Question: Your task is to use the information in the case to decide whether this project is worth undertaking in the bull case only. You can

Your task is to use the information in the case to decide whether this project is worth undertaking in the bull case only. You can submit all of the following in one file:

- All assumptions

- (Projected) profit and loss [as far as you can go]

- (Projected) free cash flow analysis

- Calculation of NPV and IRR

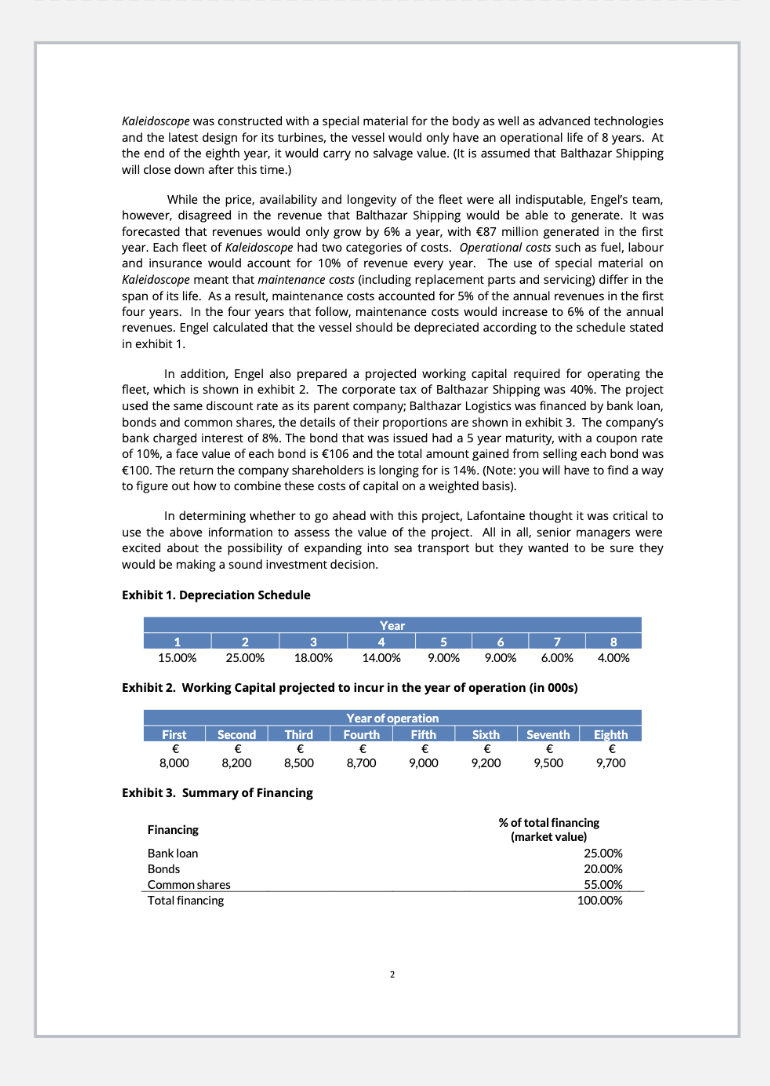

TERENCE TSE Balthazar Logistics 6th March 2021 In March 2018, Tom Lafontaine, CEO for Balthazar Logistics Inc., a trucking company, was evaluating a new proposal that would require substantial investment. This project was of particular importance as it would represent a new source of revenue - one that is badly needed. The investment involves branching out into a new business. Lafontaine, therefore, had to decide whether his company should immediately start the project. From trucking to shipping Balthazar Logistics owned a huge fleet of trucks that deliver valuable goods across the UK and Europe. Founded in 1983, the company had grown substantially. However, Balthazar Logistics has been on a decline since the 90s. Severe competition almost drove the company into bankruptcy. Various CEOs had been appointed to revive the company but without much success. But that was until Tom Lafontaine. He joined the company as the CFO in 2009, having spent his earlier career at one of the largest investment banks. In 2013, he was made the CEO and tasked with restoring the former glory of the company. Having saved the ailing Balthazar Logistics and turned it into one of the most profitable companies within the trucking industry, Lafontaine ought to have many reasons to be happy. Yet, he was not. This was because he knew that the profit margin for the trucking company would become increasingly razor thin as other non-trucking firms had been entering this market. This worried him. At a meeting with the senior management of the company in November 2017, he put forward such concerns and asked the senior executives to come up with new ways to ensure that Balthazar Logistics could remain profitable. Balthazar Shipping In the follow-up senior management meeting that took place in early 2018, Evans Engel, a newly recruited business development executive from a major shipping company, proposed that Balthazar Logistics might want to consider moving into a completely new line of business to create a new stream of revenue. Specifically, he suggested that company could expand into the sea logistics business. Engel and his team identified a certain number of sea routes that the company could realistically serve in the near future. In order to serve these sea routes, Balthazar Shipping, a newly created division within Balthazar Logistics, would need to purchase a fleet of vessels. Having done some prior research and relying on his experience, Engel identified that the vessel that could best meet the requirements of Balthazar Shipping was a fleet of ships called Kaleidoscope, the latest type of transport vessel in the industry of sea logistics. Project economics The purchase price tag attached to a fleet of Kaleidoscope was 290 million. Since the fleet was custom-made and Balthazar Shipping was a new entity, manufacturer insisted that the purchase ought to be paid in full upfront - the company would have to make this payment in 2019. Once the purchase was made, the fleet would enter service on the first day of 2020. Since each Kaleidoscope was constructed with a special material for the body as well as advanced technologies and the latest design for its turbines, the vessel would only have an operational life of 8 years. At the end of the eighth year, it would carry no salvage value. (It is assumed that Balthazar Shipping will close down after this time.) While the price, availability and longevity of the fleet were all indisputable, Engel's team, however, disagreed in the revenue that Balthazar Shipping would be able to generate. It was forecasted that revenues would only grow by by 6% a year, with 87 million generated in the first year. Each fleet of Kaleidoscope had two categories of costs. Operational costs such as fuel, labour and insurance would account for 10% of revenue every year. The use of special material on Kaleidoscope meant that maintenance costs (including replacement parts and servicing) differ in the span of its life. As a result, maintenance costs accounted for 5% of the annual revenues in the first four years. In the four years that follow, maintenance costs would increase to 6% of the annual revenues. Engel calculated that the vessel should be depreciated according to the schedule stated in exhibit 1. In addition, Engel also prepared a projected working capital required for operating the fleet, which is shown in exhibit 2. The corporate tax of Balthazar Shipping was 40%. The project used the same discount rate as its parent company, Balthazar Logistics was financed by bank loan, bonds and common shares, the details of their proportions are shown in exhibit 3. The company's bank charged interest of 8%. The bond that was issued had a 5 year maturity, with a coupon rate of 10%, a face value of each bond is 106 and the total amount gained from selling each bond was 100. The return the company shareholders is longing for is 14%. (Note: you will have to find a way to figure out how to combine these costs of capital on a weighted basis). In determining whether to go ahead with this project, Lafontaine thought it was critical to use the above information to assess the value of the project. All in all, senior managers were excited about the possibility of expanding into sea transport but they wanted to be sure they would be making a sound investment decision. Exhibit 1. Depreciation Schedule 1 15.00% 2 25.00% Year 4 14.00% 6 9.00% 8 4.00% 18.00% 9.00% 6.00% Exhibit 2. Working Capital projected to incur in the year of operation (in 000s) First Second 8,000 8,200 Third 8,500 Year of operation Fourth Fifth 8,700 9,000 Sixth 9,200 Seventh 9,500 Eighth 9,700 Exhibit 3. Summary of Financing Financing Bank loan Bonds Common shares Total financing % of total financing (market value) 25.00% 20.00% 55.00% 100.00%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts