Question: Your portfolio manager is using the Capital Asset Pricing Model (CAPM) for making recommendations to you. The research department of your portfolio manager has developed

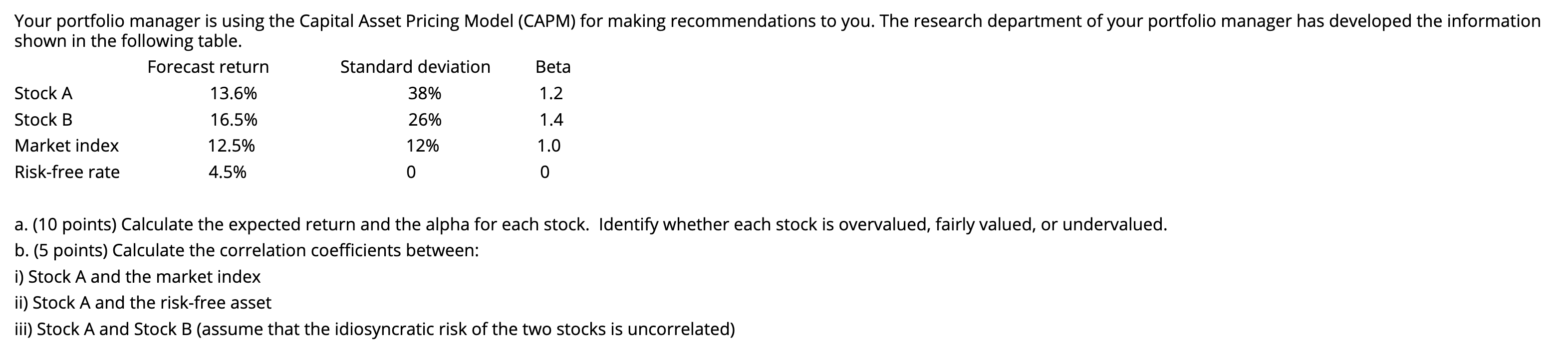

Your portfolio manager is using the Capital Asset Pricing Model (CAPM) for making recommendations to you. The research department of your portfolio manager has developed the information shown in the following table. Forecast return Standard deviation Beta Stock A 13.6% 38% 1.2 Stock B 16.5% 26% Market index 12.5% 12% 1.0 Risk-free rate 4.5% 0 0 1.4 a. (10 points) Calculate the expected return and the alpha for each stock. Identify whether each stock is overvalued, fairly valued, or undervalued. b. (5 points) Calculate the correlation coefficients between: i) Stock A and the market index ii) Stock A and the risk-free asset iii) Stock A and Stock B (assume that the idiosyncratic risk of the two stocks is uncorrelated)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts