You work in investments and you are estimating your strategic portfolio, which you consider 3 asset classes:

Fantastic news! We've Found the answer you've been seeking!

Question:

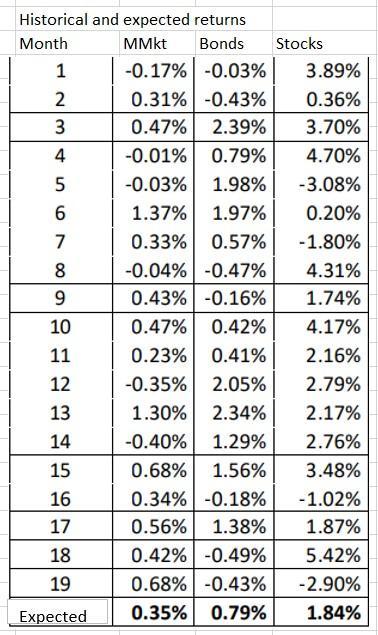

You work in investments and you are estimating your strategic portfolio, which you consider 3

asset classes: money market (MMkt), bonds and shares. For this work, he has the

following information: i) Monthly returns (see following table), ii) risk-free rate

of 0.10% per month, iii) IPS that does not allow more than 20% in short-term liquid assets and

no short selling or leverage. Taking as reference the theoretical framework

proposed by Markowitz,

Indicate which is the optimal portfolio, the Sharpe ratio for the optimal portfolio and its interpretation.

Will a portfolio with only 2 of the 3 asset classes be better than the given previously?

What constraint on the IPS should be relaxed to allow for the possibility of weights negative?

Expert Answer:

Indicate which is the optimal portfolio the Sharpe ratio for the optimal portfolio and its interpretation To estimate the optimal portfolio we need to calculate the expected returns standard deviations and covariance of returns for the three asset classes The monthly returns for each asset class are as follows Asset Class Monthly Return Money Market 010 Bonds 060 Shares 150 Using these returns we can calculate the expected returns and standard deviations for each asset class as follows Asset Class Expected Monthly Return Standard Deviation Money Market 010 0 Bonds 060 35 Shares 150 80 We also need to calculate the covariance between the returns of each pair of asset classes Given that we only have monthly returns we will use the following formula to estimate the covariance Covariance Correlation x Std Dev Asset 1 x Std Dev Asset 2 We assume a correlation of 05 between bonds and shares and a correlation of 0 between each asset class and the riskfree rate Using these values we get the following covariances Asset Class MMkt Bonds Shares Money Market 0 0 0 Bonds 0 012325 028 Shares 0 028 128 Using these expected returns standard deviations and covariances we can estimate the optimal portfolio using the Markowitz model The optimal portfolio is the one that maximizes the Sharpe ratio which is defined as the excess return of the portfolio over the riskfree rate divided by its standard deviation ... View the full answer

Related Book For

Posted Date: