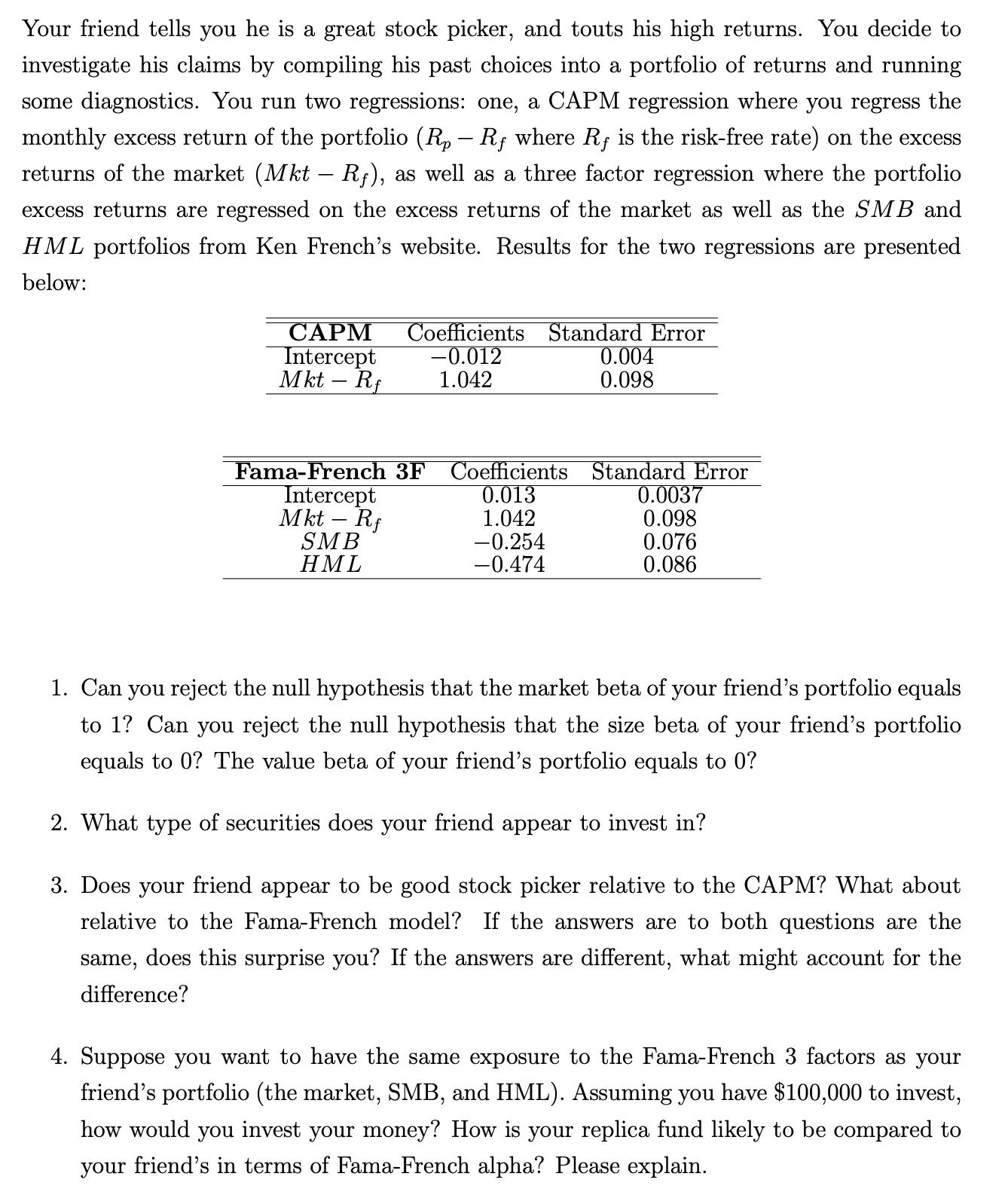

Your friend tells you he is a great stock picker, and touts his high returns. You...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

1 For the CAPM regression we cannot reject the null hypothesis that the market beta equals 1 since t... View the full answer

Related Book For

Posted Date: