Question: A two-way fixed effects model, suppose that the fixed effects model is modified to include a time-specific dummy variable as well as an individual-specific variable.

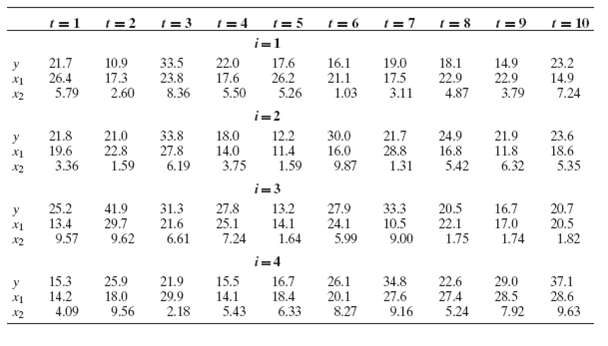

A two-way fixed effects model, suppose that the fixed effects model is modified to include a time-specific dummy variable as well as an individual-specific variable. Then yit = αi + γt + β'xit + εit. At every observation, the individual- and timespecific dummy variables sum to 1, so there are some redundant coefficients. The discussion in Section 13.3.3 shows that one way to remove the redundancy is to include an overall constant and drop one of the time specific and one of the timedummy variables. The model is, thus, yit = μ + (αi ?? α1) + (γt ?? γ1) + β'xit + εit. (Note that the respective time- or individual-specific variable is zero when t or i equals one.) Ordinary least squares estimates of β are then obtained by regression of yit ?? yi ??yt + y on xit ?? xi.??xt + x. Then (αi ?? α1) and (γt ?? γ1) are estimated using the expressions in (13-17) while m = y ?? b' x. Using the following data, estimate the full set of coefficients for the least squares dummy variable model:

Test the hypotheses that (1) the ??period?? effects are all zero, (2) the ??group?? effects are all zero, and (3) both period and group effects are zero. Use an F test in each case.

y 344 y X1 X2 y X1 X2 y X1 x2 t=1 1=2 21.7 10.9 17.3 26.4 5.79 2.60 21.8 19.6 3.36 25.2 13.4 9.57 15.3 14.2 4.09 21.0 33.8 22.8 27.8 1.59 1=3 1=4 1=5 i=1 33.5 22.0 17.6 23.8 17.6 26.2 8.36 5.50 5.26 25.9 18.0 9.56 41.9 31.3 27.8 29.7 21.6 25.1 9.62 6.61 6.19 3.75 18.0 14.0 21.9 29.9 2.18 7.24 15.5 14.1 5.43 i=2 12.2 11.4 1.59 13.2 14.1 1.64 i=4 16.7 18,4 6.33 t=6 (=7 16.1 19.0 18.1 21.1 17.5 22.9 1.03 30.0 16.0 9.87 27.9 24.1 5.99 26.1 20.1 8.27 3.11 21.7 28.8 1.31 33.3 10.5 9.00 34.8 27.6 1=8 9.16 4.87 24.9 16.8 5.42 20.5 22.1 1.75 22.6 27.4 5.24 1=9 14.9 22.9 3.79 21.9 11.8 6.32 16.7 17.0 1.74 29.0 28.5 7.92 r = 10 23.2 14.9 7.24 23.6 18.6 5.35 20.7 20.5 1.82 37.1 28.6. 9.63

Step by Step Solution

3.40 Rating (159 Votes )

There are 3 Steps involved in it

A two way fixed effects model Suppose the fixed effects model is modified to include a time specific dummy variable as well as an individual specific ... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

3-M-E-E-A (92).docx

120 KBs Word File