Robeson County has a Capital Projects Fund for its courthouse renovations. The appropriation authority for the fund

Question:

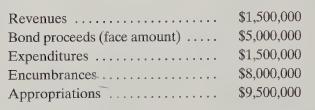

Robeson County has a Capital Projects Fund for its courthouse renovations. The appropriation authority for the fund continues until the end of the project. The voters approved a bond issue for the specific purpose of financing courthouse renovations and the county commissioners committed a revenue source specifically for that purpose as well. The commission’s policy is that expenditures are presumed to be made first from bond proceeds, then from the committed revenue source. The fund has the following balances as of September 30, 20X8, its first fiscal year-end:

Assume that $1,500,000 of unassigned General Fund resources were transferred from the General Fund to provide financing instead of the commission committing revenues specifically to the project. How should Fund Balance as of September 30, 20X8, be reported?

a. Restricted, $5,000,000.

b. Assigned (by voters) $5,000,000.

c. Restricted, $3,500,000 and Assigned, $1,500,000.

d. Restricted, $3,500,000 and Unassigned, $1,500,000.

e. None of the above.

Step by Step Answer:

To determine how the Fund Balance should be reported lets analyze the inf...View the full answer

Governmental And Nonprofit Accounting Theory And Practice

ISBN: 9780132552721

9th Edition

Authors: Robert J Freeman, Craig D Shoulders, Gregory S Allison, Terry K Patton, Robert Smith,