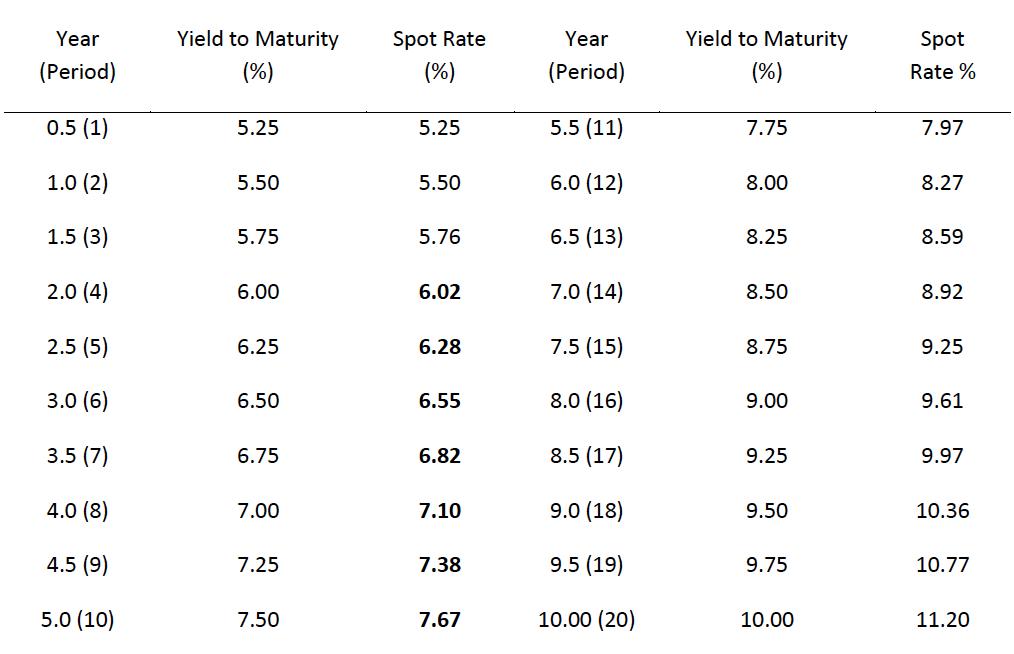

You observe the yields of the following Treasury securities at below (all yields are shown on a

Fantastic news! We've Found the answer you've been seeking!

Question:

You observe the yields of the following Treasury securities at below (all yields are shown on a bond-equivalent basis). All the securities maturing from 1.5 years on are selling at par. The 0.5 and 1.0-year securities are zero-coupon instruments.

(a) What should the price of a 6% 5.5-year Treasury security be?

(b) What is the six-month forward rate starting in the seventh year?

Expert Answer:

a To calculate the price of a 6 55year Treasury security we need to discount the semiannual coupons ... View the full answer

Related Book For

Posted Date: