cover through the fund and he couldn't be bothered changing it at the time. Now he wants to know what fund would actually suit him best. On further discussion with him about his goals, he nominated 60 as his preferred retirement age and $65,000 as an income he thought should be enough to provide him with a decent lifestyle with some travel. He has just had a pay increase and felt that he should look more closely at what he is doing with the extra money. You have discussed his financial goals with him and have agreed that his objectives at the moment are to: • choose the best superannuation fund for the long term to maximise growth • find a fund that offers decent returns for reasonable fees • get financially back on track after the divorce • reduce tax and increase long-term savings • make his financial arrangements less complex • clear his home loan before he turns 60 when he hopes to retire or reduce his work hours • financially protect himself and his son Will in the event that he passes away prematurely or suffers a serious illness or accident • retire at age 60 with $65,000 in after tax-income that lasts for life. Assets, liabilities and cash flow This section sets out Tom's relevant assets and liabilities, as well as his current cash flow. Table 1 below shows his assets and liabilities of relevance and Table 2 below details his current superannuation. Table 1 Assets and liabilities Item Principal residence: 32 Small Street, Teneriffe QLD Contents (insured value) Motor vehicle: 2020 Kia Seltos Sport Cash in bank Superannuation (combined balance) Value $1,255,000 $60,000 $35,000 $6,000 $189,650 $1,545,650 Table 2 Superannuation account details Item Start date Account balance Tax-free Taxable taxed Taxable untaxed Death cover Premium (annual) TPD cover Premium (annual) Income protection cover Premium (annual) Average 10-year return Nominated beneficiary Loans $300,000 AMG MySuper 1/08/2017 $67,150 $0 $67,150 $0 $0 $0 $0 $0 $0 $0 5.14% No nomination $0 $0 $0 $0 $300,000 Total After the divorce last year, Tom downsized and bought a smaller home with an outstanding mortgage of $300,000. He has a P&I loan with Suncorp, variable interest at 3.74%, and is currently on track to clear this mortgage in 13 years based on his current repayments. Although this is important to him, he is also keen to start increasing retirement savings as he feels it is a good way of putting money away where he won't be tempted to use it. Net value $955,000 $60,000 $35,000 $6,000 $189,650 $1,245,650 Australian Super MySuper Balanced 1/01/1998 $122,500 $7,500 $115,000 $0 $107,000 $174 $23,000 $80 $3,000 per month $273 9.31% No nomination Tom has made no voluntary contributions to superannuation in the last six years. He has no particular knowledge of the funds he is invested in and has simply gone with the default options. He is open to consider other funds. He has completed a risk profile analysis with you and he has been identified as a growth investor. However, he has been somewhat contradictory in his statements as he wants as much growth as possible but also doesn't want anything too risky as he needs to build wealth after the divorce. Table 3 below shows Tom's income and cash flow. Table 3 Income and expenses Item Salary Deductible expenses Taxable income Tax payable (including LITO and Medicare) After-tax income Mortgage Living expenses Total expenses Net income after tax and expenses Value $135,000 $350 $134,650 -$37,581 $97,420 -$29,560 -$48,000 $77,560 $19,859 Tom is making repayments to clear his loan within 13 years. He has some tax deductions from charities and work-related expenses. His employer allows salary sacrifice. He has custody of Will every second week and his expenses reflect this. He is not in a serious relationship and doesn't expect to be in the near future. He and his ex-wife share custody of their son in a 50/50 arrangement and have similar incomes, so there is no child maintenance, and what needs to be covered is included in his living expenses. The property settlement from their divorce has been finalised and is reflected in the details provided above. Question 1 Prepare a strategy paper for the clients (40 marks | Word limit: 2,000 words) Refer to Case study A: Tom Blake and prepare a strategy paper for the client regarding his superannuation and retirement only. A strategy paper is used to set out and explain the options available for a client and the best option(s) for them based on their needs, wants, goals, constraints and limitations. Your strategy paper must address the following: (a) Summarise the client's current position: • key goals and objectives (3 marks) • current financial situation and outcomes based on Tom's current situation (4 marks) • constraints and limitations in being able to meet goals. (3 marks) (b) (c) Identify and consider two (2) different accumulation strategies, showing how they meet the client's goals, with supporting calculations/data where relevant. (10 marks for each strategy - total 20 marks) Given the two (2) different strategies you have outlined in part (b) above, provide a statement outlining which strategy you would recommend that meet Tom's needs and objectives. You should explain why you prefer one strategy over the other. (10 marks) You have just had a meeting with a new client, Tom Blake, aged 47. Tom has recently divorced, and has one child, Will, aged 7. He is determined to stay single and wants to plan for his future and eventual retirement. He has come to see you because he recently read that his super fund, AMG MySuper, was in the news because it had failed some test twice and was now closed to new members. He joined the fund about four years ago when he started his current job, because a friend recommended it. He has a second super fund that he has not contributed to in a few years which he kept because he had insurance cover through the fund and he couldn't be bothered changing it at the time. Now he wants to know what fund would actually suit him best. On further discussion with him about his goals, he nominated 60 as his preferred retirement age and $65,000 as an income he thought should be enough to provide him with a decent lifestyle with some travel. He has just had a pay increase and felt that he should look more closely at what he is doing with the extra money. You have discussed his financial goals with him and have agreed that his objectives at the moment are to: • choose the best superannuation fund for the long term to maximise growth • find a fund that offers decent returns for reasonable fees • get financially back on track after the divorce • reduce tax and increase long-term savings • make his financial arrangements less complex • clear his home loan before he turns 60 when he hopes to retire or reduce his work hours • financially protect himself and his son Will in the event that he passes away prematurely or suffers a serious illness or accident • retire at age 60 with $65,000 in after tax-income that lasts for life. Assets, liabilities and cash flow This section sets out Tom's relevant assets and liabilities, as well as his current cash flow. Table 1 below shows his assets and liabilities of relevance and Table 2 below details his current superannuation. Table 1 Assets and liabilities Item Principal residence: 32 Small Street, Teneriffe QLD Contents (insured value) Motor vehicle: 2020 Kia Seltos Sport Cash in bank Superannuation (combined balance) Value $1,255,000 $60,000 $35,000 $6,000 $189,650 $1,545,650 Table 2 Superannuation account details Item Start date Account balance Tax-free Taxable taxed Taxable untaxed Death cover Premium (annual) TPD cover Premium (annual) Income protection cover Premium (annual) Average 10-year return Nominated beneficiary Loans $300,000 AMG MySuper 1/08/2017 $67,150 $0 $67,150 $0 $0 $0 $0 $0 $0 $0 5.14% No nomination $0 $0 $0 $0 $300,000 Total After the divorce last year, Tom downsized and bought a smaller home with an outstanding mortgage of $300,000. He has a P&I loan with Suncorp, variable interest at 3.74%, and is currently on track to clear this mortgage in 13 years based on his current repayments. Although this is important to him, he is also keen to start increasing retirement savings as he feels it is a good way of putting money away where he won't be tempted to use it. Net value $955,000 $60,000 $35,000 $6,000 $189,650 $1,245,650 Australian Super MySuper Balanced 1/01/1998 $122,500 $7,500 $115,000 $0 $107,000 $174 $23,000 $80 $3,000 per month $273 9.31% No nomination Tom has made no voluntary contributions to superannuation in the last six years. He has no particular knowledge of the funds he is invested in and has simply gone with the default options. He is open to consider other funds. He has completed a risk profile analysis with you and he has been identified as a growth investor. However, he has been somewhat contradictory in his statements as he wants as much growth as possible but also doesn't want anything too risky as he needs to build wealth after the divorce. Table 3 below shows Tom's income and cash flow. Table 3 Income and expenses Item Salary Deductible expenses Taxable income Tax payable (including LITO and Medicare) After-tax income Mortgage Living expenses Total expenses Net income after tax and expenses Value $135,000 $350 $134,650 -$37,581 $97,420 -$29,560 -$48,000 $77,560 $19,859 Tom is making repayments to clear his loan within 13 years. He has some tax deductions from charities and work-related expenses. His employer allows salary sacrifice. He has custody of Will every second week and his expenses reflect this. He is not in a serious relationship and doesn't expect to be in the near future. He and his ex-wife share custody of their son in a 50/50 arrangement and have similar incomes, so there is no child maintenance, and what needs to be covered is included in his living expenses. The property settlement from their divorce has been finalised and is reflected in the details provided above. Question 1 Prepare a strategy paper for the clients (40 marks | Word limit: 2,000 words) Refer to Case study A: Tom Blake and prepare a strategy paper for the client regarding his superannuation and retirement only. A strategy paper is used to set out and explain the options available for a client and the best option(s) for them based on their needs, wants, goals, constraints and limitations. Your strategy paper must address the following: (a) Summarise the client's current position: • key goals and objectives (3 marks) • current financial situation and outcomes based on Tom's current situation (4 marks) • constraints and limitations in being able to meet goals. (3 marks) (b) (c) Identify and consider two (2) different accumulation strategies, showing how they meet the client's goals, with supporting calculations/data where relevant. (10 marks for each strategy - total 20 marks) Given the two (2) different strategies you have outlined in part (b) above, provide a statement outlining which strategy you would recommend that meet Tom's needs and objectives. You should explain why you prefer one strategy over the other. (10 marks)

Expert Answer:

Answer rating: 100% (QA)

Strategy Paper for Tom Blakes Superannuation and Retirement a Current Position Key Goals and Objectives Choose the best superannuation fund for the long term to maximize growth Find a fund that offers ... View the full answer

Related Book For

Posted Date:

Students also viewed these finance questions

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

A double-ended queue or deque (pronounced "deck") is a collection that is a combination of a stack and a queue. Write a class Deque that uses a linked list to implement the following API: public...

-

What is the price/earnings ratio, and how is it calculated? Discuss in detail.

-

Do strengths always receive higher ratings than weaknesses?

-

An electron and a proton are fired in opposite directions, and at the instant they are nearest each other, their separation distance is \(3.0 \mu \mathrm{m}\) (Figure P28.84). At that instant, the...

-

Net Play Manufacturing uses a job order cost system in each of its three manufacturing departments. Manufacturing overhead is applied to jobs on the basis of direct labor cost in Department A, direct...

-

6. An igloo, a hemispherical enclosure built of ice (1.67 J/m-sC), has as inner radius of 2.50m. The thickness of the ice is 0.5m. At what rate must thermal energy be generated to maintain the air...

-

Severo S.A. of Sao Paulo, Brazil, is organized into two divisions. The companys contribution format segmented income statement (in terms of the Brazilian currency, the real, R) for last month is...

-

7. The annual annuity stream of payments with the same present value as a p cost. the project's incremental sunk opportunity equivalent annual a. b. C. d. 8. A cost that has already been paid, or the...

-

1) Brown coal contains solid carbonaceous material, non-combustible minerals (ash) as well as locked in water. Victorian lignite contains 52% of moisture and 3% of ash. Elemental analysis revealed a...

-

Sally Burns meets with her physician complaining of a headache, sore throat, and coughing. She has a group health insurance through her employer which has a co-payment of $100.00. She pays the...

-

Perdon Corporation manufactures safes-large mobile safes, and large walk-in stationary bank safes. As part of its annual budgeting process, Perdon is analyzing the profitability of its two products....

-

Private nonprofit four - year colleges charge, on average, $ 2 6 , 7 7 3 per year in tuition and fees. The standard deviation is $ 6 , 7 1 3 . Assume the distribution is normal. Let X be the cost for...

-

"Lawsuit Claims Nightclub Fired Waitresses for Being Too Short" was a headline of Fox5 News New York. According to the report, two women filed suit against their previous employer, a prominent New...

-

Required 1. How much is the carrying amount of the lease liability on December 31, 2022? 2. Assuming that the asset will revert to the lessor at the end of the lease term and all improvements were...

-

Perform the operation by first converting the numerator and denominator to scientific notation. Write the answer in scientific notation. 7,200,00/0.000009

-

Mowers Unlimited Inc. (MUI) manufactures and distributes lawnmowers. To promote the sale of a new mower type, MUI offered a mail-in rebate to retail purchasers of $50 per mower. Pertinent details...

-

The date is February 26, 2018, and you are in the process of making adjusting entries for Bellevue Company for the year ended December 31, 2017. In your analysis of accounts receivable and bad debts,...

-

Refer to the information in problem 6-22. Assume that the company uses a periodic inventory system and counts inventory at the end of each month. Data from 6-22. Required: Using the LIFO cost method...

-

Travis Mordica asks, Since share dividends dont change anything, why declare them? What is your answer to Travis?

-

The following equity accounts are in the ledger of Eudaley Group at December 31, 2025. Instructions Prepare the equity section of the statement of financial position at December 31, 2025. Share...

-

The equity section of Atrio Ltd. showed the following: share premium 6,101, share capitalordinary 925, share capitalpreference 58, retained earnings 7,420, and treasury shares 2,828. (All amounts are...

Study smarter with the SolutionInn App