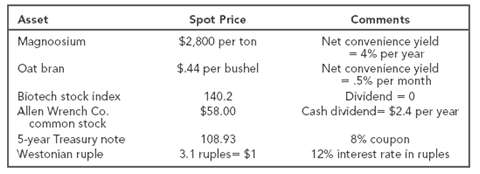

Question: Consider the commodities and financial assets listed in Table 27.6. The risk-free interest rate is 6 percent a year, and the term structure is flat.

Consider the commodities and financial assets listed in Table 27.6. The risk-free interest rate is 6 percent a year, and the term structure is flat.

a. Calculate the six-month futures price for each case.

b. Explain how a magnoosium producer would use a futures market to lock in the selling price of a planned shipment of 1,000 tons of magnoosium six months from now.

c. Suppose the producer takes the actions recommended in your answer to (b), but after one month magnoosium prices have fallen to $2,200. What happens? Will the producer have to undertake additional futures market trades to restore its hedged position?

d. Does the biotech index futures price provide useful information about the expected future performance of biotech stocks?

e. Suppose Allen Wrench stock falls suddenly by $10 per share. Investors are confident that the cash dividend will not be reduced. What happens to the futures price?

f. Suppose interest rates suddenly fall. The spot rate for cash flows 6 months from now is 4 percent (per year); it is 4.5 percent for cash flows 12 months from now, 4.8 percent for cash flows 18 months from now, and 5 percent for all subsequent cash flows. What happens to the six-month futures price on the five-year Treasury note? What happens to a trader who shorted 100 notes at the futures price calculated in part (a)?

g.?An importer must make a payment of one million ruples three months from now. Explain two?strategies the importer could use to hedge against unfavorable shifts in the ruple?dollar exchange rate.

Asset Spot Price Comments Net convenience yield = 4% per year Net convenience yield -.5% per month Dividend = 0 Cash dividend= $2.4 per year Magnoosium $2,800 per ton Oat bran $.44 per bushel Biotech stock index 140.2 Allen Wrench Co. common stock $58.00 5-year Treasury note Westonian ruple 108.93 8% coupon 12% interest rate in ruples 3.1 ruples= $1

Step by Step Solution

3.36 Rating (159 Votes )

There are 3 Steps involved in it

a For each we make use of the general relationship or Futures price 1 rf t Spot price PVconvenience yield Thus the sixmonth futures prices are Note th... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

35-B-C-F-R-A-M (28).docx

120 KBs Word File