New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing

Auditing The Art and Science of Assurance Engagements 12th Canadian edition Alvin A. Arens, Randal J. Elder, Mark S. Beasley, Ingrid B. Splettstoesser - Solutions

How does engagement risk (auditor business risk) affect the audit process?

Explain why inherent risk is estimated for segments rather than for the overall audit. What is the effect on the amount of evidence the auditor must accumulate when inherent risk is increased from medium to high for a segment?

State the categories of circumstances that affect audit risk, and list the factors that the auditor can use to indicate the degree to which each category exists.

Distinguish between attention-directing analytical procedures and those intended to reduce detailed substantive procedures.

Gail Gordon, PA, has found ratio and trend analysis relatively useless as a tool in conducting audits. For several engagements, she computed the industry ratios included in publications by The Financial Post Company and compared them with client ratios. For most engagements, the client’s business

It is imperative that the auditor follow up on all material differences discovered through analytical procedures. What factors affect such investigations?

Explain the purpose of common-size financial statements.

The following are eight situations, each containing two means of accumulating evidence:1. Confirm accounts receivable with business organizations versus confirming receivables with consumers.2. Physically examine 8-cm steel plates versus examining electronic parts.3. Examine duplicate sales

In auditing the financial statements of a manufacturing company, the PA has found that the traditional audit trail has been replaced by an electronic one. As a result, the PA may place increased emphasis on automated internal controls and on analytical procedures of the data under audit. These

Tour province administers to students in public schools and high schools standardized tests of reading, writing, and mathematics. Reports are produced both by school and for the province overall describing how students fared in these tests. Recently, the Annual Report of the Office of the

Stores is a large department store chain with catalogue operations. The company has recently expanded from 6 to 43 stores by borrowing from several large financial institutions and from a public offering of common stock. A recent investigation has disclosed that Grande materially overstated net

Jim has two bank accounts, one for payroll and one for processing other transactions at CondoCleaners.com. He will have sales transactions (credit card deposits from the credit card service provider), payroll transactions for his employees, and expense cheques from himself, costs for suppliers and

Identify the three factors that determine the persuasiveness of evidence. How are these three factors related to audit procedures, sample size, items to select, and timing?

Identify the characteristics that determine the appropriateness of evidence. For each characteristic, provide one example of a type of evidence that is likely to be appropriate.

What are the four characteristics of the definition of a confirmation? Distinguish between a confirmation and external documentation.

What is the relationship between the control environment and control systems?

Describe the five principles that should be addressed in an effective fraud risk management process.

What is the purpose of an information systems steering committee? How does such a committee support effective corporate governance?

What is IT dependence and how can it be prevented?

List three categories of general controls. For each category, provide an example of an effective control.

You are auditing a manufacturing company with three different locations. For each phase of the financial statement audit, provide an example of the impact of automation on the audit process.

Why does the auditor need to assess controls over information systems acquisition, development, and maintenance?

Distinguish between obtaining an understanding of internal control and assessing control risk. Also, explain the methodology the auditor uses for each.

Define what is meant by a “control” and a “weakness in internal control.” Give two examples of each in the sales and collection cycle.

Describe the seven steps in assessing control risk during a financial statement audit.

Distinguish between the objectives of an internal control questionnaire and the objectives of a flowchart for documenting information about a client’s internal control. State the advantages and disadvantages of each of these two methods.

Describe what is meant by “key control” and “control deficiency.”

Explain what is meant by "significant deficiencies" as they relate to internal control. What should the auditor do when he or she has discovered significant deficiencies in internal control?

Explain what is meant by "tests of controls." Write one inspection of documents test of control and one reperformance test of control for the following internal control: hours of time cards are re-added by an independent payroll clerk and initialled to indicate performance.

Distinguish between a substantive approach and a combined approach in auditing a financial statement assertion.

Compare management’s concerns about internal control with those of the auditor.

What control processes should a small business have for IT operations and support?

During audit planning, an auditor obtained the following information:1. Management has a strong interest in employing inappropriate means to minimize reported earnings for tax- motivated reasons.2. Assets and revenues are based on significant estimates that involve subjective judgments and

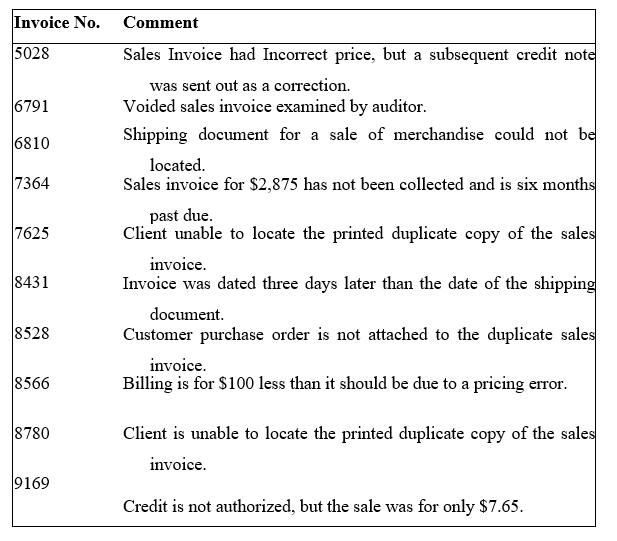

The following are errors or fraud and other irregu. 1. The incorrect price was used on sales invoices for billing larities that have occurred in Fresh Foods Grocery Store Ltd., shipments to customers because the incorrect price was a wholesale and retail grocery company. Entered into a computer

Froggledore Realty Limited is a brokerage firm that employs 35 real estate agents. The agents are given an office and basic telephone service (estimated at a $250 value per month) and are paid on a commission basis. The building has wireless computing so that agents can bring in their own

Recently, you had lunch with some friends at a new restaurant in your neighbourhood. After ordering, the server entered his password into a computer and punched in your order. The server continued taking orders and you noticed the cook removing a small printout and placing it on the wall in front

Hans & Co. LLP, is auditing CCC Inc.'s 2011 financial statements. The firm previously audited the company’s 2009 and 2010 financial statements. The 2009 audit resulted in a qualified opinion because the auditors were unable to verify the opening inventory for that year, but the 2010 audit

Metro Plastics Limited is a medium-sized manufacturer of rigid plastics. It produces casings for printers, telephones, computer screens, and other types of equipment. It also produces stand-alone plastics, such as baskets and jars. Recently, Metro Plastics was purchased by a large food

Gaboria Frank is the owner of Frankincents Machining Limited, a custom machining centre with 10 full-time employees and a part-time bookkeeper, Norma, who comes in two days a week. Norma convinced Gaboria to purchase a small business suite of accounting packages and a desktop computer with a laser

Friggle Corp. is a leasing and property management company located in Alberta. It provides financing to organizations wishing to purchase equipment or property and manages apartments and condominium properties. The company decided that it was time to upgrade its local area network. It decided also

This problem requires the use of ACL software, use “Metaphor_APTrans_2002 file in ACL_Demo.” The suggested command or other source of information needed to solve the problem requirement is included at the end of each question.REQUIREDa. For each of the computer-assisted audit procedures listed

Frequently, management is more concerned about internal controls that promote operational efficiency than about those that result in reliable financial

Jim’s business is booming, and within six months, he has gone from his first cluster of four condominiums to 30 condominium towers within the downtown core that are serviced by his cleaning staff. Jim hired his first supervisor, Vagney, this month and has spent the past week training her and

For each of the seven types of evidence discussed in Chapter 8, identify whether the evidence is applicable to procedures for risk assessment, obtaining an understanding of internal control, tests of controls, analytical procedures, or tests of details of balances.

The following are three decision factors related to the assessed level of control risk: effectiveness of internal controls, cost-effectiveness of a reduced assessed level of control risk, and results of tests of controls. Identify the combination of conditions for these three factors that is

Alphatori Company’s shares have been purchased by a food conglomerate, a public company. How will this change in ownership affect the accounting framework in use by Alphatori? How will the change in accounting framework affect the audit of Alphatori?

The following are 11 audit procedures taken from an audit program:1. Add the supplier balances in the accounts payable master file, and compare the total with the general ledger.2. Examine vendors’ invoices to verify the ending balance in accounts payable.3. Compare the balance in employee

Jennifer Schaefer, a public accountant, follows the philosophy of performing interim tests of controls on every December 31 audit as a means of keeping overtime to a minimum. Typically, the interim tests are performed sometime between August and November. REQUIRED a. Evaluate her decision to

Review the phases of the financial statement audit. List each phase that involves risk assessment. State which types of audit procedures would be used during each phase that you listed.

The following are three situations, all involving private companies, in which the auditor is required to develop an audit strategy: 1. The client has inventory at approximately 50 locations in a three-province region. The inventory is difficult to count and can be observed only by travelling by

Sidhu, a PA, is planning his first audit of Microservices Ltd., a local retailer of computers and related products. Microservices is a new company, and this is the client’s first fiscal year of operations. The owner has explained to Sidhu that she wants an audit from the beginning of the fiscal

Brewer, a public accountant, had been the partner in charge of the audit of Merkle Manufacturing Company, a nonpublic company, for 13 years. Merkle had had remarkable growth and profits in the past decade, primarily as a result of the excellent leadership provided by Bill Merkle and other competent

As explained in this chapter and in previous chapters, revenue recognition is likely to have the potential for material misstatement at most audits. Recall that orders for cleaning are placed two or more days ahead of time and paid for by credit card at the time of booking. Jim records sales in his

Explain what is meant by “recalculation” and “reperformance.” Give an example of each type of audit evidence. Why are recalculation and reperformance often dual-purpose tests?

An auditor may perform tests of controls and substantive procedures simultaneously as a matter of audit convenience. However, the substantive procedures and sample size are, in part, dependent upon the results of the tests of controls. How can the auditor resolve this apparent inconsistency?

Explain how the calculation of the gross margin percentage and the ratio of accounts receivable to sales, and their comparison to that of previous years, are related to the confirmation of accounts receivable and other tests of the accuracy of accounts receivable.

Distinguish between a combined audit approach and a substantive audit approach. Give one example of when each might be appropriate for the acquisition and payment cycle.

Assume that the client’s internal controls over the recording and classifying of capital asset additions are considered weak because the individual responsible for recording new acquisitions has inadequate technical training and limited experience in accounting. How would this situation affect

What major difference between tests of controls and tests of details of balances makes attribute sampling inappropriate for tests of details of balances?

Outline a situation for which discovery sampling would be used.

Distinguish between random selection and statistical measurement. State the circumstances under which one can be used without the other.

Describe what is meant by a “sampling unit.” Explain why the sampling unit for verifying the existence of recorded sales differs from the sampling unit for testing for the possibility of omitted sales.

Explain the difference between an attribute and an exception condition. State the exception condition for the following audit procedure: the duplicate sales invoice has been initialled, indicating the performance of internal verification.

Identify the factors an auditor uses to decide the appropriate ARACR. Compare the sample size for an ARACR of 10 percent with that of 5 percent, all other factors being equal.

State the relationship between each of the following:a. ARACR and sample size.b. Population size and sample size.c. TER and sample size.d. EPER and sample size.

Explain what is meant by “analysis of exceptions,” and discuss its importance.

Lam, a PA, is auditing the financial statements of his client, Harvesters Ltd., a company that sells and distributes agricultural equipment across Canada. Lam has performed a preliminary evaluation of the company’s internal control over sales transactions, and has concluded that the quality of

For the examination of the financial statements of Scotia Inc., Rosa Schellenberg, a public accountant, has decided to apply non statistical audit sampling in the tests of sales transactions. Based on her knowledge of Scotia’s operations in the area of sales, she decides that the estimated

You have been asked to do planning for statistical testing in the control testing of the audit of cash receipts. Following is a partial audit program for the audit of cash receipts:1. Review the cash receipts journal for large and unusual transactions.2. Trace entries from the prelisting of cash

An audit partner is developing an office training program to familiarize her professional staff with statistical decision models applicable to the audit of dollar-value balances. She wants to demonstrate the relationship of sample sizes to population size and variability and the auditor’s

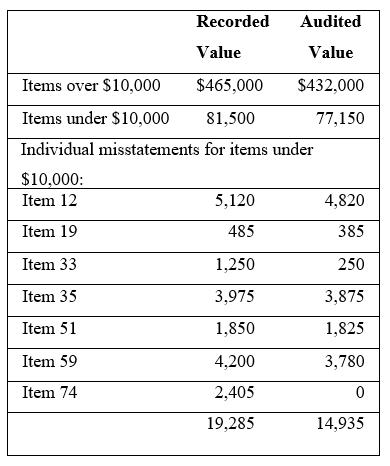

PA has just completed the accounts receivable confirmation process in the audit of Danforth Paper Company Ltd., a paper supplier to retail shops and commercial users.Following are the data related to this process:Accounts receivable recorded balance

There are about 350 payroll transactions and about 1,500 sales transactions in the current year under audit at CondoCleaners.com. The only material asset account is com? Justify your response, fixed assets. REQUIRED What type of sampling might be suitable at Condo-Cleaners.

Distinguish between a sampling error and a non sampling error. How can each be reduced?

Explain the difference between replacement sampling and non replacement sampling. Which method do auditors usually follow? Why?

What are the two types of simple random sample selection methods? Which of the two methods is used most often by auditors, and why?

List the transaction-related audit objectives for the verification of cash receipts. For each objective, state one internal control that the client can use to reduce the likelihood of misstatements.

Deirdre Brandt, a public accountant, tested sales transactions for the month of March in an audit of the financial statements for the year ended December 31, 2012. Based on the excellent results of the tests of controls, she decided to significantly reduce her substantive tests of details of

Describe the risks of error and fraud in the sales and collection cycle. Relate each risk of error or fraud to a relevant audit assertion.

ABC is a small manufacturing company that sells all of its products on credit; payment is normally due within 30 days. What are the risks associated with credit sales? What controls can ABC implement to mitigate these risks?

Items 1 through 8 are selected questions of the type generally found in internal control questionnaires used by auditors to obtain an understanding of internal control in the sales and collection cycle. In using the questionnaire for a particular client, a “yes" response to a question indicates a

Jintian Clothing Ltd. manufactures sportswear and sells it to large department stores in Western Canada. The company records sales in a sales journal. When a customer orders merchandise, a sales clerk prepares a sales invoice. The credit manager must approve all sales to new customers, and a record

You were asked in February 2013 by the board of management of your church to review its accounting procedures. As part of this review, you have prepared the following comments relating to the collections made at weekly services and record-keeping for members’ pledges and contributions:1. The

The following is a partial audit program for the audit of cash receipts:1. Review the cash receipts journal for large and unusual transactions.2. Trace entries from the prelisting of cash receipts to the cash receipts journal to determine if each is recorded.3. Compare customer name, date, and

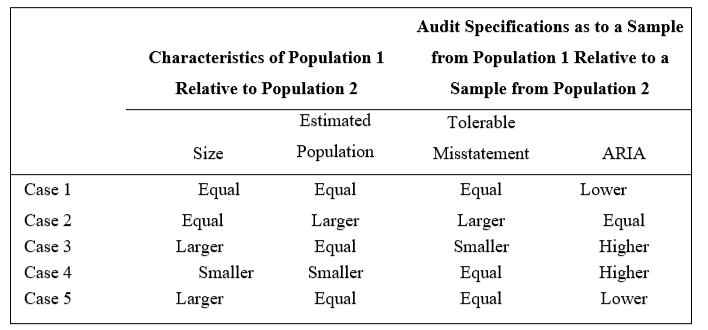

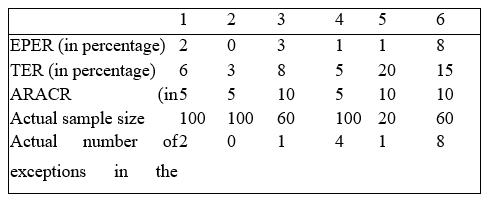

The following are auditor judgments and audit sampling results for six populations. Assume large populationREQUIREDa. For each population, did the auditor select a smaller sample size than is indicated by using attribute sampling tables for determining sample size? Evaluate, selecting either a

In performing tests of controls and substantive tests of transactions for the Oakland Hardware Company, Ben Frentz, a public accountant, is concerned with the internal verification of pricing, extensions, and footings of sales invoices, and the accuracy of the calculations. In testing sales using

Pharmaceutical Company, a drug manufacturer, has the following internal controls for billing and recording accounts receivable:1. An incoming customer’s purchase order is received in the order department by a clerk who enters the information into the sales management system. The system assigns

This problem requires the use of ACL software, use the Metaphor_AR_2002 file in ACL_Demo (in the Tables folder). The suggested command or other source of information needed to solve the problem requirement is included at the end of each question. a. Determine the total number and amount of

Many of the condominium towers that comprise CondoCleaners.com’s customer base have stores or businesses located in or near the towers. Jim has decided to further expand his business by offering cleaning services to businesses. Unlike residential customers, commercial accounts generate accounts

Distinguish between bad-debt expense and write off of uncollectable accounts. Explain why they are audited in completely different ways.

List the transaction-related audit objectives for the verification of sales transactions. For each objective, state one internal control that the client can use to reduce the likelihood of misstatements.

What three types of authorizations are commonly used as internal controls for sales? For each authorization, state a test of controls that the auditor could use to verify whether the control was effective in preventing misstatements.

Distinguish between tests of details of balances and tests of controls for the sales and collection cycle. Explain how the tests of controls affect the tests of details.

Define what is meant by “alternative procedures,” and explain their purpose. Which alternative procedures are the most reliable? Why?

Ewing his interim audit visit, Charles Ai determined that one of the subsidiary companies of Mega Big Limited had experienced some very serious problems with respect to the credit management and collection of trade accounts receivable. During the first six months of the year, the accounts

Explain the relationship of each of the following to the sales and collection cycle: flowcharts, assessing control risk, tests of controls, and tests of details of balances.

Charles is an articling public accounting student working on his first financial statement audit engagement. The client is BBB Appliances Inc. One of his duties was to prepare an aging of the company’s accounts receivables. His audit supervisor explained that the company’s receivables have

Johnson Clock Company sells specialty clocks, watches, and other timekeeping devices. Since its inception, the company has sold items through its home office store and atIndustry and collector trade shows around the country. To meet the demand from collectors around the world, the company began

You have been assigned to the first examination of the accounts of Duck Lake Inc. for the year ending March 31, 2012. Accounts receivable is confirmed on December 31,2011, and at that date the receivables consisted of approximately 200 accounts with balances totalling $956,750. Seventy-five of

The following are the entire outstanding accounts receivable for Stan€™s Bookbinding Company Ltd. The population is smaller than would ordinarily be the case for statistical sampling, but an entire population is useful to show how to select samples by monetary unit sampling.REQUIREDa. Select a

For each of the following situations:a. Discuss the key issues to address in determining whether or not revenue should be recognized.b. Identify additional information required or audit procedures to be performed by the auditor to quantify or otherwise audit the issues identified in (a).c. Use

Showing 8200 - 8300

of 10291

First

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

Last

Step by Step Answers

-1.png)

-2.png)

-1.png)

-2.png)