On 1 January 20x4, P Co purchased a 90% interest in Topaz Co, a company that specializes

Question:

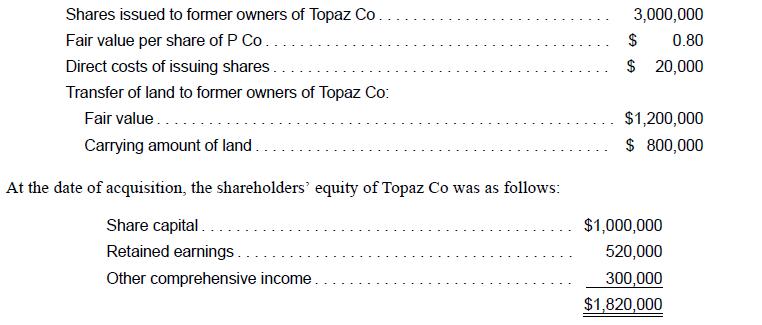

On 1 January 20x4, P Co purchased a 90% interest in Topaz Co, a company that specializes in developing patented engineering processes. To acquire the controlling interest in Topaz Co, P Co transferred consideration to the former owners of Topaz Co as follows:

The fair value of non-controlling interests on acquisition date was $340,000. As at acquisition date, Topaz Co had a research and development project that had the following expected outcomes:

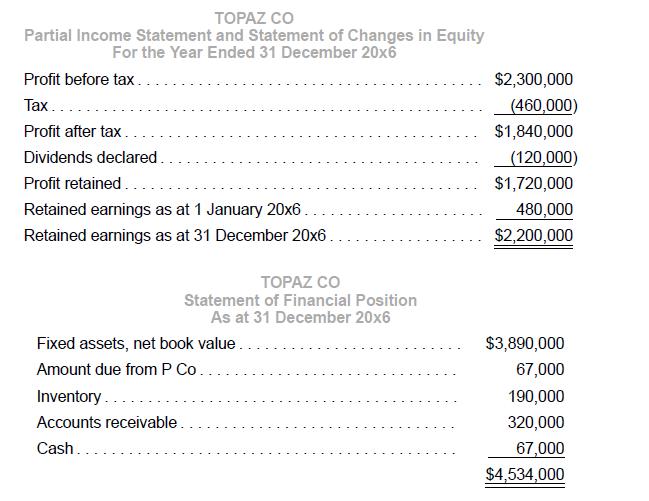

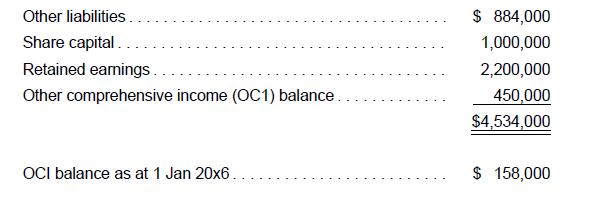

Topaz Co incurred research expenditures of $120,000. The development expenditures incurred to acquisition date of $100,000 did not meet the conditions for capitalization in IAS 38 Intangible Assets. Topaz Co successfully completed the research and development project on 31 December 20x5. The estimated economic life of the intangible asset was ten years. P Co and its group use the cost model to measure its intangible assets. The financial statements of Topaz Co for the year ended 31 December 20x6 are as follows:

Additional information:

(a) On 1 July 20x5, Topaz Co transferred excess equipment to P Co at an invoiced price of $1,200,000. Topaz Co had purchased the equipment on 1 July 20x2 at an original cost of $800,000, when the useful life was ten years.

The remaining useful life on 1 July 20x5 was four years. Residual value was negligible.

(b) On 1 July 20x6, P Co sold inventory to Topaz Co at the transfer price of $360,000. The carrying amount of the inventory in P Co’s books prior to the sale was $280,000. Forty percent remained unsold as at 31 December 20x6.

(c) Recognize tax effects on fair value adjustments and other adjustments at the tax rate of 20%.

(d) Other comprehensive income (OCI) arises from items of income that bypass net income in accordance with IAS 1 Presentation of Financial Statements. OCI is built up in separate accounts in equity. (Hint: Where OCI balance at beginning of the year is provided, separate allocation of current and change in post-acquisition OCI in the same way as for profit and post-acquisition retained earnings).

Required:

1. Explain how the accounting for research and development differs for the legal entity and the economic entity at acquisition date and after acquisition date in accordance with IAS 38.

2. Prepare consolidation entries for the year ended 31 December 20x6, with narratives (brief headers) and workings in accordance with IFRS 3 and IFRS 10.

3. Perform an analytical check on the balance of non-controlling interests as at 31 December 20x6, showing the workings clearly.

4. If P’s retained earnings as at 31 December 20x6 was $5,000,000, perform an analytical check on consolidated retained earnings as at 31 December 20x6.

5. If the fair value of the remaining inventory sold by P Co to Topaz Co was $130,000 as at 31 December 20x6, explain if the new information has any effect on your consolidation adjustment.

Step by Step Answer:

Advanced Financial Accounting An IFRS Standards Approach

ISBN: 9781285428765

4th Edition

Authors: Pearl Tan, Chu Yeong Lim, Ee Wen Kuah