You have the privilege of serving on the board of directors for a local not-for-profit that works

Question:

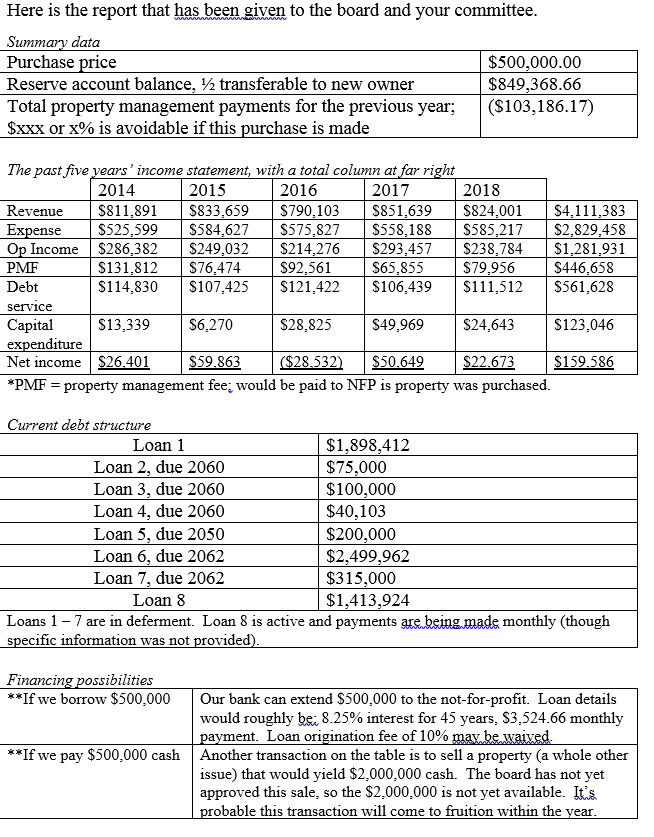

You have the privilege of serving on the board of directors for a local not-for-profit that works to prevent homelessness. As a board member, it is your fiduciary duty to ensure the sustainability of the organization; poor judgment on your part could spell misfortunate for the residents. The not-for-profit owns and manages seven locations throughout your city which are used to house those less fortunate. Each location is its own entity for accounting purposes?that is, it generates its own revenue (per 8 housing vouchers and resident rent payment) and records its own expenditures. Each entity also undergoes its own audit. There is a central accounting office, and consolidated financial statements are compiled annually after all seven "entity" and "parent" audits are completed.

At a recent board meeting, the executive director presented the board with an opportunity to expand the organization's reach. Essentially, to acquire a building already zoned and used for affordable housing. The building would increase the number of clients the not-for-profit accommodates (this is great news as the board's annual goal is to increase the number of residents).

In order for the board to make a decision, the executive director and controller compiled relevant financial data (presented on page two)to the best of their ability. The real trick to the decision is deciding which piece of financial data is relevant (if it's relevant at all) and also discerning when the data is/will be relevant. Because of the substantial purchase price, due diligence should be exercised to a fault. The board chair has decided to establish a special committee to take a deep dive into the financial data, and give a recommendation to the entire board at their next meeting. As an accounting professional, you've been volunteered to take part in the committee.

As a committee member, it will be your duty to peruse the above data and convert it to useable information (to the best ofyourability). Remember, not everyone on the board, and that will read your memo, is accounting-savvy. And, don't necessarily worry about every piece of data?that is,keep your eyes on the forest, not the trees.

Part I

Your deliverable for the next board meeting is a memo outlining your committee's findings. In particular (and anything else you believe is necessary):

Expert Answer:

Here is a memo outlining my committees findings regarding the proposed property purchase To Board of Directors From Special Committee on Property Purc... View the full answer

Advanced Financial Accounting

ISBN: 978-0137030385

6th edition

Authors: Thomas Beechy, Umashanker Trivedi, Kenneth MacAulay