Your client, Paul, owns a one-third interest as a managing (general) partner in the service-oriented PRE LLP.

Question:

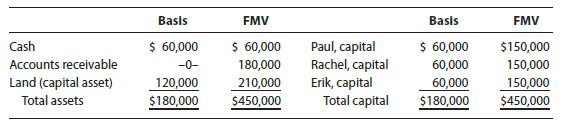

Your client, Paul, owns a one-third interest as a managing (general) partner in the service-oriented PRE LLP. He would like to retire from the limited liability partnership at the end of 2022 and asks your help in structuring the buyout transaction. He expects that his basis in the LLP interest will be about $60,000 at that time. Based on interim financial data and revenue projections, the LLP’s balance sheet is expected to approximate the following at the end of the year.

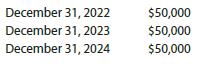

Although the LLP has some cash, the amount is not adequate to purchase Paul’s entire interest in the current year. The LLP has proposed to pay Paul, in liquidation of his interest, according to the following schedule.

Paul has agreed to this payment schedule, but the parties are not sure of the tax consequences of the buyout and have temporarily halted negotiations to consult with their tax advisers. Paul has retained you to determine the income tax ramifications of the buyout and to make sure he secures the most advantageous result available.

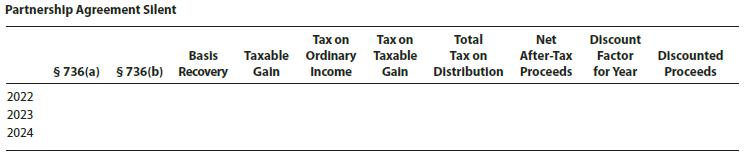

a. If the buyout agreement between Paul and PRE is silent as to the treatment of each payment, how will each payment be treated by Paul and the partnership?

b. As Paul’s adviser, what payment schedule would you recommend that Paul negotiate to minimize his current tax liability?

c. Regarding the LLP, what payment schedule would ensure that the remaining partners receive the earliest possible deductions?

d. Under the three alternatives in parts (a) to (c), what is the present value of Paul’s after-tax cash received from the buyout? Which alternative do you recommend to your client, Paul? Does this change your recommendations in parts (a) through (c)? Paul’s Federal and state tax rate for capital gains is 25%, and his marginal combined state and Federal rate for ordinary income is 40%. Paul typically earns 6% on his investments (after-tax discount rate); the first payment will be received one year from now (with the other payments one year apart). Use the present value tables in Appendix E. Each year’s after-tax cash flow differs, so discount each year’s net after-tax proceeds separately and then sum the totals.

Create a spreadsheet that summarizes the after-tax cash flows, and present values of the three alternatives. You might use the format shown at the end of this problem for part (a), where the partnership agreement is silent, and then copy and modify the format for parts (b) and (c).

e. What additional planning opportunities might be available to the partnership?

Step by Step Answer:

a Because Paul is a general partner in a serviceproviding partnership the payment must be allocated between 736a and 736b payments If the partners do not enter into a specific agreement as to the timi...View the full answer

South-Western Federal Taxation 2022 Corporations, Partnerships, Estates And Trusts

ISBN: 9780357519240

45th Edition

Authors: William A. Raabe, James C. Young, Annette Nellen, William H. Hoffman