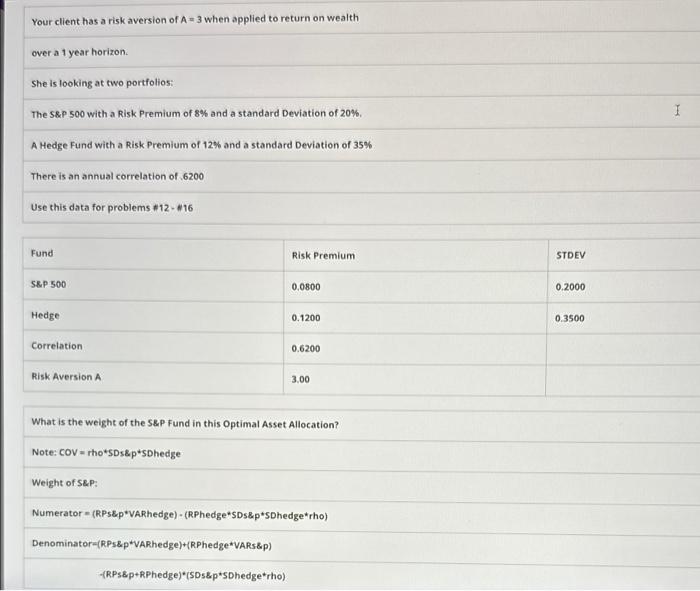

Question: Your client has a risk aversion of A=3 when applied to return on wealth over a 1 year horizon. She is looking at two portfolios:

Your client has a risk aversion of A=3 when applied to return on wealth over a 1 year horizon. She is looking at two portfolios: The S\&P 500 with a Risk Premium of 8% and a standard Deviation of 20%. A Hedge Fund with a Risk Premium of 12% and a standard Deviation of 35% There is an annual correlation of .6200 Use this data for problems $1216 \begin{tabular}{|l|l|l|l|} \hline Fund & Risk Premium & STDEV \\ \hline SE.P 500 & 0.0800 & 0.2000 \\ \hline Hedge & 0.1200 & 0.3500 \\ \hline Correlation & 0.6200 & 3.00 \\ \hline Risk Aversion A & \\ \hline \end{tabular} What is the weight of the S\&P Fund in this Optimal Asset Allocation? Note: COV= rho*SDs\&p*SDhedge Weight of S\&P: Numerator =( RPsEp*VARhedge ) - (RPhedge*SDS\&p*SDhedge* rho) Denominator=(RPs\&p+VARhedge)+(RPhedge*VARs\&p) (RPs\&p+RPhedge)*(SDs\&p*SDhedge*rho)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts