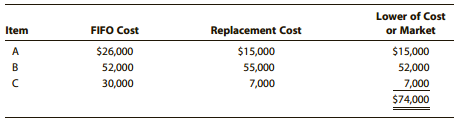

In 2017, Gail changed from the lower of cost or market FIFO method to the LIFO inventory

Question:

Item C was damaged goods, and the replacement cost used was actually the esti-mated selling price of the goods. The actual cost to replace item C was $32,000.

a. What is the correct beginning inventory for 2017 under the LIFO method?

b. What immediate tax consequences (if any) will result from the switch to LIFO?

The ending inventory is the amount of inventory that a business is required to present on its balance sheet. It can be calculated using the ending inventory formula Ending Inventory Formula =...

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a Gail must restore the beginning inventory value to actual cost to use LIFO Item FIFO Cost A 26000 ...View the full answer

Answered By

Nimlord Kingori

2023 is my 7th year in academic writing, I have grown to be that tutor who will help raise your grade and better your GPA. At a fraction of the cost on other sites, I will work on your assignment by taking it as mine. I give it all the attention it deserves and ensures you get the grade that I promise. I am well versed in business-related subjects, information technology, Nursing, history, poetry, and statistics. Some software's that I have access to are SPSS and NVIVO. I kindly encourage you to try me; I may be all that you have been seeking, thank you.

360+ Reviews

1070+ Question Solved

Related Book For

South Western Federal Taxation Individual Income Taxes 2018

ISBN: 9781337385893

41st Edition

Authors: William H. Hoffman, David M. Maloney, William A. Raabe, James C. Young, Nellen

Question Posted: