Choose the best answer. 1. Which of the following would not be considered a general long-term liability?

Question:

1. Which of the following would not be considered a general long-term liability?

a. The estimated liability to clean up the hazardous waste storage sites of the city€™s Public Works Department.

b. Capitalized equipment leases of the water utility fund.

c. Compensated absences for the city€™s Police Department.

d. Five-year notes payable used to acquire computer equipment for the city€™s administrative offices.

2. Proceeds from bonds issued to construct a new city hall would most likely be recorded in the journal of the

a. Capital projects fund.

b. Debt service fund.

c. General Fund.

d. Enterprise fund.

3. The liability for long-term debt issued to finance a capital project will appear in which financial statement?

a. Government-wide statement of net position.

b. Capital projects fund balance sheet.

c. Debt service fund balance sheet.

d. General Fund balance sheet.

4. Which one of the following statements regarding debt margin is correct?

a. Debt margin is the total amount of indebtedness of specified types of debt that is allowed by law to be outstanding at any one time.

b. Debt margin is calculated without regard to debt that is authorized but not yet issued.

c. Debt margin is the difference between the legal debt limit and the amount of net indebtedness subject to limitation.

d. All of the above statements regarding debt margin are correct.

5. Budgeting entries for a debt service fund would

a. Not include an entry for estimated revenues because taxes are always recorded directly into the General Fund.

b. Include an estimated adjustment to bonds payable equal to the amount of principal payments that will become legally due during the fiscal year.

c. Include estimated other financing uses equal to the amount of interest payments that will become legally due during the fiscal year.

d. Include appropriations for principal payments that will become legally due during the fiscal year.

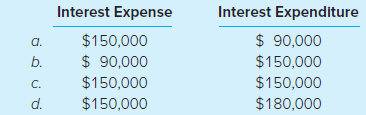

6. On March 2, 2020, 20-year, 6 percent, general obligation serial bonds were issued by Mossy County at the face amount of $3,000,000. Interest of 6 percent per year is due semiannually on March 1 and September 1. The first principal payment of $150,000 is due on March 1, 2021. The county€™s fiscal year-end is December 31. What amounts are reported as interest expense in the government-wide financial statements and interest expenditure in the debt service fund for 2020?

7. Debt service funds may be used to account for all of the following except

a. Repayment of debt principal.

b. Lease payments.

c. Amortization of premiums on bonds payable.

d. The proceeds of refunding bond issues.

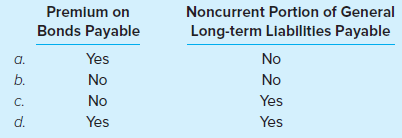

8. Which of the following items would be reported in the Governmental Activities column of the government-wide financial statements?

9. The liability for special assessment bonds for which the city is not obligated in any manner should be recorded in a

a. Debt service fund general journal.

b. Custodial fund general journal.

c. Governmental activities general journal.

d. None of the fund or governmental activities general journals but should be disclosed in the notes to the financial statements.

10. Total general long-term indebtedness subject to debt margin calculations typically does not include

a. Debt authorized but not issued as of year-end.

b. Special assessment debt for which a government might be liable if collections are insufficient.

c. General obligation debt.

d. Lease obligations.

11. Payment of general obligation bond interest would be recorded as

a. An expenditure in the governmental activities general journal.

b. An other financing use in the governmental activities general journal.

c. An expenditure in the debt service fund general journal.

d. An other financing use in the debt service fund general journal.

12. Debt issuance costs

a. Include legal and administrative fees associated with bond issuance.

b. Are recognized as an expense at the governmental fund level.

c. Are capitalized and amortized over the life of the bond.

d. Are reported as deferred outflows of resources at the government-wide level.

13. If bonds are sold at a premium:

a. The premium is typically recorded in the debt service fund at the fund level.

b. The premium is amortized at the government-wide level.

c. The premium is recorded as a component of the bond liability at the government-wide level.

d. All of the above statements are true.

14. Annual lease payments

a. Are required to be paid from a debt service fund.

b. Require payment of interest from a debt service fund and principal from governmental activities.

c. Are recorded at both the fund and government-wide levels.

d. Are reported in the notes to the financial statements but not within the financial statements themselves.

15. Long-term liabilities of a government

a. Include compensated absences, claims and judgments, and pollution remediation obligations.

b. Are only reported at the fund level within the financial statements.

c. Are only reported at the government-wide level within the financial statements.

d. Both a and c are true.

Financial statements are the standardized formats to present the financial information related to a business or an organization for its users. Financial statements contain the historical information as well as current period’s financial...

Step by Step Answer:

1 b 2 a 3 a 4 c 5 d ...View the full answer

Accounting for Governmental and Nonprofit Entities

ISBN: 978-1259917059

18th edition

Authors: Jacqueline L. Reck, James E. Rooks, Suzanne Lowensohn, Daniel Neely