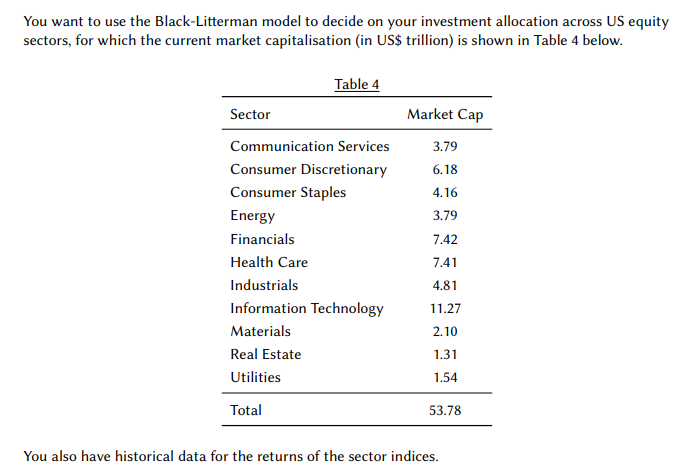

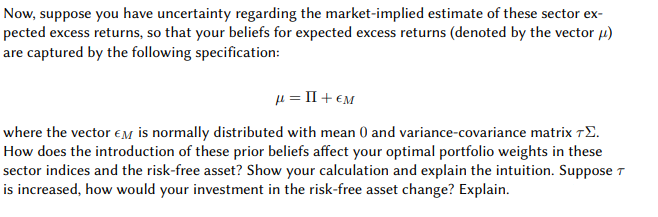

You want to use the Black-Litterman model to decide on your investment allocation across US equity...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

The BlackLitterman model combines the marketimplied expected returns captured by the market capitalization weights with the investors own views on the expected returns to determine optimal portfolio w... View the full answer

Related Book For

Posted Date: