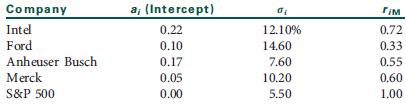

Question: Based on five years of monthly data, you derive the following information for the companies listed: a. Compute the beta coefficient for each stock. b.

Based on five years of monthly data, you derive the following information for the companies listed:

a. Compute the beta coefficient for each stock.

b. Assuming a risk-free rate of 8 percent and an expected return for the market portfolio of 15 percent, compute the expected (required) return for all the stocks and plot them on the SML.

c. Plot the following estimated returns for the next year on the SML and indicate which stocks are undervalued or overvalued.

• Intel—20 percent

• Ford—15 percent

• Anheuser Busch—19 percent

• Merck—10 percent

Company uicl Ford Anheuser Busch Merck S&P 500 a, (Intercept) 0.22 0.10 0.17 0.05 0.00 12.10% 14.60 7.60 10.20 5.50 riM 0.72 0.33 0.55 0.60 1.00

Step by Step Solution

3.36 Rating (171 Votes )

There are 3 Steps involved in it

a b ER i RFR B i R M RFR 08 B i 15 08 08 07B i Stock Beta ER i 08 07B i Inte... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

370-B-A-I (4397).docx

120 KBs Word File