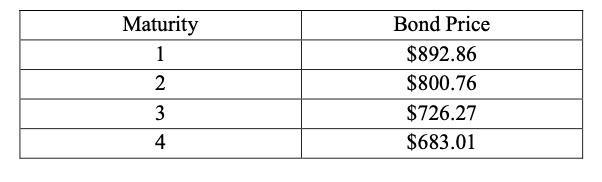

You observe the prices of the following zero-coupon bonds with a par value of $1,000. Compute the

Fantastic news! We've Found the answer you've been seeking!

Question:

You observe the prices of the following zero-coupon bonds with a par value of $1,000. Compute the one-year forward rates for

1) One year from today,

2) Two years from today, and

3) Three years from today, respectively. (Assuming annual compounding).

Expert Answer:

To compute the oneyear forward rates for each of the specified time periods 1 year 2 ye... View the full answer

Related Book For

Foundations of Financial Management

ISBN: 978-1259024979

10th Canadian edition

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen, Doug Short, Michael Perretta

Posted Date: