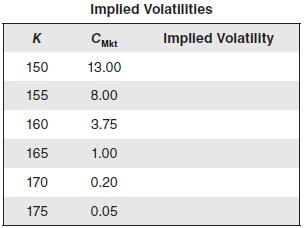

Question: Complete the following table using the following information: Column 1 reports six strike prices $150 to $175 at $5 intervals. Column 2 is

Complete the following table using the following information:

• Column 1 reports six strike prices $150 to $175 at $5 intervals.

• Column 2 is for the closing stock price on YBM, $160.

• Column 3 is for the risk-free interest rate r = 10 percent per year.

• Column 4 is for the time to maturity, which is twenty days (20/265 = 0.054795 years).

• Column 5 reports European call option prices from the market.

• Column 6 reports the implied volatility that you need to calculate.

150 155 160 165 170 175 Implied Volatilities CMktImplied Volatility 13.00 8.00 3.75 1.00 0.20 0.05

Step by Step Solution

3.41 Rating (154 Votes )

There are 3 Steps involved in it

To solve for implied volatility 1 Fill out the first six columns as directed in the problem use a gu... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

646-B-B-F-M (2935).docx

120 KBs Word File