Question: You recently accepted the controller position for Java the Hut, a regional coffee chain. Prepare Acquisition Journal Entry to reflect fair values of New Castle

You recently accepted the controller position for Java the Hut, a regional

coffee chain.

Prepare Acquisition Journal Entry to reflect fair values of New Castle Coffee on 1/1

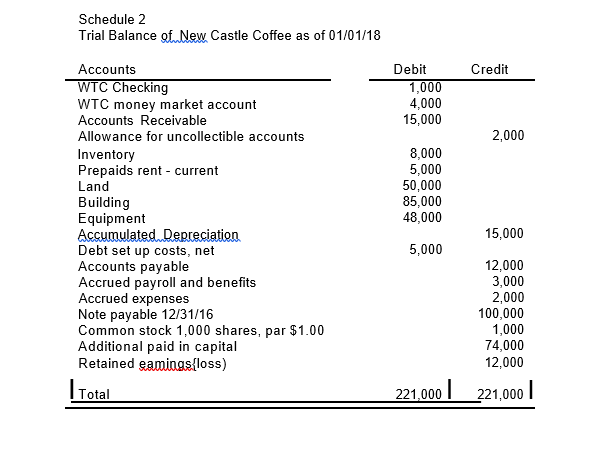

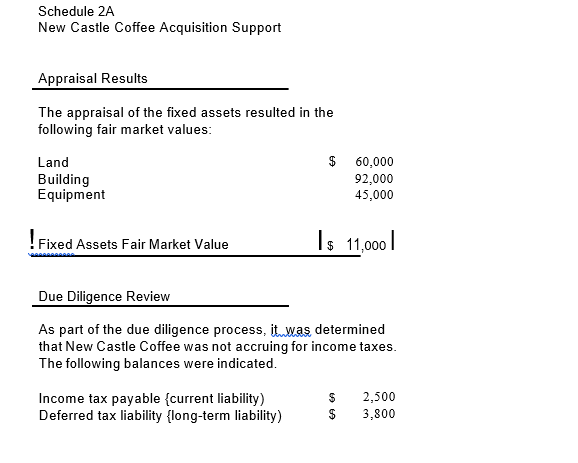

- Prepare the acquisition accounting analysis of New Castle Coffee using

the information in Schedule 2 and Schedule 2A

- Prepare the acquisition journal entry for New Castle Coffee based on your work above.

- Using the journal entry in Number 3, compare the journal entry values by

account and amount and identify all differences compared to Schedule 2.

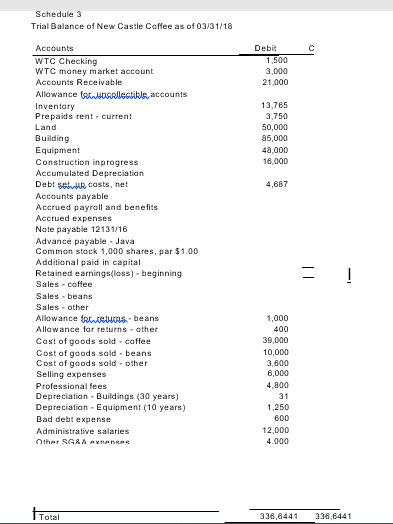

Adjust Schedule 3 for Acquisition Values

Because the project uses a situation you may encounter in practice, the reported results of New Castle Coffee on 3/31 included in Schedule 3 do not include any adjustments for the acquisition. Remember that the accounting department of New Castle Coffee would keep functioning as if the acquisition never occurred until new values are established. In practice, this is often a number of months following an acquisition to complete the appropriate accounting.

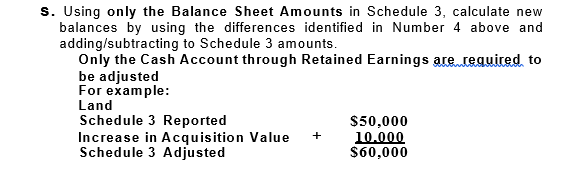

s. Using only the Balance Sheet Amounts in Schedule 3, calculate new balances by using the differences identified in Number 4 above and adding/subtracting to Schedule 3 amounts.

Only the Cash Account through Retained Earnings are required to be adjusted.

s. Using only the Balance Sheet Amounts in Schedule 3, calculate new balances by using the differences identified in Number 4 above and adding/subtracting to Schedule 3 amounts. Only the Cash Account through Retained Earnings are required to be adjusted For example: Land Schedule 3 Reported Increase in Acquisition Value Schedule 3 Adjusted + $50,000 10.000 $60,000 Schedule 2 Trial Balance of New Castle Coffee as of 01/01/18 Accounts WTC Checking WTC money market account Accounts Receivable Allowance for uncollectible accounts Inventory Prepaids rent - current Land Building Equipment Accumulated Depreciation Debt set up costs, net Accounts payable Accrued payroll and benefits Accrued expenses Note payable 12/31/16 Common stock 1,000 shares, par $1.00 Additional paid in capital Retained eamings{loss) Total Debit 1,000 4,000 15,000 8,000 5,000 50,000 85,000 48,000 5,000 221,000 Credit 2,000 15,000 12,000 3,000 2,000 100,000 1,000 74,000 12,000 221,000 Schedule 2A New Castle Coffee Acquisition Support Appraisal Results The appraisal of the fixed assets resulted in the following fair market values: Land Building Equipment ! Fixed Assets Fair Market Value 60,000 92,000 45,000 Is 11,000 Income tax payable {current liability) Deferred tax liability (long-term liability) $ Due Diligence Review As part of the due diligence process, it was determined that New Castle Coffee was not accruing for income taxes. The following balances were indicated. 69 69 $ $ 2,500 3,800 Schedule 3 Trial Balance of New Castle Coffee as of 03/31/18 Accounts WTC Checking WTC money market account Accounts Receivable Allowance collectible, accounts Inventory Prepaids rent -current Land Building Equipment Construction inprogress. Accumulated Depreciation Debt se costs, net Accounts payable Accrued payroll and benefits Accrued expenses Note payable 12131/16 Advance payable Java Common stock 1,000 shares, par $1.00 Additional paid in capital Retained earnings(loss) - beginning Sales-coffee Sales - beans Sales - other Allowance faces-beans Allowance for returns - other Cost of goods sold-coffee Cost of goods sold - beans Cost of goods sold - other Selling expenses Professional fees Depreciation - Buildings (30 years) Depreciation Equipment (10 years) Bad debt expense Administrative salaries Other SG&A AYNANAS Total Debit 1,500 3,000 21,000 13,765 3,750 50,000 85,000 48,000 16,000 4,687 1,000 400 39,000 10,000 3,600 6,000 4,800 31 1,250 600 12,000 4.000 336,6441 = ! 336,6441 s. Using only the Balance Sheet Amounts in Schedule 3, calculate new balances by using the differences identified in Number 4 above and adding/subtracting to Schedule 3 amounts. Only the Cash Account through Retained Earnings are required to be adjusted For example: Land Schedule 3 Reported Increase in Acquisition Value Schedule 3 Adjusted + $50,000 10.000 $60,000 Schedule 2 Trial Balance of New Castle Coffee as of 01/01/18 Accounts WTC Checking WTC money market account Accounts Receivable Allowance for uncollectible accounts Inventory Prepaids rent - current Land Building Equipment Accumulated Depreciation Debt set up costs, net Accounts payable Accrued payroll and benefits Accrued expenses Note payable 12/31/16 Common stock 1,000 shares, par $1.00 Additional paid in capital Retained eamings{loss) Total Debit 1,000 4,000 15,000 8,000 5,000 50,000 85,000 48,000 5,000 221,000 Credit 2,000 15,000 12,000 3,000 2,000 100,000 1,000 74,000 12,000 221,000 Schedule 2A New Castle Coffee Acquisition Support Appraisal Results The appraisal of the fixed assets resulted in the following fair market values: Land Building Equipment ! Fixed Assets Fair Market Value 60,000 92,000 45,000 Is 11,000 Income tax payable {current liability) Deferred tax liability (long-term liability) $ Due Diligence Review As part of the due diligence process, it was determined that New Castle Coffee was not accruing for income taxes. The following balances were indicated. 69 69 $ $ 2,500 3,800 Schedule 3 Trial Balance of New Castle Coffee as of 03/31/18 Accounts WTC Checking WTC money market account Accounts Receivable Allowance collectible, accounts Inventory Prepaids rent -current Land Building Equipment Construction inprogress. Accumulated Depreciation Debt se costs, net Accounts payable Accrued payroll and benefits Accrued expenses Note payable 12131/16 Advance payable Java Common stock 1,000 shares, par $1.00 Additional paid in capital Retained earnings(loss) - beginning Sales-coffee Sales - beans Sales - other Allowance faces-beans Allowance for returns - other Cost of goods sold-coffee Cost of goods sold - beans Cost of goods sold - other Selling expenses Professional fees Depreciation - Buildings (30 years) Depreciation Equipment (10 years) Bad debt expense Administrative salaries Other SG&A AYNANAS Total Debit 1,500 3,000 21,000 13,765 3,750 50,000 85,000 48,000 16,000 4,687 1,000 400 39,000 10,000 3,600 6,000 4,800 31 1,250 600 12,000 4.000 336,6441 = ! 336,6441

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts