The following are monthly percentage price changes for four market indexes. Compute the following. a. Average monthly

Question:

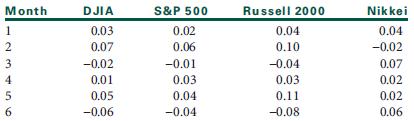

The following are monthly percentage price changes for four market indexes.

Compute the following.

a. Average monthly rate of return for each index

b. Standard deviation for each index

c. Covariance between the rates of return for the following indexes:

DJIA–S&P 500

S&P 500–Russell 2000

S&P 500–Nikkei

Russell 2000–Nikkei

d. The correlation coefficients for the same four combinations

e. Using the answers from parts (a), (b), and (d), calculate the expected return and standard deviation of a portfolio consisting of equal parts of (1) the S&P and the Russell 2000 and (2) the S&P and the Nikkei. Discuss the two portfolios.

Expected ReturnThe expected return is the profit or loss an investor anticipates on an investment that has known or anticipated rates of return (RoR). It is calculated by multiplying potential outcomes by the chances of them occurring and then totaling these... Portfolio

A portfolio is a grouping of financial assets such as stocks, bonds, commodities, currencies and cash equivalents, as well as their fund counterparts, including mutual, exchange-traded and closed funds. A portfolio can also consist of non-publicly...

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a b c d Correlation equals the covariance divided by each standard deviation Correlation D...View the full answer

Answered By

Jayshree Rathi

Hello Students!

This is Jayshree Rathi. I work on a number of renowned student-centric channels such as Chegg, coursehero, as a certified private tutor.

If you are looking for relevant and original content to complete your assignments, essays, and homework, then contact me and within the promised time, I will deliver you your personalized academic work and help you score the best.

1+ Reviews

10+ Question Solved

Related Book For

Investment Analysis and Portfolio Management

ISBN: 978-0538482387

10th Edition

Authors: Frank K. Reilly, Keith C. Brown

Question Posted: