Question: You know that the cash flow statement classifies cash receipts and cash payments as operating, investing, and financing activities. Before preparing the cash flow statement,

- You know that the cash flow statement classifies cash receipts and cash payments as operating, investing, and financing activities. Before preparing the cash flow statement, accounting data must be analyzed to locate transactions in both the cash account and other locations. After the transactions have been located, it should be determined whether each one affects operating, investing, or financing cash flow. Last, whether the transaction results in a cash inflow or outflow must be ascertained. Accountants consider this statement to be foundational for a business to continuously operate.

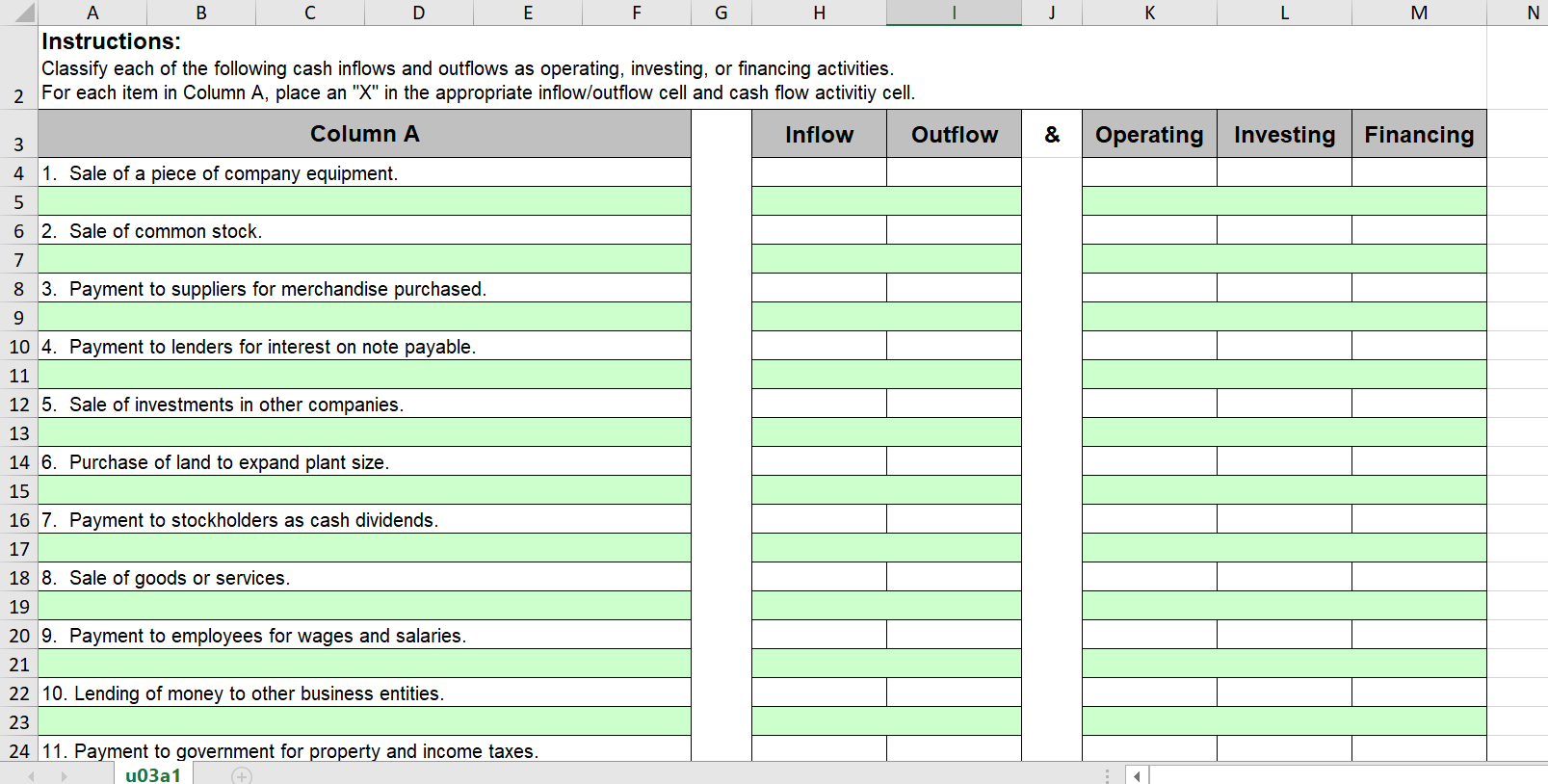

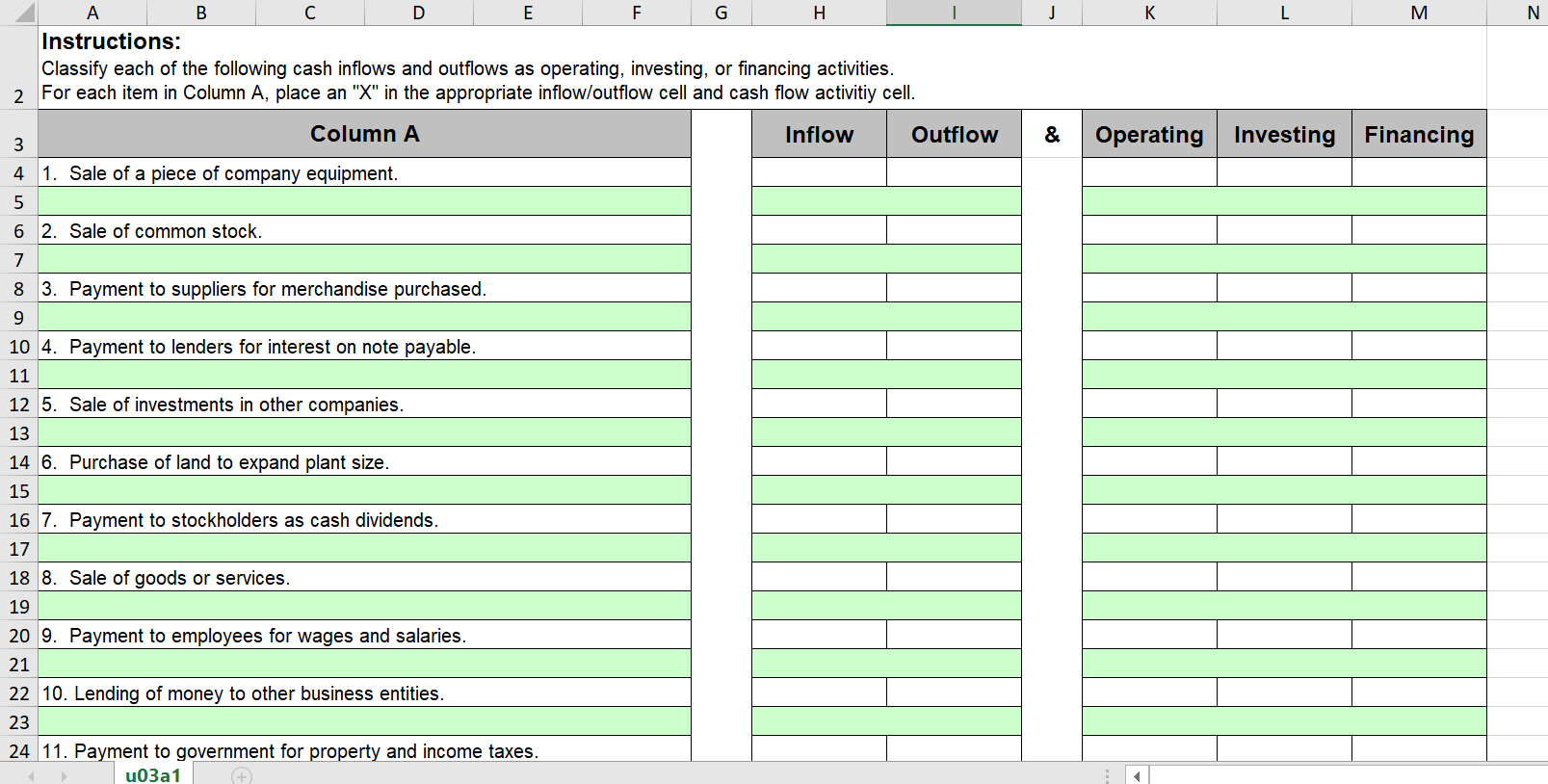

- For this part of the assessment, use the Assessment 3, Part 1 Template to classify each of the following cash inflows and outflows as operating, investing, or financing activities:

- Sale of a piece of company equipment.

- Sale of common stock.

- Payment to suppliers for merchandise purchased.

- Payment to lenders for interest on note payable.

- Sale of investments in other companies.

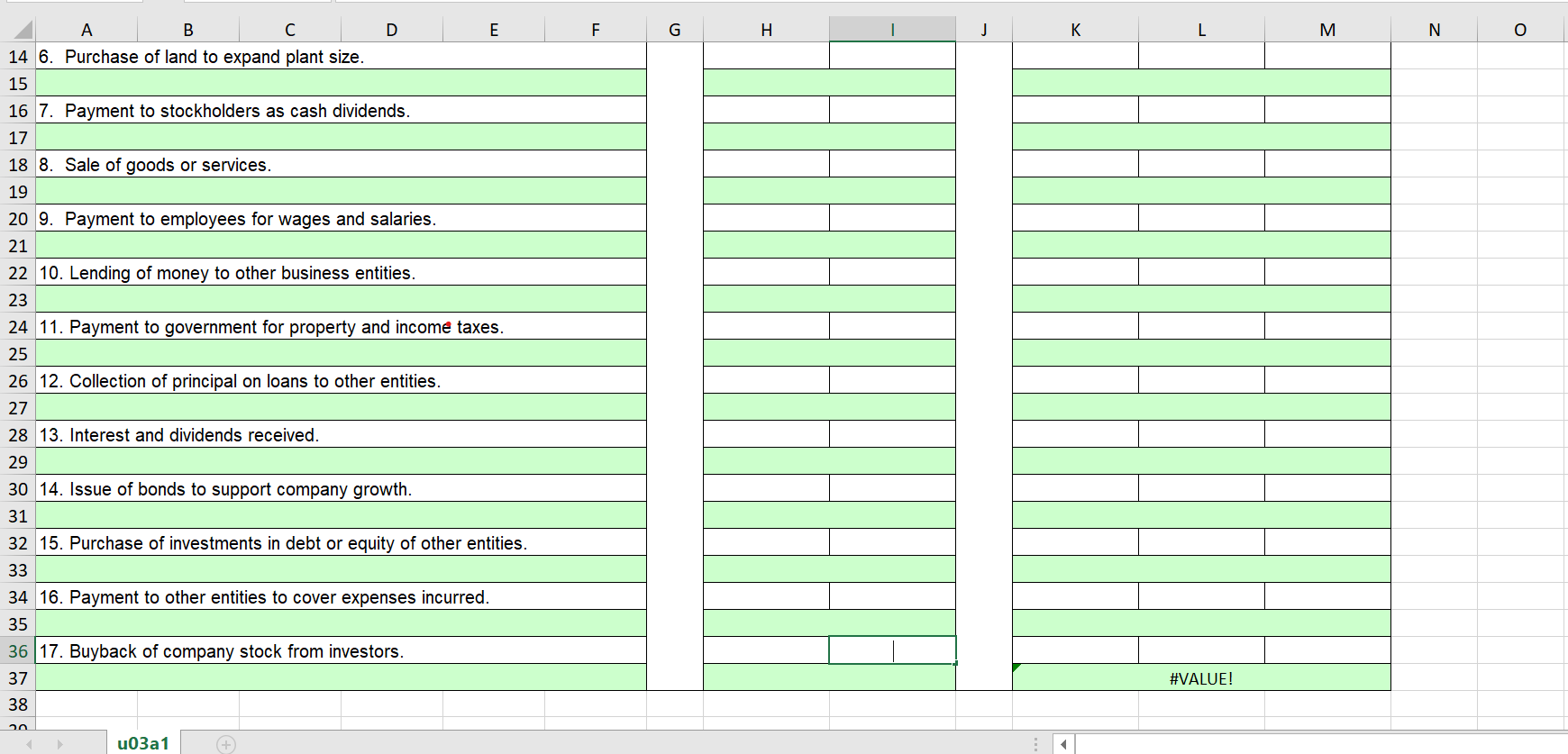

- Purchase of land to expand plant size.

- Payment to stockholders as cash dividends.

- Sale of goods or services.

- Payment to employees for wages and salaries.

- Lending of money to other business entities.

- Payment to government for property and income taxes.

- Collection of principal on loans to other entities.

- Interest and dividends received.

- Issue of bonds to support company growth.

- Purchase of investments in debt or equity of other entities.

- Payment to other entities to cover expenses incurred.

- Buyback of company stock from investors.

A l B l C | D E F 14 6. Purchase of land to expand plant size. 15 16 7. Payment to stockholders as cash dividends. 17 18 8. Sale of goods or services. 19 20 9. Payment to employees for wages and salaries. 21 22 10. Lending of money to other business entities. 23 24 11. Payment to government for property and income taxes. 25 26 12. Collection of principal on loans to other entities. 27 28 13. Interest and dividends received. 29 30 14. Issue of bonds to support company growth. 31 32 15. Purchase of investments in debt or equity of other entities. 33 34 16. Payment to other entities to cover expenses incurred. 35 36 17. Buyback of company stock from investors. 37 #VALUE! 38 u03a1 A B C D E F G H K M N Instructions: Classify each of the following cash inflows and outflows as operating, investing, or financing activities. 2 For each item in Column A, place an "X" in the appropriate inflow/outflow cell and cash flow activitiy cell. 3 Column A Inflow Outflow & Operating Investing Financing 4 1. Sale of a piece of company equipment. 5 6 2. Sale of common stock. 7 8 3. Payment to suppliers for merchandise purchased. 9 10 4. Payment to lenders for interest on note payable. 11 12 5. Sale of investments in other companies. 13 14 6. Purchase of land to expand plant size. 15 16 7. Payment to stockholders as cash dividends. 17 18 8. Sale of goods or services. 19 20 9. Payment to employees for wages and salaries. 21 22 10. Lending of money to other business entities. 23 24 11. Payment to government for property and income taxes. 403a1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts