The Beal Manufacturing Companys costing system has two direct-cost categories: direct materials and direct manufacturing labor. Manufacturing

Question:

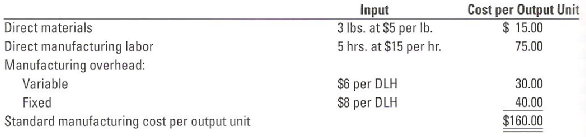

The Beal Manufacturing Company’s costing system has two direct-cost categories: direct materials and direct manufacturing labor. Manufacturing overhead (both variable and fixed) is allocated to products on the basis of standard direct manufacturing labor hours (DLH). At the beginning of 2009, Beal adopted the following standards for its manufacturing costs:

The denominator level for total manufacturing overhead per month in 2009 is 40,000 direct manufacturing labor-hours. Beal’s flexible budget for January 2009 was based on this denominator level. The records for January indicated the following:

1. Prepare a schedule of total standard manufacturing costs for the 7,800 output units in January 2009.

2. For the month of January 2009, compute the following variances, indicating whether each is favorable (F) or unfavorable (U):

a. Direct materials price variance, based on purchases

b. Direct materials efficiency variance

c. Direct manufacturing labor price variance

d. Direct manufacturing labor efficiency variance

e. Total manufacturing overhead spending variance

f. Variable manufacturing overhead efficiency variance

g. Production-volume variance

Step by Step Answer:

1 Total standard production costs are based on 7800 units of output 2 Solu...View the full answer

Cost Accounting A Managerial Emphasis

ISBN: 978-0136126638

13th Edition

Authors: Charles T. Horngren, Srikant M.Dater, George Foster, Madhav