Question: You would like to forecast future bond yields using time series models. The variable of interest is d_WSPCA You used SAS procedure ARIMA to find

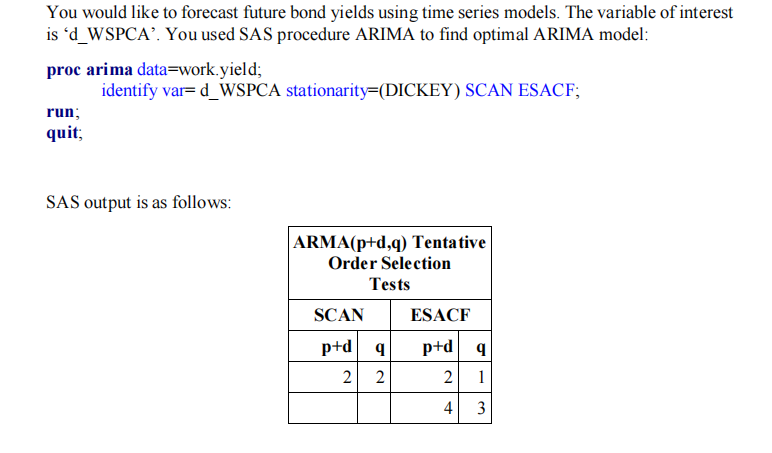

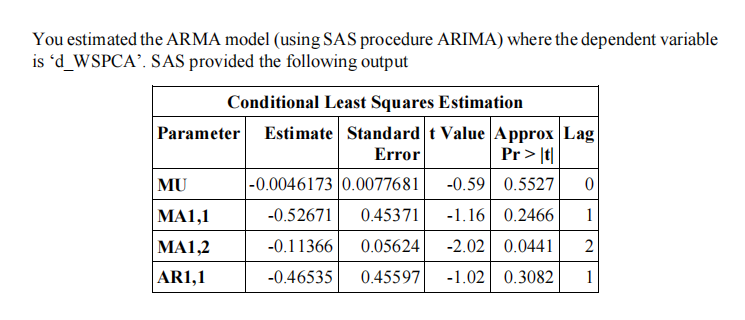

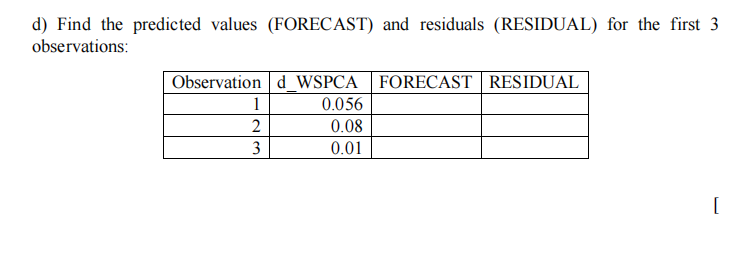

You would like to forecast future bond yields using time series models. The variable of interest is d_WSPCA You used SAS procedure ARIMA to find optimal ARIMA model: proc arima data=work. yield; identify var=d_WSPCA stationarity=(DICKEY) SCAN ESACF; run; quit; SAS output is as follows: ARMA(p+d,q) Tentative Order Selection Tests SCAN ESACF p+d 9 p+d 9 2 2 2 1 4 3 You estimated the ARMA model (using SAS procedure ARIMA) where the dependent variable is d_WSPCA'. SAS provided the following output Conditional Least Squares Estimation Parameter Estimate Standard t Value Approx Lag Error Pr>1t| MU -0.0046173 0.0077681 -0.59 0.5527 0 MA1,1 -0.52671 0.45371 - 1.16 0.2466 1 MA1,2 -0.11366 0.05624 -2.02 0.0441 2 AR1,1 -0.46535 0.45597 -1.02 0.3082 1 d) Find the predicted values (FORECAST) and residuals (RESIDUAL) for the first 3 observations: Observation d WSPCA FORECAST RESIDUAL 1 0.056 2 0.08 3 0.01 [ You would like to forecast future bond yields using time series models. The variable of interest is d_WSPCA You used SAS procedure ARIMA to find optimal ARIMA model: proc arima data=work. yield; identify var=d_WSPCA stationarity=(DICKEY) SCAN ESACF; run; quit; SAS output is as follows: ARMA(p+d,q) Tentative Order Selection Tests SCAN ESACF p+d 9 p+d 9 2 2 2 1 4 3 You estimated the ARMA model (using SAS procedure ARIMA) where the dependent variable is d_WSPCA'. SAS provided the following output Conditional Least Squares Estimation Parameter Estimate Standard t Value Approx Lag Error Pr>1t| MU -0.0046173 0.0077681 -0.59 0.5527 0 MA1,1 -0.52671 0.45371 - 1.16 0.2466 1 MA1,2 -0.11366 0.05624 -2.02 0.0441 2 AR1,1 -0.46535 0.45597 -1.02 0.3082 1 d) Find the predicted values (FORECAST) and residuals (RESIDUAL) for the first 3 observations: Observation d WSPCA FORECAST RESIDUAL 1 0.056 2 0.08 3 0.01 [

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts