Question: (This exercise requires appropriate computer software. The computations required can be done with RATS, EViews, Stata, TSP, LIMDEP, and a variety of other software using

(This exercise requires appropriate computer software. The computations required can be done with RATS, EViews, Stata, TSP, LIMDEP, and a variety of other software using only preprogrammed procedures.) Quarterly data on the consumer price index for 1950.1 to 2000.4 are given in Appendix Table F5.1. Use these data to fit the model proposed by Engle and Kraft (1983). The model is πt = β0 + β1πt??1 + β2πt??2 + β3πt??3 + β4πt??4 + εt where πt = 100 ln [pt/pt??1] and pt is the price index.

a. Fit the model by ordinary least squares, then use the tests suggested in the text to see if ARCH effects appear to be present.

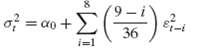

b. The authors fit an ARCH (8) model with declining weights, Fit this model. If the software does not allow constraints on the coefficients, you can still do this with a two-step least squares procedure, using the least squares residuals from the first step. What do you find?

c. Bollerslev (1986) recomputed this model as a GARCH (1, 1). Use the GARCH (1, 1) form and refit your model.

' = aut iml (9-i 36

Step by Step Solution

3.31 Rating (163 Votes )

There are 3 Steps involved in it

This exercise requires appropriate computer software The computations required can be done with RATS EViews Stata TSP LIMDEP and a variety of other software using only preprogrammed procedures Quarter... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

3-M-E-E-A (79).docx

120 KBs Word File