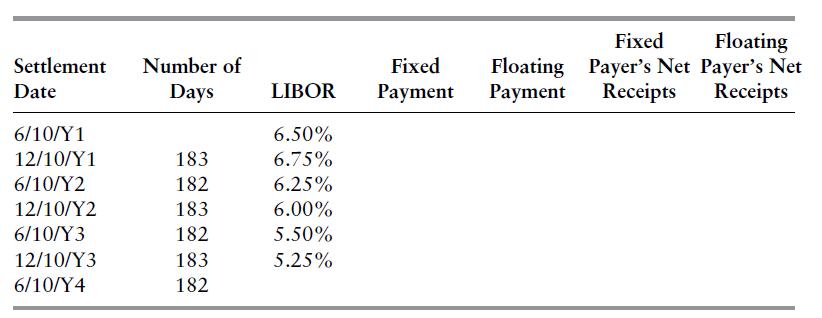

Question: The table below shows the effective dates on a 6%/LIBOR swap, the number of days between effective dates, and assumed LIBORs on effective dates. Complete

The table below shows the effective dates on a 6%/LIBOR swap, the number of days between effective dates, and assumed LIBORs on effective dates. Complete the table by determining the swap’s fixed payments, floating payments, and net receipts received by the fixed- and floating-rate payers.

Settlement Number of Fixed Floating Date Days LIBOR Payment Payment 6/10/Y1 6.50% 12/10/Y1 183 6.75% 6/10/Y2 182 6.25% 12/10/Y2 183 6.00% 6/10/Y3 182 5.50% 12/10/Y3 183 5.25% 6/10/Y4 182 Floating Fixed Payer's Net Payer's Net Receipts Receipts

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock