Question: You're tasked with estimating inventory contained in a building that burned down to the ground. It was a total loss. You have the following information

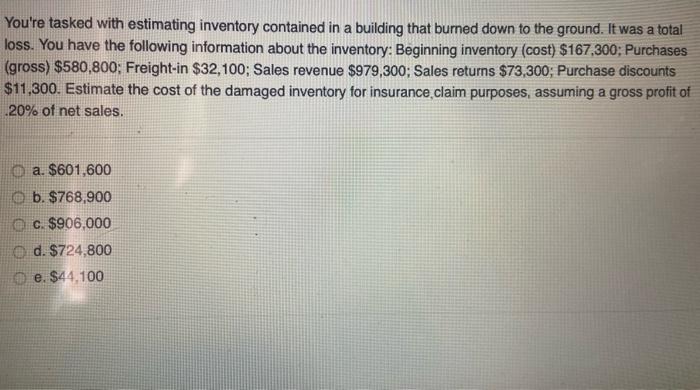

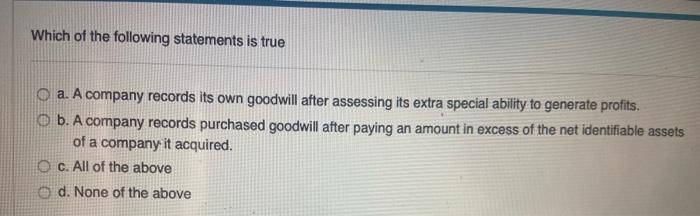

You're tasked with estimating inventory contained in a building that burned down to the ground. It was a total loss. You have the following information about the inventory: Beginning inventory (cost) $167,300; Purchases (gross) $580,800: Freight-in $32,100; Sales revenue $979,300; Sales returns $73,300; Purchase discounts $11,300. Estimate the cost of the damaged inventory for insurance claim purposes, assuming a gross profit of 20% of net sales. a. $601,600 b. $768,900 c. $906,000 d. $724,800 e. $44.100 Which of the following statements is true O a. A company records its own goodwill after assessing its extra special ability to generate profits. O b. A company records purchased goodwill after paying an amount in excess of the net identifiable assets of a company it acquired. c. All of the above d. None of the above

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts