Question: Your answer on question a,b,c,d. Want to compare my answer with yours REQUIRED (b) Prepare the budgeted income statement of Exelon Racket (Pty) Ltd for

Your answer on question a,b,c,d. Want to compare my answer with yours

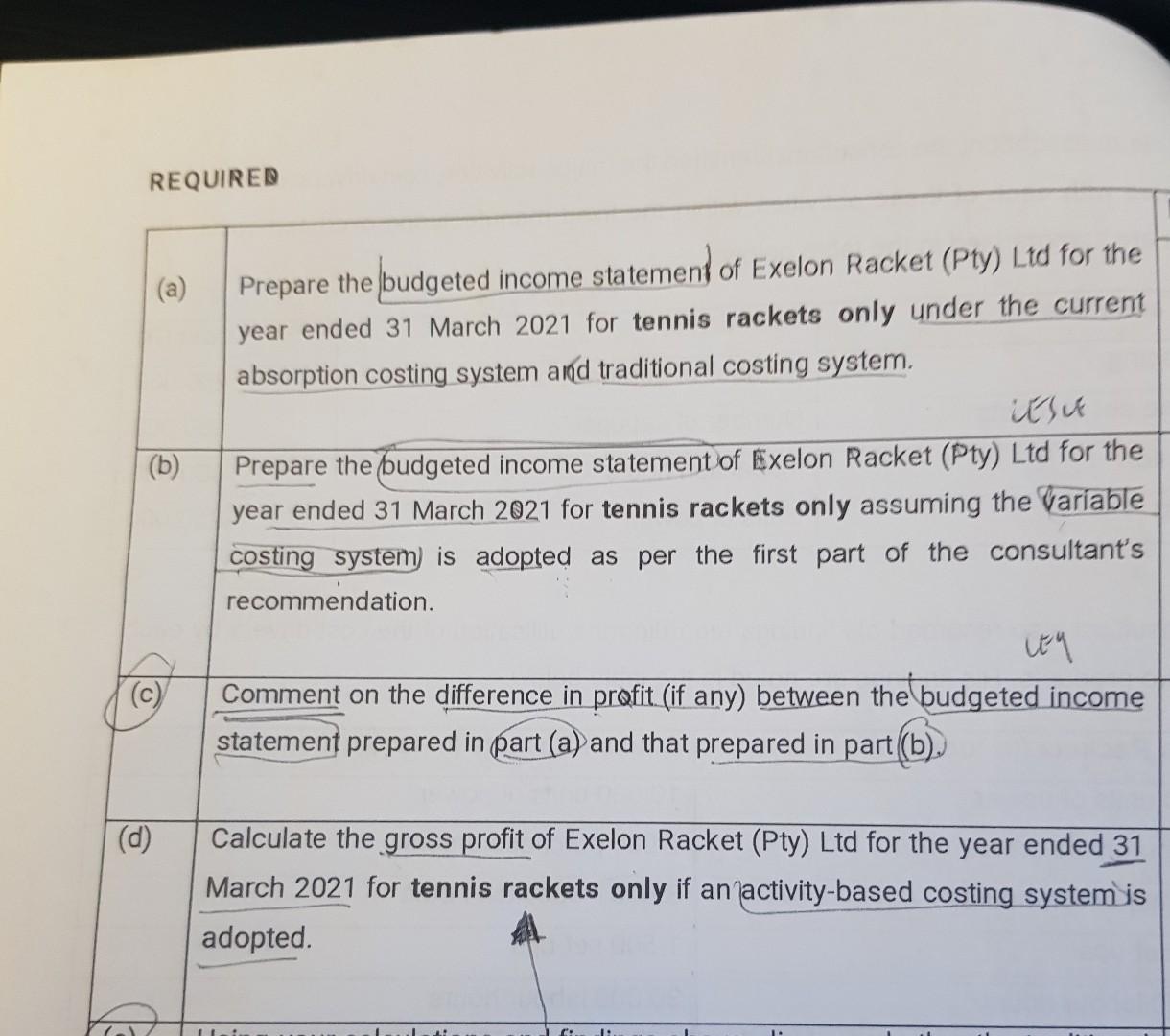

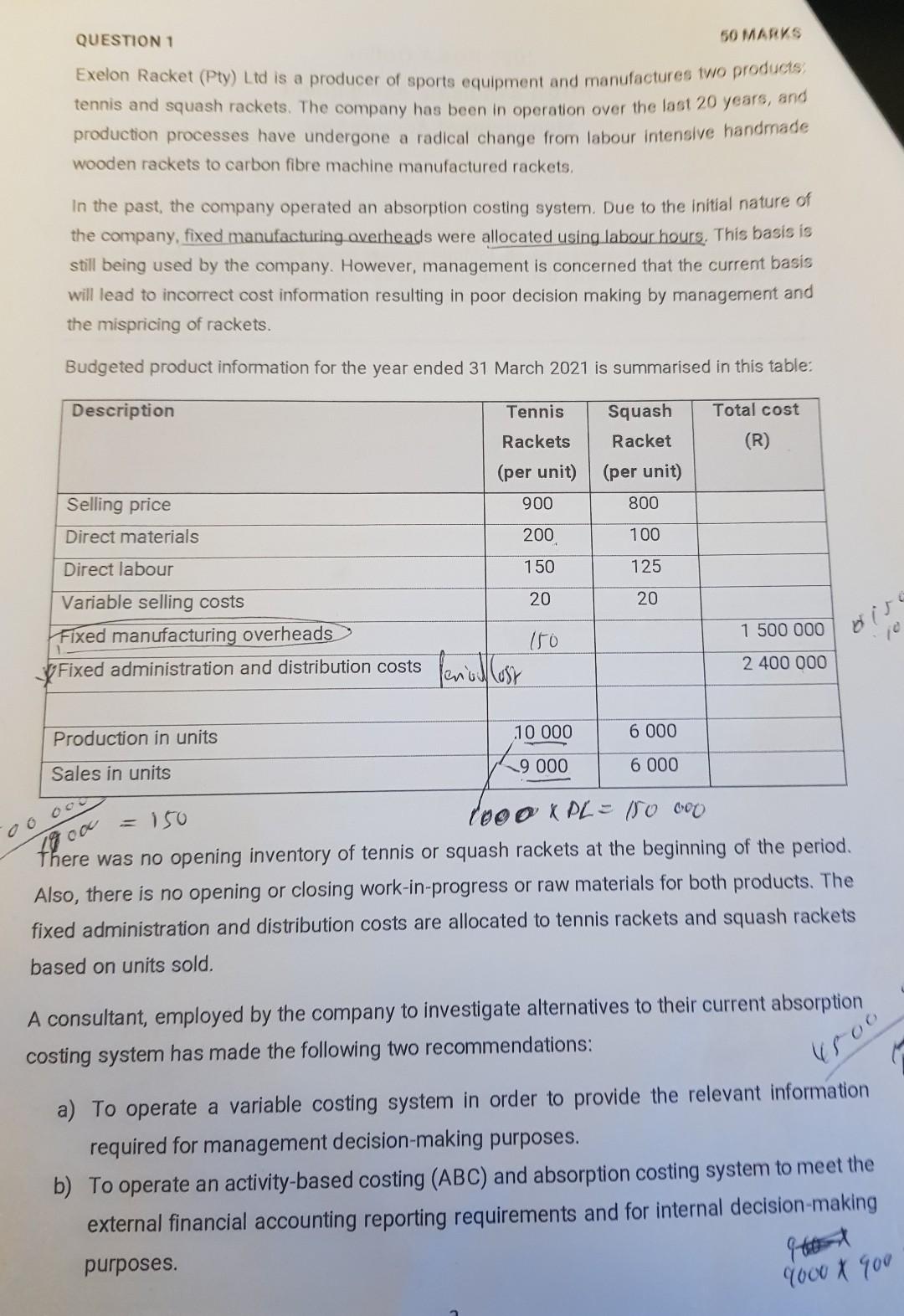

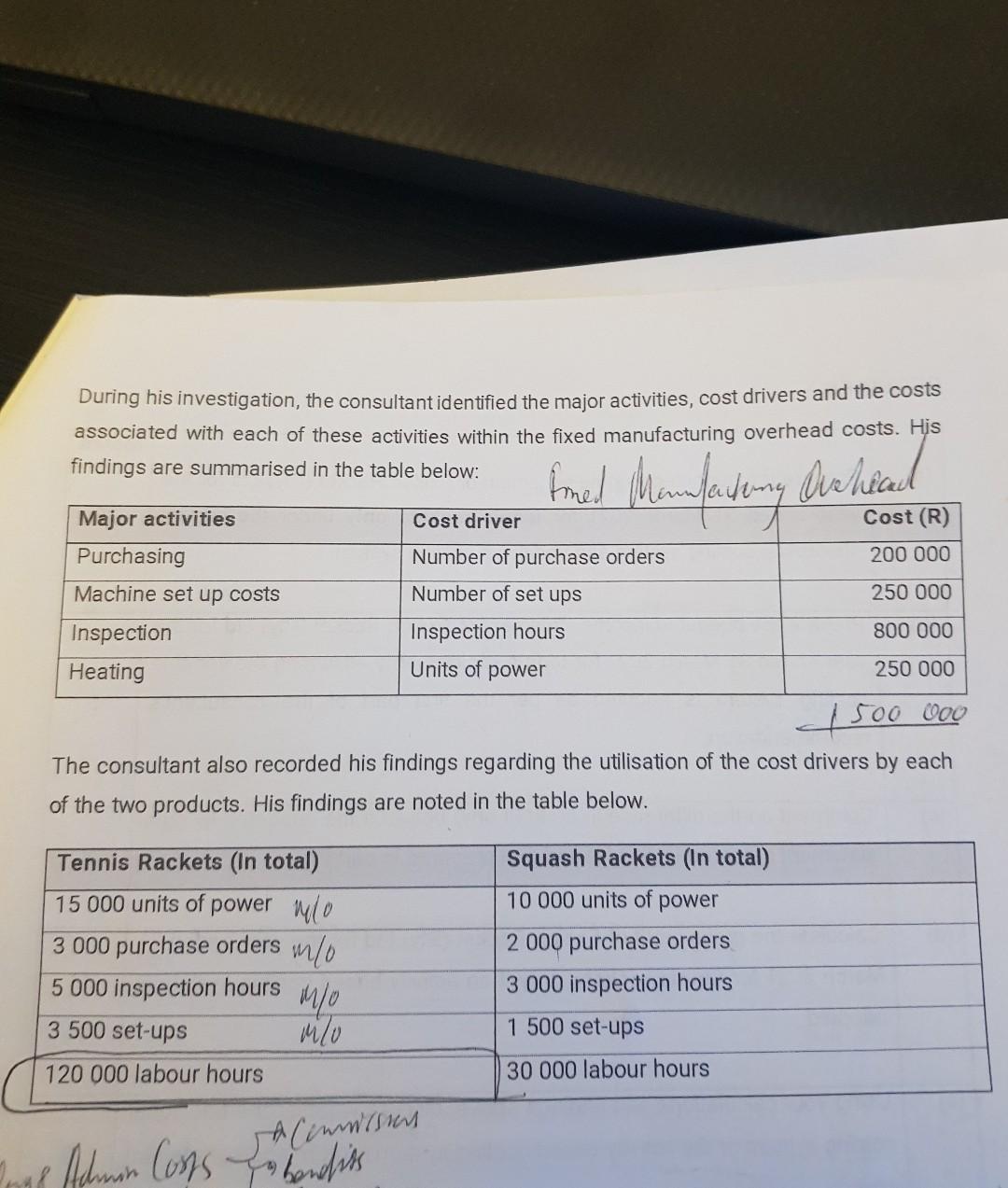

REQUIRED (b) Prepare the budgeted income statement of Exelon Racket (Pty) Ltd for the year ended 31 March 2021 for tennis rackets only under the current absorption costing system and traditional costing system. uu Prepare the budgeted income statement of Exelon Racket (Pty) Ltd for the year ended 31 March 2021 for tennis rackets only assuming the variable costing system is adopted as per the first part of the consultants recommendation. ity Comment on the difference in profit (if any) between the budgeted income statement prepared in part (a) and that prepared in part(b), (d) Calculate the gross profit of Exelon Racket (Pty) Ltd for the year ended 31 March 2021 for tennis rackets only if an'activity-based costing system is adopted. QUESTION 1 50 MARKS Exelon Racket (Pty) Ltd is a producer of sports equipment and manufactures to products tennis and squash rackets. The company has been in operation over the last 20 years, and production processes have undergone a radical change from labour intensive handmade wooden rackets to carbon fibre machine manufactured rackets, In the past, the company operated an absorption costing system. Due to the initial nature of the company, fixed manufacturing overheads were allocated using labour hours. This basis is still being used by the company. However, management is concerned that the current basis will lead to incorrect cost information resulting in poor decision making by management and the mispricing of rackets. Budgeted product information for the year ended 31 March 2021 is summarised in this table: Description Tennis Total cost Rackets Squash Racket (per unit) (R) (per unit) 900 800 Selling price Direct materials 200 100 Direct labour 150 125 20 20 Variable selling costs Fixed manufacturing overheads ( 150 yFixed administration and distribution costs fenoll Cosy 1 500 000 2 400 000 Production in units 10 000 6 000 9 000 Sales in units 6 000 foner 150 tooo KPL = 50 000 there was no opening inventory of tennis or squash rackets at the beginning of the period. Also, there is no opening or closing work-in-progress or raw materials for both products. The fixed administration and distribution costs are allocated to tennis rackets and squash rackets based on units sold, A consultant, employed by the company to investigate alternatives to their current absorption costing system has made the following two recommendations: 4500 a) To operate a variable costing system in order to provide the relevant information required for management decision-making purposes. b) To operate an activity-based costing (ABC) and absorption costing system to meet the external financial accounting reporting requirements and for internal decision-making purposes. 9000 x 900 During his investigation, the consultant identified the major activities, cost drivers and the costs associated with each of these activities within the fixed manufacturing overhead costs. His findings are summarised in the table below: fmed Manfarteng Dinhead Cost driver Cost (R) 200 000 Major activities Purchasing Machine set up costs Inspection Heating 250 000 Number of purchase orders Number of set ups Inspection hours Units of power 800 000 250 000 1 500 000 The consultant also recorded his findings regarding the utilisation of the cost drivers by each of the two products. His findings are noted in the table below. Tennis Rackets (In total) 15 000 units of power wo 3 000 purchase orders mlo 5 000 inspection hours 3 500 set-ups mo 120 000 labour hours Squash Rackets (In total) 10 000 units of power 2 000 purchase orders 3 000 inspection hours 1 500 set-ups 30 000 labour hours info Cenwissen & Schmon Cons bonofiss

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts