Question: You model GDP as an AR(1) process: 9. You model GDP as an AR(1) process: In(GDPt) = a + pln(GDP+-1) + et (a) Briefly explain

You model GDP as an AR(1) process:

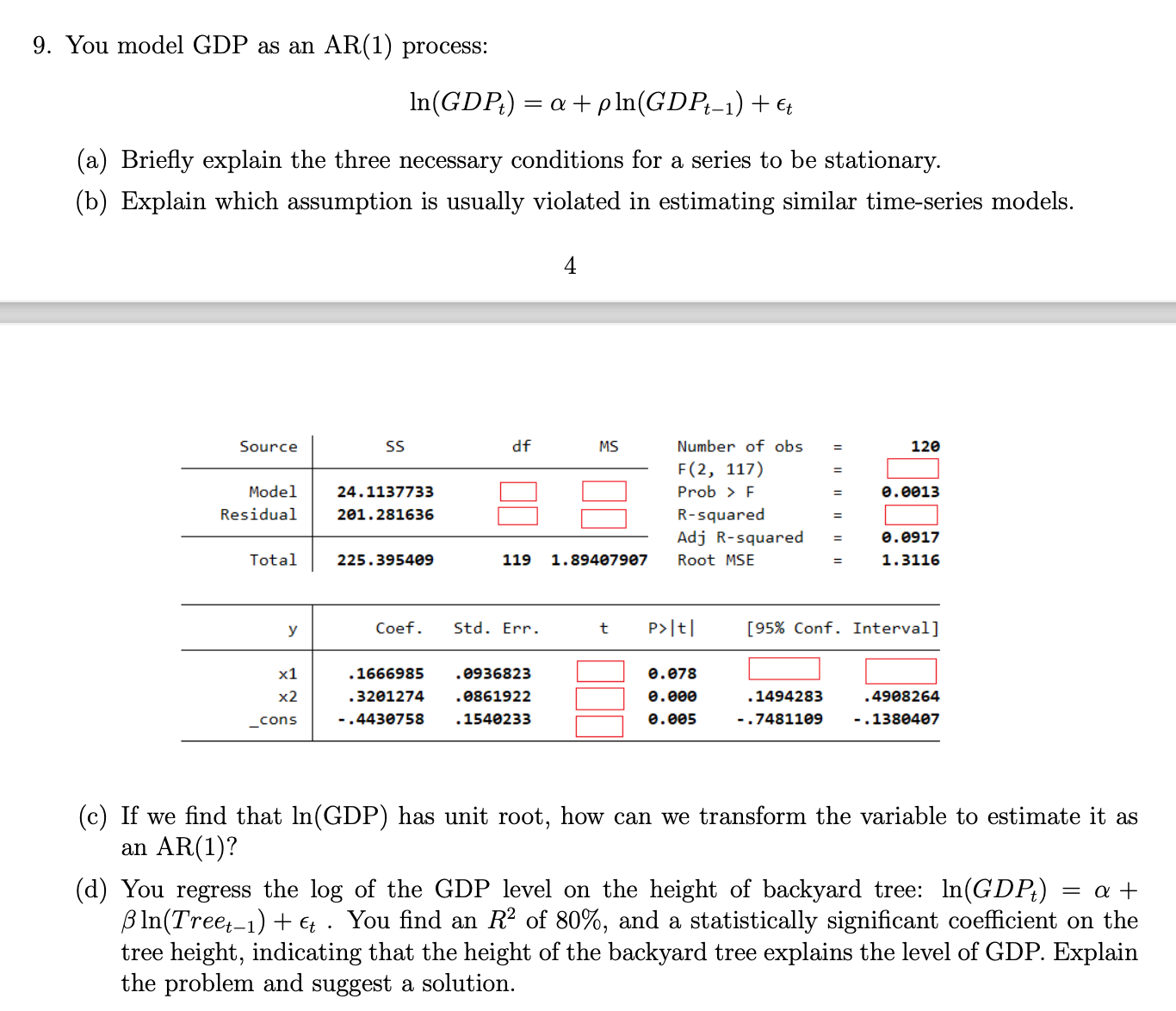

9. You model GDP as an AR(1) process: In(GDPt) = a + pln(GDP+-1) + et (a) Briefly explain the three necessary conditions for a series to be stationary. (b) Explain which assumption is usually violated in estimating similar time-series models. 4 Source SS df MS Number of obs 120 F(2, 117) Model 24. 1137733 Prob > F 11 1I II . 0013 Residual 201 . 281636 R-squared Adj R-squared 8. 0917 11 1I Total 225 . 395409 119 1. 89407907 Root MSE 1. 3116 y Coef. Std. Err. t P>It| [95% Conf. Interval] x1 . 1666985 . 0936823 0. 078 x2 . 3201274 0861922 0.000 . 1494283 . 4908264 _cons - . 4430758 . 1540233 0. 005 - . 7481109 - . 1380407 (c) If we find that In(GDP) has unit root, how can we transform the variable to estimate it as an AR(1)? (d) You regress the log of the GDP level on the height of backyard tree: In(GDPt) = a + BIn(Treet-1) + et . You find an R2 of 80%, and a statistically significant coefficient on the tree height, indicating that the height of the backyard tree explains the level of GDP. Explain the problem and suggest a solution

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts