On June 1, 2018, Skylark Enterprises, a calendar year LLC reporting as a sole proprietorship, acquired a

Question:

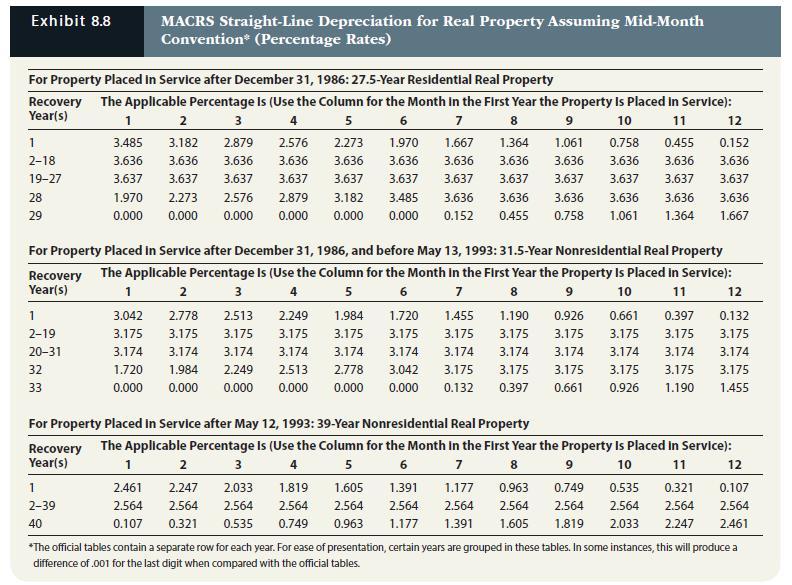

On June 1, 2018, Skylark Enterprises, a calendar year LLC reporting as a sole proprietorship, acquired a retail store building for $500,000 (with $100,000 being allocated to the land). The store building was 39-year real property, and the straight-line cost recovery method was used. The property was sold on June 21, 2022, for $385,000.

a. Compute the cost recovery and adjusted basis for the building using Exhibit 8.8 from Chapter 8.

b. What are the amount and nature of Skylark’s gain or loss from disposition of the property? What amount, if any, of the gain is unrecaptured § 1250 gain?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a b Building cost 2018 cost recovery rate 2019 cost recove...View the full answer

Answered By

Muhammad Umair

I have done job as Embedded System Engineer for just four months but after it i have decided to open my own lab and to work on projects that i can launch my own product in market. I work on different softwares like Proteus, Mikroc to program Embedded Systems. My basic work is on Embedded Systems. I have skills in Autocad, Proteus, C++, C programming and i love to share these skills to other to enhance my knowledge too.

1+ Reviews

10+ Question Solved

Related Book For

South Western Federal Taxation 2023 Comprehensive Volume

ISBN: 9780357719688

46th Edition

Authors: Annette Nellen, Andrew D. Cuccia, Mark Persellin, James C. Young

Question Posted: